AOTH’s investing strategy in a changing macro environment that favors commodities and precious metals – Richard Mills

2025.10.18

The following article summarizes Ahead of the Herd’s approach to investing, shows how we have been right about the cyclical turn towards commodities, including critical and precious metals, and features 13 client advertisers on our website, aheadoftheherd.com.

Top-down, bottom-up investing

When looking for an investment, the approach I take involves looking at the global, big-picture conditions. I study trends, read the news, basically watch and listen to what’s going on in the world. Then I study the different sectors to select the one(s) that I think is going to match up well with the overriding, long-term theme. This is top-down investing.

The second part of my search for an investment is a bottom-up approach. This is where I find individual companies in the specific sector, I have chosen to invest in.

Project development stages and risk versus reward — Richard Mills

If you’ve done your homework, all the necessary ingredients for a potentially successful investment — the right place and time, the right sector, an excellent project in a safe jurisdiction, and a high-quality management team — should be in place.

Remember, everything about a company flows from management — the ability to find a project or have joint ventures (JVs) offered to the company; developing the project in a timely and efficient manner; financings done at a higher and higher share price; control over the share structure; and management interests aligned with shareholder interests.

I spend most of my due diligence time and effort on:

- A top-down theme — discover the dominant overall global theme(s).

- Bottom-up searches — find the companies involved at the stage your comfortable investing in.

- Management due diligence

Think of an investment in a junior mining play as a journey from high-risk speculation to a lower risk investment. The milestones in getting to the destination are a series of de-risking events made possible by exploration, which most often includes taking soil or rock chip samples, conducting geochemical or geophysical surveys, and diamond drilling, the ultimate “truth machine” that either confirms or denies geological theories.

These milestones start with an initial discovery, with more drilling leading to a maiden (first) resource estimate and are followed by a series of economic/ technical studies, including a PEA, prefeasibility study and feasibility study.

The point here is not that juniors are risky investments, they are but that a great deal of the risk can be taken out of them, through exploration and the completion of milestones that serve to prove the geological model and the extraction plan for getting the resource to market.

Early-stage “greenfield” exploration plays that succeed in finding a discovery have a good chance of finding more on the property and that moves them into the post-discovery, resource definition stage, my favorite stage junior. The discovery has been made, the junior is going to try to put together a resource estimate, a MRE.

Once a company outlines a resource, the next phase is developing the asset further. Completing the various technical studies required serves to de-risk the project and moves it further along the path to becoming a mine.

The big money is made by investing in a junior at an exceedingly early stage, usually when the stock has a miniscule market cap (MC) and it’s shares are trading for pennies.

Commodities: the last safe haven standing

Commodities tend to be “boom and bust”, also known as super-cycles.

A “commodity super-cycle” is a period of consistent price increases lasting more than five years, and in some cases, decades. The Bank of Canada defines it as an “extended period during which commodity prices are well above or below their long-run trend.”

Super-cycles occur because of the long lag between commodity price signals and changes in supply. While each commodity is different, the following is a rundown of a typical boom-bust cycle:

As economies grow, so does the demand for commodities, and eventually the demand outstrips supply. That leads to rising commodity prices, but the commodity producers don’t initially respond to the higher prices because they’re unsure whether they will last. As a result, the gap between demand and supply continues to widen, keeping upward pressure on prices.

Eventually, prices get so attractive that producers respond by making additional investments to boost supply, narrowing the supply and demand gap. High prices continue to encourage investment until finally, supply overtakes demand, pushing prices down. But even as prices fall, supply continues to rise as investments made during the boom years bear fruit. Shortages turn to gluts and commodities enter the bearish part of the cycle.

There is a significant upswing coming in the commodity cycle that will be driven by geopolitical tensions and underinvestment in the mining sector, according to McEwen Mining’s Executive Chair and Chief Owner, Rob McEwen.

“Right now, we’re at the bottom of the cycle, and it’s ascending,” McEwen told Kitco Mining on the sidelines of the 2025 Mines and Money conference. He emphasized that commodities are at a 10-12-year low relative to financial assets, suggesting substantial room for growth. (Kitco News)

Leigh Goehring, Managing Partner at Goehring & Rozencwajg and a seasoned investor in natural resources, in 2024 shared his wealth of experience on the Commodity Culture podcast. His message is clear: the time to dive into commodities is now, as they are currently at their most undervalued state in market history. (Goehring & Rozencwajg)

AOTH predicted the boom in commodities as far back as December 2023.

In the article, Why commodities are sailing into a perfect storm of higher prices — Richard Mills, we identified global warming, El Nino, agriculture, water, energy, shipping, metals, and resource nationalism as factors leading to higher commodity prices.

We wrote:

“Many metals — including copper, graphite, nickel and cobalt — are going to be increasingly hard to source in the West due to lack of exploration spending, a lack of refineries and smelters and 20-year permitting timelines to build new mines.

Throw in the looming threats of global warming, El Nino, and resource nationalism which will only drive prices higher.

Think about it: we can’t mine, we can’t refine, we’re running out of fresh water, our oceans are dying, and people are scrambling to either stop resource development or governments are hanging on tightly to whatever resources they have and charging higher resource rents for it.

The end result is a perfect storm for commodities — a major bull market across the board. The shift from tight to loose monetary policy has yet to happen, but it’s coming.”

It turns out we were right about rising commodity prices.

Commodities: the last safe haven standing — Richard Mills

The Fed stopped raising interest rates in July 2023 and started cutting them in September 2024. Lower interest rates lessen the cost of carrying inventories and raise commodity prices. (Harvard Kennedy School)

Lowering interest rates weakens a country’s currency by making it less attractive for foreign investors seeking higher returns. This can cause the US dollar to weaken as investors move their money to countries with higher interest rates.

The decline in the value of the dollar is one of the most newsworthy trends of 2025, along with the Trump tariffs.

The US dollar index (DXY), which reflects the dollar’s value against a basket of other currencies, is down about 10% year to date. According to CNBC, it was the worst first half of the year for the dollar since 1973.

A lower dollar is good for most commodities including metals. That’s because if the USD depreciates, commodity prices rise because they become cheaper for holders of other currencies. (EBC Financial Group)

As of Oct. 8, 2025, the Bloomberg Commodity Total Return Index had climbed 12% year to date to reach a three-year high. The bulk of the performance has been driven by five key commodities: gold, silver, copper, arabica coffee and live cattle. (@Ole_S_Hansen on X)

Gold is now up 65% year to date and reached a record-high $4,379.50/oz on Oct. 17, silver is doing even better at a YTD increase of 75%, and palladium and platinum have both gained 68%. Copper is up 24%, currently trading at $4.95/lb and continues its climb from $2/lb in 2016, having spiked to $5.80/lb in July.

In fact, commodities are the last safe-haven standing in a world of low bond prices and high yields (investors don’t like long-term bonds like the 10-year and the 30-year Treasury because of the risk of higher inflation.) US inflation has climbed from 2.3% in April to 2.9% in August).

Meanwhile, the dollar and US Treasuries are both waning as safe havens, with gold being the chief beneficiary.

When the US dollar depreciates against the world’s major currencies such as the euro and the yen, gold prices usually rise. Because gold is traded in dollars, when the dollar weakens, gold is cheaper compared to other currencies, boosting its appeal to investors.

The second Trump administration has been characterized by a low dollar, which is just the way Trump likes it, since a weak dollar is good for exports, and backs Trump’s mantra of repatriating American manufacturing jobs lost to overseas competition.

Three factors why the dollar has been in decline, by Visual Capitalist:

- GDP growth projections are soft

- Inflation expectations are stable but elevated

- Interest rates are down

There’s also de-dollarization. August’s global fund manager survey from the Bank of America found investors were 16% underweight the dollar, the lowest level since 2006.

Reuters columnist Mike Dolan says the 20-year high in dollar underweighting by asset managers indicates both wariness of US assets at large — due to concerns about the current US administration’s approach to global trade, geopolitics and institutional integrity — and a more structural dollar retreat.

Many emerging-economy central banks are exploring alternatives to the dollar-based financial system which they increasingly see as a source of vulnerability rather than stability.

After the 2022 invasion of Ukraine, the US and its allies froze $335 billion of Russia’s foreign exchange reserves, which alarmed other nations. They bought and are still buying gold to prevent the same thing from happening to them.

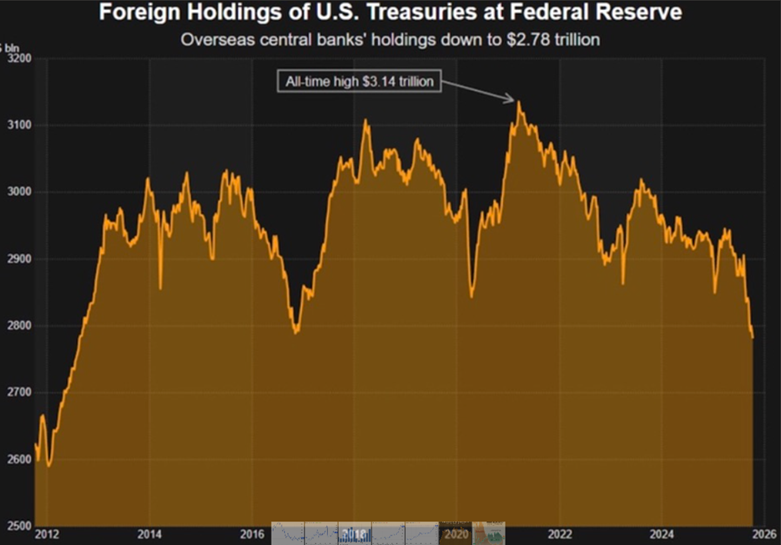

The US Treasury market is the largest and most liquid government securities market globally, with over $29 trillion in outstanding securities as of September 2025.

However, Reuters reported that The amount of U.S. Treasuries held at the New York Fed on behalf of global central banks has slumped to its lowest in over a decade, casting renewed doubt on foreign appetite for U.S. sovereign debt and other dollar-denominated assets…

The latest figures show that the value of U.S. Treasuries held at the New York Fed on behalf of foreign central banks is $2.78 trillion. That’s the lowest since August 2012, and down $130 billion in just two months.

Indeed, it’s notable that peak holdings over the last year and a half, of $2.95 trillion, were in March-April this year, coinciding with peak market volatility around U.S. President Donald Trump’s ‘Liberation Day’ tariff chaos. According to this temperature check, foreign central banks seem to have cooled on Treasuries since then.

In fact, central banks now hold more gold than US Treasuries, which hasn’t happened since 1996. Visual Capitalist notes that persistent gold buying by CBs and rising US debt risks are reshaping reserve composition towards hard assets like precious metals.

When Britain’s neophyte Prime Minister Liz Truss published a mini budget that made unfunded tax cuts and raised the amount borrowed, the bond vigilantes sold UK gilts en masse, sunk the pound and forced Truss to resign.

Could the same thing happen in the US? Well, Trump would never resign, but quite possibly, if the United States continues to rack up debt and reduce revenues through tax cuts, it could.

Indeed, a US bond market crash seems inevitable. If it does, the last safe haven standing will be commodities, especially precious metals.

The bond vigilantes are holding their fire — for now — Richard Mills

Conclusion

Gold has received a significant boost from President Trump 2.0, and it has kept climbing as his trade war continues.

The gold ‘fear trade is on’ — Richard Mills

A major incident involving a landslide at the world’s second largest copper mine, Grasberg in Indonesia, has upended the copper market and sent the price of the base metal soaring.

On the last day of September, Bloomberg reported copper recorded its biggest monthly advance since June.

Analysts at Societe Generale SA wrote that the copper market could be on track for the widest annual supply deficit since 2004.

Freeport-McMoRan, the operator/ part owner of Grasberg, has slashed production guidance for this year and 2026.

Meanwhile demand for copper continues apace.

Electrification and decarbonization are driving demand for metals, especially critical metals like copper. Some are even calling copper the new oil.

EVs for example contain four times as much copper as gas-powered cars. Technology companies are investing hundreds of billions of dollars to build AI data centers requiring reams of copper wiring.

Demand for copper — the cornerstone for all electricity-related technologies — is set to grow by 53% to 39 million tonnes by 2040, according to BloombergNEF. A shortfall of 30% could occur by 2035.

We’ve already seen spectacular gains, but we believe that we are going to see a lot more before this precious metals and commodities bull market is over.

If the employment situation worsens and inflation keeps climbing, look for economic growth to sputter as the US enters stagflation — an unsavory mix of inflation, low growth and high unemployment.

Historically, gold outperforms other asset classes during times of economic stagnation and inflation. Of the four business cycle phases since 1973, stagflation is the most supportive of gold, and the worst for stocks, whose investors get squeezed by rising costs and falling revenues. Gold returned 32.2% during stagflation compared to 9.6% for US Treasury bonds and -11.6% for equities.

The World Gold Council (WGC) says gold is attracting more attention from central banks than at any time in the last decade.

Over the past three years, central banks have purchased over 3,000 tonnes of the precious metal. Analysts predict they could add another 1,000 tonnes to their reserves this year.

Demand is largely being driven by emerging market central banks, which are diversifying their holdings away from the US dollar, more so than developed market central banks.

Central banks worldwide are on track to buy 1,000 tonnes of gold in 2025, which would be their fourth year of massive purchases as they diversify reserves from dollar-denominated assets into bullion, consultancy Metals Focus said, via Reuters.

Gold’s share of central bank reserves reached 24% in the second quarter, its highest share since the 1990s, Deutsche Bank strategists reported on Oct. 9, via Cointelegraph.

Moreover, the de-dollarization trend continues, with foreign vendors from Latin America to Asia asking US importers to settle invoices in euros, pesos and yuan to avoid USD currency swings.

While some retail investors have sat out this gold bull due to how expensive the physical metal is (bars and coins), retail is getting in the game through gold-backed exchange traded funds.

Bloomberg reported that inflows into gold ETFs surged to a record $10.5 billion so far in September, with YTD inflows exceeding $50 billion, citing Citigroup data.

Investors are buying gold for various reasons, including: the ongoing trade war instigated by the Trump administration; the fear of a stock market crash; cryptocurrency and AI bubbles that look ready to pop; sticky inflation; rising US unemployment; the threat of a recession evidenced by a slowing of US manufacturing due to high tariffs; ballooning deficits and debt that politicians no longer seem to care about; and the prospect of further interest rate cuts.

For silver, it’s the combination of monetary and industrial demand, combined with tight supply conditions, that is driving the metal to fresh heights. A dramatic “silver squeeze” is resulting from reduced mine output, depleted warehouse inventories, fears of US tariffs on silver imports, and that China could stop bullion exports altogether. The country is the world’s second-largest silver producer behind Mexico, according to the US Geological Survey.

The silver squeeze is manifesting in the suspension of sales of silver products by the Perth Mint, possibly the first among other to follow, and silver dealers in India who are defaulting on deliveries.

We forecast higher prices in the coming months, and more records broken, as geopolitical and trade war tensions continue to roil markets and investors flock to the safety of precious metals.

As gold and silver keep climbing, along with copper — the most critical of all critical metals due to its crucial role in electrification and decarbonization — a major opportunity is presented to savvy resource investors, who know that junior resource companies, which can usually be bought for pennies or dimes on the dollar, in the right conditions can appreciate quickly. A 5-cent stock can easily quadruple to 20 cents in a commodities bull market like we are experiencing today.

Below are 13 examples of companies that we at AOTH believe offer excellent leverage to rising commodity prices:

Golden Goose Resources Corp. (CSE:CGR)

CGR’s Goldfire, Quebec project is situated between Gold Fields’ discoveries and their 4-million-ounce Windfall Mine. The project is on the Urban Barry Deformation Belt, within the world-famous Abitibi Greenstone Belt; the geology is thought to be the same as at Windfall.

Under the Spotlight – Dustin Nanos CEO, Golden Goose Resources

Golden Goose also has its La Esperanza Project in Argentina — 10 kilometers of low-sulfidation, epithermal gold veins, highlighted by 2 meters at 24 grams per tonne, another 5 meters at 13.1 g/t channel samples, and some high-grade rock chips at 24.4 g/t. Southern Copper is currently drilling just south of La Esperanza.

At the end of October, the company is returning to the Goldfire project for further exploration. The last two months of the year will be spent at La Esperanza doing more mapping and sampling to find out where the next drill targets are going to be for the drill campaign next spring.

Graphite One (TSXV:GPH, OTCQB: GPHOF)

With the United States almost 100% import-dependent for anode active materials, Graphite One is developing a complete US-based advanced graphite supply chain project anchored by the Graphite Creek deposit, recognized by the US Geological Survey as the largest graphite deposit in the country. Graphite mined from Graphite Creek, situated on the Seward Peninsula about 60 km north of Nome, Alaska, would be processed into concentrate at an adjacent processing plant. The Graphite One Project plan includes an advanced graphite material and battery anode material manufacturing plant located in Warren, Ohio.

Could G1 be the next company that Washington takes a stake in? – Richard Mills

Video: Both graphite and rare earths have military and civilian applications

Graphite One has received significant grants and two letters of interest to provide up to $895 million in loans from the federal government. Also, Graphite One could play a crucial role in breaking US dependence on China for graphite imports.

Based on G1’s Feasibility Study released in April, the Graphite Creek Mine in Alaska would have capacity to produce 175,000 tonnes of graphite concentrate per year during its projected 20-year mine life — a production rate triple that of two years ago.

In 2023, G1 closed a $2 million private placement from Bering Straits Native Corporation to support development of the Graphite Creek deposit. Earlier this month, Graphite One announced a second strategic investment from two native corporations, Doyon Limited and Aleut, for aggregate gross proceeds of $5 million (approx. CAD$7 million).

Harvest Gold Corporation (TSXV:HVG)

Harvest Gold Corporation is exploring three large 100%-owned gold exploration properties in the world-renowned Abitibi region of Quebec, the seventh-ranked mining and exploration jurisdiction in the world.

The Abitibi is a geological formation now dominated by Gold Fields. Harvest Gold controls three large prospective land packages (Urban Barry, Mosseau and La Belle) all overlaying the same geological contact within the Urban Barry Greenstone Belt.

On July 24 HVG announced they have identified 23 priority drill targets in the central and north parts of Mosseau.

Drilling began in August, with 5,000 meters planned in a first phase. The company also completed a high-resolution magnetic survey over Mosseau and La Belle in September, and a property-wide till sampling survey of Urban Barry at the end of August.

As of Oct. 3, 14 holes at Mosseau had been completed, totalling 3,030 meters. The three most recent holes targeted the central portion of the property, where historical prospecting and diamond drilling work suggested strong potential and continuity of the gold mineralization.

Harvest Gold has also engaged IOS Geosciences of Chicoutimi, Quebec to operate its fall field exploration program, which will include soil sampling, prospecting and mapping across parts of the Mosseau and LaBelle properties. This work is designed to build on recent high-resolution magnetic survey results and to further refine drill targets for upcoming exploration campaigns.

Ahead of the Herd & Under the Spotlight – Rick Mark, CEO Harvest Gold (TSX.V:HVG)

Kodiak Copper (TSXV:KDK, OTCQB:KDKCF)

Kodiak Copper’s MPD Project is a 344-square-kilometer land package near several operating mines in the southern Quesnel Terrane, British Columbia’s primary copper-gold producing belt.

The company has published a partial initial resource estimate that comprises four of the seven mineralized zones: Gate, Ketchan, Man and Dillard. Between the indicated and inferred categories, the resource amounts to 1.676 billion pounds of copper and 1.21 million ounces of gold.

The 2025 drill program has focused on near-surface infill and confirmation drill holes at the West, Adit, and South zones using a combination of diamond and reverse circulation (RC) drilling.

A total of 44 holes and 5,003 meters was completed in mid-August.

Together with the resource estimate for the first four mineralized zones (Gate, Ketchan, Man and Dillard), this will complete the initial resource estimate for the MPD project — expected in Q4.

Results from nine drill holes at Adit were presented on Sept. 3.

Results from shallow infill drilling (10 holes @ 1,405m) at the West and South zones were presented on Sept. 22.

While the company has identified multiple zones, it remains committing to continued exploration to further grow the project, both through zone expansion and the testing of new targets.

On Sept. 25 Kodiak closed an oversubscribed $8 million bought deal private placement.

Ahead of the Herd & Under the Spotlight – Claudia Tornquist, CEO Kodiak Copper

Max Resource Corp. (TSXV: MAX, OTC:MXROF, FSE:M1D2)

Max Resource is focused on the Sierra Azul Copper-Silver Project, which sits along the Colombian portion of the world’s largest copper producing belt; and the Florália DSO Iron Ore Project located within the Iron Quadrangle in Brazil.

The strength of the Sierra Azul discovery led to an option earn-in agreement with Freeport Exploration Corp, a wholly owned affiliate of Freeport-McMoRan, the world’s largest copper miner and the world’s fifth largest miner by market cap.

In May 2024 Max acquired the Florália DSO Iron Ore Project, which appears to have significant potential with a possible pathway to near-term cash flow.

A wholly owned Australian entity, Max Iron Brazil Ltd., plans to list on the ASX, with Max shareholders approving the undertaking of an IPO.

The 2025 exploration campaign consisted of channel sampling, diamond and mobile auger power drilling.

A 55% stake in Max Brazil targeting production approvals and the largest copper producer in the world spending another $44 million to advance Sierra Azul presents investors with a compelling case to put Max at the top of their watch list.

In August Max reported that it acquired the Mora Gold-Silver Title, a highly prospective gold-silver concession in the Middle Cauca Gold Belt, which stretches across central Colombia and is home to several world-class gold deposits.

On Oct. 15 Max closed an oversubscribed non-brokered private placement of CAD$3.4 million.

Under the Spotlight – Brett Matich, CEO Max Resource and Brazil Iron Ore

Mercado Minerals Ltd. (CSE:MERC)

Mercado Minerals has gained two high-grade silver projects in Sinaloa State, Mexico, having signed and executed a definitive share purchase agreement dated Sept. 26, 2025, to acquire all of the outstanding shares of Concordia Silver.

The properties, Copalito and Zamora, are both located along the western side of the Sierra Madre Occidental, a world-class mining district hosting many silver and gold deposits.

According to the company, the Copalito Project presents a district-scale opportunity with known and drilled silver-gold, low-sulfidation vein mineralization that is open for expansion.

Under the terms of a June Letter of Intent (LOI) with Concordia, Mercado will acquire an option to purchase seven concessions covering 2,820 ha. Six known veins have a cumulative strike length of over 8 km.

The Zamora Project and surrounding area presents district-scale potential that, according to historical reports, has never been drilled.

Under the terms of the LOI, Mercado will acquire four concessions covering 378 ha, which covers small-scale historical underground production at Campanillas, and the right to potentially bring another 2,999 ha of concessions back into good standing with the government, thereby securing title. If successful, Mercado will own a total of 3,377 ha covering a cumulative strike length of over 8 km of structures with 14 historical high-grade silver gold mines on them.

Orestone Mining Corp. (TSXV:ORS)

Orestone’s property portfolio includes exposure to gold, silver and copper in Canada and Argentina. Two of its three projects at the drill-ready stage: Captain in north-central British Columbia and Francisca in Salta province, Argentina.

Its near-term objective on the Francisca property is to define an oxide gold deposit mineable by open-pit methods using low-cost heap leach gold recovery. The company’s 100%-owned Captain Gold-Copper Project hosts a large, gold-dominant porphyry system that is permitted and ready to drill.

Orestone’s near-term plans are to do more mapping and some resampling of the trenches. A recent check assay program revealed a lot of 4-6-gram material on surface, and they’ve planned where the first drill holes are going to be, but Hottman says they need to do a bit more confirmation before they start drilling.

In September Orestone said it expanded Francisca to 9 square km.

Orestone has filed an amended Notice of Work (NOW) permit for an additional 23 drill locations at its Captain gold-copper porphyry property in BC. Drilling is anticipated in the first quarter of 2026.

A non-brokered private placement for up to $2 million at $0.08 per unit was announced on Oct. 14. Crescat Capital took down $232,000 of the financing, thereby maintaining its 11.64% ownership of ORS.

Orestone planning to drill Francisca in Q3/Q4, Captain in Q1 2026 — Richard Mills

Under the Spotlight – with David Hottman, CEO, Orestone Mining

Rackla Metals is targeting Reduced Intrusion-Related Gold Systems (RIRGS) mineralization on the southeastern part of the Tombstone Gold Belt in Canada’s eastern Yukon and western Northwest Territories.

The Vancouver-based company started its 2025 drill program in mid-July at the BiTe Zone on the Grad property in the NWT. The original goal of 4,000 meters was upsized to 5,000m due to encouraging observations in the drill core and surface work.

Rackla is run by one of the legends in the gold mining business, Chief Executive Simon Ridgway, who founded Fortuna Silver, Radius Gold, and is also the CEO of Volcanic Gold.

The goal is to find something as significant as Snowline Gold’s Valley deposit. Valley is about 160 km from Grad and contains 7.94 million oz. gold in the measured and indicated category and 0.89 million oz. in the inferred.

While Rackla has not yet seen visible gold, which helps companies target drill holes and is characteristic of Snowline’s Valley and some other RIRGS deposits, this doesn’t discourage Ridgway, who says bismuth is a sponge for gold and they are finding lots of bismuth in the veins and disseminated in the intrusive.

On Sept. 8, RAK announced that it has completed drilling at the BiTe showing, and that it has made a new discovery from surface sampling on the Manta intrusion, 2 km south of BiTe.

Assay results from the first three holes were reported on Oct. 6, with seven more holes still to come.

Video – Rackla Metals: A Legend’s Gold Discovery Story

Silver47 Exploration Corp. (TSXV:AGA)

Silver47’s flagship Red Mountain property in Alaska has 168 million ounces of silver-equivalent in a Jan. 12, 2024, resource estimate.

AGA also gained a handful of highly prospective new properties through a recent merger with Summa Silver.

According to the news release, the combined company will become a premier high-grade silver focused explorer and developer with a portfolio of silver-rich projects in the United States (Alaska, Nevada and New Mexico).

Collectively, mineral resources amount to approximately 10Moz silver-equivalent (AgEq) at 333 g/t AgEq of indicated mineral resources and 236Moz AgEq at 334 g/t AgEq inferred. The merger was completed on Aug. 1.

On June 18, AGA commenced its fully funded drill program at the Red Mountain VMS Project; 4,000 meters was planned to boost Silver47’s high-grade silver and critical minerals.

AGA’s most interesting new project, Mogollon, is a continuation of the big vein systems found in Mexico and is thought to be one of the biggest epithermal vein systems in the western United States.

Mogollon has shown good results to date, for example 31 meters at 448 grams per tonne silver-equivalent, and 23.2m @ 433 g/t AgEq.

On Oct. 1 AGA announced the completion of its summer drill program at Red Mountain. High-grade assays from the first batch of holes were reported on Oct. 15; assays are pending for the remaining eight holes.

The company also announced that it has drilled multiple new silver-gold veins east of the Ruby discovery at its Hughes Project in Nevada.

Under the Spotlight – Galen McNamara, CEO, Silver47

Silver North (TSXV:SNAG, OTCQB:TARSF)

Silver North’s primary assets are its 100%-owned Haldane Silver Project in Canada’s Yukon Territory (next to Hecla Mining’s Keno Hill Mine Project) and the Tim Silver Project (under option to Coeur Mining), located on the Yukon side of the Yukon-British Columbia border.

Silver North in mid-August started drilling its flagship Haldane Silver Project. According to the company, initial plans outlined 10 holes from four drill sites, totaling approximately 2,500 meters of drilling.

“The focus of the 2025 program is to expand upon the discovery made at the Main Fault last year,” Silver North’s President and CEO Jason Weber said in the Aug. 15 news release.

In just eight drill holes Silver North made three discoveries, out of the 16 holes Silver North has drilled at Haldane — a phenomenal success rate for an early-stage junior.

SNAG thinks drilling this year is going to, at the very least, achieve clear visibility towards attaining a 30-million-oz regular Keno deposit.

As of Oct. 15, six holes were completed at the Main Fault target. Of these, five holes have been sampled and sent for analysis, with one in progress. The goal is to delineate the down-dip and strike potential of the 2024 Main Fault discovery, where three stacked high-grade silver-bearing veins were intersected within a structural zone that returned 28.36m (true width) of 130 g/t silver, 0.09 g/t gold, 0.55% lead and 0.52% zinc.

Silver North drilling flagship Haldane — Richard Mills

Under the Spotlight – Jason Weber, CEO, Silver North

Storm Exploration is a Canadian mineral exploration company focused on advancing four district-scale gold projects in northwestern Ontario: Miminiska, Gold Standard, Keezhik and Attwood.

Three of Storm’s properties are in the Fort Hope area, home to a greenstone belt with the potential to host a major gold camp.

Miminiska has seen the most drilling, making it the obvious choice for an initial drill program. High-grade gold has been confirmed by drilling at a number of locations, with mineralization hosted in Banded Iron Formation (BIF).

The property has two BIF-hosted gold targets separated by 12 km: Miminiska in the west and Frond in the east. While drilling has been done on Miminiska, the Frond target also boasts compelling historical drill results, including 12.54 g/t over 3.8m. In addition, limited exploration drilling in the 1980’s identified gold bearing BIF between Miminiska and Frond, making the entire property prospective for this type of rich gold deposit.

CEO Bruce Counts describes the Miminiska target as “folded into a Z pattern with the best gold results along the northern limb. What we found is that similar conductivity signatures exist elsewhere along that northern limb and into the nose of a fold.

“We have a lot of conviction that we’ll be able to expand the gold along that arm and into the nose which will allow us to grow the gold inventory very quickly,” Counts said on drilling Miminiska.

Torr Metals, headquartered in Vancouver, British Columbia, is focused on advancing its 100%-owned copper-gold porphyry and orogenic gold projects across Canada.

The 332-square-kilometer Kolos Copper-Gold Project (including the 57-square-kilometer Bertha property strategically optioned in March 2025 for full ownership) in BC contains Nicola Belt geology along trend and with similar attributes to alkaline and calc-alkaline copper ± gold ± molybdenum porphyry mines at Copper Mountain, Highland Valley and New Afton.

The project is adjacent to Highway 5, the Coquihalla Highway, with year-round access and operation potential via forestry service roads and substantial infrastructure provided by the city of Merritt located 23 km to the south. The project contains 16 historical copper and gold occurrences, the majority never drill-tested.

In total, Torr has identified four undrilled copper-gold porphyry targets at Kolos — Sonic, Bertha, Kirby and Lodi — with surface geochemical anomalies covering a combined 11.8 km². Bertha, Kirby, and Lodi are fully drill-permitted, while Sonic is in the permitting phase.

On Oct. 15 Torr announced it has started drilling the Bertha target. The inaugural drill program at Kolos is slated for 1,500 meters, and is designed to test the 900m by 500m moderate-to-high chargeability induced polarization (IP) anomaly.

The company also said it increased the size of its previously announced non-brokered private placement, from aggregate gross proceeds of up to $2.8 million, to aggregate gross proceeds of up to $4.57 million.

Under the Spotlight – Malcolm Dorsey, CEO, Torr Metals

White Gold Corp. (TSXV:WGO, OTCQX:WHGOF)

White Gold Corp is the largest landholder in the Klondike Gold District of Canada’s Yukon Territory, with a portfolio of 15,364 quartz claims across 21 properties, covering approximately 30,000 hectares or 3,000 square kilometers.

This represents about 40% of the Yukon’s White Gold District, which first came to the attention of resource investors during the White Gold area play of 2010, and is emerging as one of the most important new gold camps in Canada, rivaling those such as Val d’Or and the Abitibi.

Its flagship White Gold Project hosts four near-surface gold deposits: Golden Saddle, Arc, Ryan’s Surprise and VG. Golden Saddle is the best near-term opportunity for White Gold to add ounces to its resource base.

White Gold in August started the second phase of its 2025 exploration program, building on the first phase announced on July 28.

Phase 1 is a continuation of the company’s successful expanded exploration focus beyond gold, targeting critical metals including copper (Cu), molybdenum (Mo), tungsten (W), antimony (Sb) and bismuth (Bi), among others. Click here for the news release

Phase 2 aims to expand the current multi-million-ounce, high-grade gold resource, and enhance the project’s technical understanding for future development. Click here for the news release

On Aug. 21 the company announced a 44% increase in indicated resources to 1.732Moz gold and a 13.4% Increase in inferred resources to 1.265Moz gold. The updated mineral resource was initiated following recent new modeling of the Golden Saddle and Arc deposits.

A $20 million private placement was announced on Sept. 22.

White Gold starts drilling flagship White Gold Project – Richard Mills

Under the Spotlight – David D’Onofrio, CEO, White Gold Corp.

Richard (Rick) Mills

aheadoftheherd.com

Subscribe to AOTH’s free newsletter

Richard does not own shares of White Gold Corp. (TSXV:WGO), Silver47 Exploration Corp. (TSXV:AGA), Rackla Metals (TSXV:RAK), Kodiak Copper (TSXV:KDK).

Richard owns shares of Torr Metals (TSXV:TMET), Storm Exploration (TSXV:STRM), Silver North (TSXV:SNAG), Orestone Mining Corp. (TSXV:ORS), Mercado Minerals Ltd. (CSE:MERC), Max Resource Corp. (TSXV: MAX) and Harvest Gold Corporation (TSXV:HVG).

TMET, WGO, STRM, SNAG, AGA, RAK, ORS, MERC, MAX KDK, GPH, HVG and GGR are paid advertisers on his site aheadoftheherd.com This article is issued on behalf of TMET, WGO, STRM, SNAG, AGA, RAK, ORS, MERC, MAX KDK, GPH, HVG and GGR

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.