Gold’s Very-Bullish Futures

Adam Hamilton, CPA

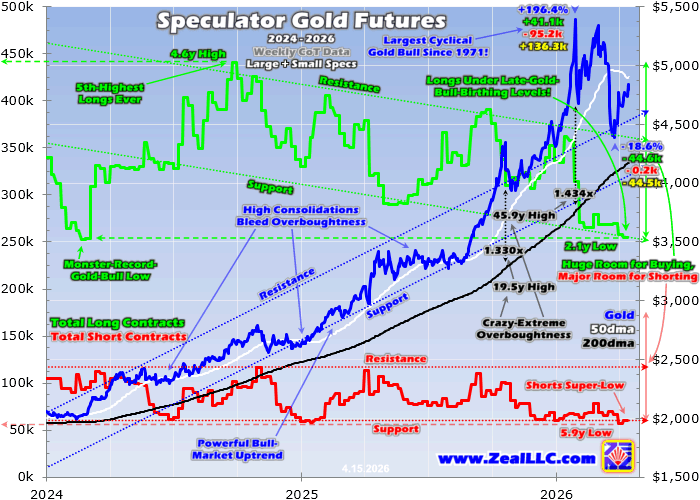

Gold remains really high despite March’s sharp correction, not far off January’s extraordinary records. So speculators’ capital firepower available for buying gold futures should have already been spent, largely tapped-out. Yet astonishingly specs’ upside bets have dwindled under their levels that birthed gold’s late monster record bull! Very-bullish gold-futures positioning remaining after such a colossal run is unprecedented.

From early October 2023 to late January 2026, gold soared 196.4% in its biggest cyclical bull ever in US-dollar terms! During that entire 27.8-month behemoth, gold didn’t suffer a single 10%+ correction. Then from that peak into late March, gold plunged 18.6% in a serious one. That dragged gold overboughtness from a terrifying 45.9-year high to a decent 1.2-year low, helping rebalance extreme technicals and sentiment.

That correction ignited in late January with a violent 10.3% single-day gold crash, its third-worst daily loss since 1971! That was effectively when dollar-gold history started, since the dollar was severed from the gold standard that year. Crazy-heavy gold-futures long dumping fueled that. Speculators’ gold-futures positioning is reported weekly in Commitments of Traders reports, current to Tuesdays but released late Fridays.

Straddling late January into early February, in two consecutive CoTs specs jettisoned a withering 43.1k and 43.7k long contracts! Those ranked as the 14th- and 13th-biggest in that entire dataset extending all the way back to January 1986, or top 0.7%. In two-CoT-week-span terms, that surged to the 2nd-largest spec long dumping ever at 86.8k contracts, nearly breaking the 89.1k record from mid-December 2017!

For decades prior to gold’s remarkable late monster record bull, American specs’ gold-futures trading was often the dominant driver of gold’s short-term price action. It still is from time to time, like late January. The reason is the extreme leverage inherent in that realm. Each gold-futures contract controls 100 troy ounces of gold, worth $479,300 at midweek prices. Yet specs don’t have to put up anywhere near that to trade.

Currently margin requirements are only $33,600 cash held in accounts for each contract traded. That allows extreme maximum leverage of 14.3x, which is actually really low for gold futures. Before gold’s volatility exploded in that recent record bull, 20x to 25x was normal! Even at 14x, every dollar deployed in gold futures has 14x the price impact on gold as a dollar invested outright. So specs wield outsized influence.

When American speculators as a herd rush into or out of gold futures, gold moves big. Those swings further really affect investor sentiment, as the US gold-futures price is the world reference one for gold. So there have been many episodes over the decades where spec gold-futures trading proved the small tail wagging the vastly-larger investment-demand dog. Late January was just the latest in a long line of them.

Normally in major gold bulls, spec gold-futures buying is one of their primary drivers along with global investment demand usually led by Americans. So spec gold-futures positioning follows a well-worn trend as gold marches higher. Gold bulls are born when spec longs are low and spec shorts are high, which implies these super-leveraged traders have done about all the selling they are likely to do leaving only buying.

That was certainly the case in early October 2023 when that monster record gold bull was born. Total spec longs ran just 264.8k contracts, not too far above late November 2022’s deep 3.6-year low. And total spec shorts had soared to 174.4k contracts, nearly matching a 3.8-year high seen in late September 2022. So speculators were unlikely to dump many more longs, and unlikely to keep ramping really-high shorts.

They had vastly more room to buy than sell, and that’s exactly what they did helping fuel gold’s early bull run. By late September 2024 spec longs had soared to a lofty 4.6-year high of 441.0k, and by mid-January 2025 spec shorts had collapsed to a 4.7-year low of 58.4k. The total amounts of this spec long buying and short-covering buying were enormous, which is easier to understand in gold-equivalent terms.

That 176.2k contacts of long buying was equivalent to 548.1 metric tons of gold, while the parallel 116.0k of short covering equated to another 360.8t! That 908.9t of gold-equivalent gold-futures buying was pivotal in fueling gold’s early record bull run. It was the impetus behind initial strong gold gains that were big enough to entice in world investors, providing the torque necessary to get their large demand flywheel spinning.

Because these raw contract numbers are difficult to parse without lots of data, I like to consider both spec longs and shorts relative to their gold-bull trading ranges. Their lowest level within a particular gold bull is recast at 0%, and their highest 100%. So normally major gold bulls are born near 0% longs and 100% shorts, then peak around 100% longs and 0% shorts. Specs gradually shift from all-out early to all-in late.

Watching spec positioning within these ranges reveals high-probability-for-success times to buy and sell gold and thus its miners’ stocks, this is a very-valuable trading tool. Further shaping this analysis, spec longs and shorts aren’t equal in importance. While buying or selling an individual long or short contract has the same gold-price impact, longs greatly outnumber shorts making them proportionally more important.

During the 121 CoT weeks gold’s late record bull spanned, spec longs averaged 4.0x larger than spec shorts. That makes the former about 4x more important in driving gold price trends than the latter due to that huge size differential. In the latest CoT report current to last Tuesday, that typical ratio persists still at 4.2x. With this background, what is going on today in spec gold-futures positioning is utterly mind-boggling.

This chart superimposes daily gold prices in blue over weekly CoT total spec longs and shorts rendered in green and red. Again late in a major gold bull you’d expect to see spec gold-futures buying effectively exhausted near 100% longs and 0% shorts. But that mostly hasn’t happened recently, and despite gold staying really high total spec longs have collapsed below this late monster record gold bull’s birthing levels!

After spending decades studying gold-futures trading’s impact on gold prices, I would’ve thought today’s situation impossible. As of the latest-reported CoT current to Tuesday April 7th, total specs longs are running just 254.5k contracts. That was just a hair above their monster-record-gold-bull low of 252.9k way back in mid-February 2024, and well under the 264.8k in early October 2023 birthing this gold bull at just $1,820!

This is such an extreme anomaly I struggled to believe it for weeks, wondering if there was some problem with CoT data. But if those ever happen, they quickly work themselves through in subsequent CoTs. Last Tuesday gold remained 158.6% above bull-launching levels, yet total spec longs had collapsed back to 3.9% lower! Trying to comprehend such sorcery, one thesis is far-higher gold prices limit gold-futures trading.

The risks inherent in gold-futures trading trounce most other markets. At 14x leverage, a mere 7.1% gold move against bets wipes out 100% of capital risked. And as we’ve seen in spades in recent months, gold can swing 7%+ in a few days without breaking a sweat. So the number of gold-futures traders is quite small relative to broader markets, controlling quite-finite pools of capital. Does higher gold mean fewer contracts?

Maybe, but much evidence is to the contrary. For example in late September 2025 while gold soared to $3,763 for the first time in history, spec longs swelled to 390.5k contracts. That was closing in on their many-years-old upper-resistance zone around 413k contracts. Yet when spec longs first exceeded 390k in that late gold bull in mid-June 2024, gold was only running $2,465. So gold 53% higher, yet spec longs the same!

A way-more-likely explanation of waning spec longs as gold soared is the remarkable nature of that late bull. American gold-futures speculators’ and American stock investors’ long-established leading roles in fueling major bulls were usurped by massive global demand as gold powered higher. That was dominated by central banks, Chinese speculators and investors, and Indian investors and gold-jewelry buyers.

I’ve analyzed this extensively in our newsletters in recent years, but consider an illustrative example. In 2025 gold skyrocketed an astonishing 64.3%! Yet net spec gold-futures buying was negligible, they added a tiny 5.5k longs and a trivial 1.6k shorts for minuscule gold-equivalent buying of 12.3t. And the easiest way to measure American stock investors’ gold buying is through the world-dominant US gold ETFs’ holdings.

Last year the combined bullion held by GLD, IAU, and GLDM climbed 372.1t utterly dwarfing gold-futures buying. The World Gold Council publishes the best-available global gold supply-and-demand data quarterly in its fantastic Gold Demand Trends reports. According to the WGC, overall global gold-ETF demand weighed in at 801.2t in 2025 including that GLD+IAU+GLDM buying which declined to just 46% of it.

In some past major-gold-bull years, GLD+IAU+GLDM accounted for nearly all and sometimes more of overall worldwide gold-ETF demand! In 2025 global central-bank demand weighed in at 863.3t, far bigger than both US gold-futures and US gold-ETF demand combined. And in China and India last year, total consumer demand including both bullion and jewelry ran a hefty 830.3t and 710.9t both dwarfing US buying.

So the gold-price-moving importance of leveraged American gold-futures trading hasn’t vanished, it has just been wildly overshadowed by enormous global gold demand. If specs flood back into gold futures from current astounding lows, that would almost certainly again catapult gold higher. 14x leverage for 14x the gold-price impact remains incredibly potent. Today’s really-low spec longs are very bullish for gold.

If something motivates specs to start chasing gold again, they now have room to do an enormous 158.5k contracts of long buying before returning to their 413k resistance. That rivals the 176.2k contracts of spec long buying at best within gold’s late monster bull, and is the equivalent of another 493.0t of gold buying. I don’t know if speculators will resume chasing gold in such uncharted territory, but they have vast room to.

These super-leveraged speculators have been more likely to add to their upside bets when gold is rallying but not rocketing. Soaring too high too fast greatly ups the odds of a big-and-fast rebalancing selloff, which can be an existential threat to gold-futures traders wielding maximum leverage. So spec longs blasted higher in Q3’24 as gold rallied, but plunged in early October 2025 as gold threatened to shoot parabolic.

The rest of 2026 looks way more modest for gold compared to 2025, and thus more gold-futures-friendly. There’s no way gold is going to skyrocket another 2/3rds this year, and is just recovering from that recent serious correction last month. If gold rallies a far-more-normal 10% to 20% in 2026, we’d be looking at year-end levels from $4,744 to $5,175. Such way-less-risky gradual advancing could convince specs to return.

Last week in my essay on gold stocks’ spring rally, I included a gold-seasonals chart. In all modern bull-market years since 2001, or fully 22 of these last 25 years, gold has averaged very-impressive 16.6% annual gains. Something more along those lines this year could easily entice speculators to flood in and normalize their really-low longs, accelerating gold’s recovery. I suspect that will indeed come to pass.

While total spec longs now running just 0.9% up into their late monster record gold bull’s trading range is very bullish for the yellow metal, the current super-low shorts sure aren’t. Weighing in at just 60.7k contracts last Tuesday, that is only 3.5% up into their own similar trading range. And the CoT week before they had sunk to a deep 5.9-year low of 56.6k! So specs also have lots of room to aggressively short sell.

While upper resistance of total spec shorts in recent years is around 115k contracts, those downside bets could conceivably soar as high as 175k like back in early October 2023. So worst case that leaves room for a massive 114.3k contracts of short selling, which would hammer gold sharply lower. That could very well be unleashed if gold rolls over into a bear market suffering mounting selling pressure, which is possible.

But it doesn’t seem very likely. As analyzed a few weeks ago in my essay on gold’s war disconnect, gold still has plenty of great bullish fundamentals going for it. Global demand remains robust by most accounts, American stock investors’ implied portfolio allocations were shockingly still less than 0.5% even as gold peaked in late January, and the coming stock bear as this AI bubble inevitably bursts will boost diversification.

And the longer gold remains high and the higher it powers, the more herd psychology shifts from bearish to bullish. Several years ago all but the hardened contrarians believed gold was dead, an obsolete asset class. Today all kinds of investors around the world are increasingly realizing gold remains an essential part of all portfolios. With that worldview moving toward universal acceptance, huge shorting gets irrational.

Again normally gold bulls end leading to gold bears when spec longs are way up near 100% into their bull trading range and spec shorts near 0%. Today those numbers are under 1% and 4%, respectively really-bullish and quite-bearish for gold! But spec longs are 4x more important than shorts due to the relative numbers of those contracts outstanding. So the bullish gold case based on very-low spec longs is much stronger.

Even if specs don’t flood back into longs in coming months to chase gold’s gains, super-low spec longs dramatically slash the risks of big-and-fast gold plunges. While specs had room to jettison that near-record 86.8k longs in two CoT weeks in late January crashing gold since they started at 357.9k contacts, they almost certainly can’t again far lower at that 254.5k. Fewer gold plunges will bolster global investors’ confidence.

When gold shot parabolic in late January, I was really bearish warning of an imminent big-and-fast-selloff reckoning. After that came to pass in line with historical averages in late March, we started aggressively adding a bunch of great new mid-tier and junior gold-stock trades in our weekly newsletter. Those are surging with gains already as high as +19.4%! The really-low spec gold-futures longs helped justify those buys.

The bottom line is speculators’ gold-futures positioning is very bullish for gold today. Despite it remaining not far under recent record highs, total spec longs are actually below levels birthing gold’s late monster record bull. That means these super-leveraged traders have vast room to flood back in and chase gold higher, amplifying its gains. This extreme anomaly is unprecedented, driven by that gold bull’s unique nature.

American gold-futures specs’ traditional co-starring role in driving gold higher was greatly overshadowed by massive sustained global demand dominated by central banks, Chinese, and Indians. That enabled gold to continue soaring higher as specs reversed all their early-bull long buying. While spec shorts are bearish for gold like usual, spec longs are proportionally more important outnumbering shorts about 4x.

Adam Hamilton, CPA

April 17, 2026

Copyright 2000 – 2026 Zeal LLC (www.ZealLLC.com)

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.