Could G1 be the next company that Washington takes a stake in? – Richard Mills

2025.10.10

It’s a question that’s been on my mind as the US government buys into mining companies that are developing critical minerals projects — the goal being to mine, process and sell end products to local industries, thereby bolstering American supply chains and reducing dependence on foreign imports, mostly from China.

On Oct. 7 Reuters confirmed that The Trump administration is ramping up efforts to secure U.S. supply chains for critical minerals and semiconductors by converting federal grants to companies into equity stakes, aimed at reducing reliance on China.

Among the mining and exploration companies linked to the strategic investment push are MP Materials (NYSE:MP), Lithium Americas (TSX:LAC), Critical Metals (NASDAQ:CRML), USA Rare Earth (NASDAQ:USAR), Trilogy Metals (TSX:TMQ), and United States Antimony Corporation (NYSE:UAMY).

MP Materials

In July the Department of Defense entered a public-private partnership with MP Materials, the company running the Mountain Pass rare earths mine in California. Through the deal, the DoD acquired a 15% stake, making it the company’s largest shareholder. Mountain Pass is currently the country’s only rare earths mine and processing facility.

USA Rare Earth

USA Rare Earth is developing a mine in Sierra Blanca, Texas, and a neodymium magnet manufacturing facility in Stillwater, Oklahoma. The latter is expected to enter commercial production in H1 2026.

CEO Barbara Humpton reportedly told CNBC that the company was in close talks with the White House while responding to a question about potential interest in striking a deal with the Trump administration.

Lithium Americas

Lithium Americas is developing the Thacker Pass lithium project in Nevada. According to Yahoo Finance, the administration took a 10% stake as part of negotiations to restructure a $2.26 billion federal loan. The mine is expected to become the largest lithium operation in the Western hemisphere when it comes online in 2028.

Trilogy Metals

Earlier this week, the federal government said it is partnering with Trilogy Metals due to the company’s claims in the Ambler mining district, a remote part of northeastern Alaska.

The company says the Upper Kobuk Mineral Projects (UKMP) consists of a 471,796-acre land package containing state, patented and native lands. The two most advanced projects are the feasibility-stage Arctic copper-zinc-lead-gold-silver volcanogenic massive sulfide (VMS) project, and the Bornite copper-cobalt carbonate replacement project.

By investing $35.6 million, Washington will own 10% of Trilogy. The deal also gives it the option to buy an additional 7.5% of the shares.

Accompanying the investment was a decision to green light the Ambler Road Project, giving access to the mining district and overturning the Biden administration’s move to block the same project last year.

According to Quartz, The area has “one of the largest undeveloped copper-zinc mineral belts in the world and contains extensive deposits of copper, silver, gold, lead, cobalt, and other strategic metals,” it said. The administration claimed there is a “need for access to domestic critical minerals, and there is no economically feasible and prudent alternative route.”

Critical Metals

Trump has previously stated his desire to annex Greenland, despite objections from Greenlanders, the Greenland government, and Denmark, which retains control over foreign policy, security, and currency within the self-governing territory.

The White House has said it is exploring a potential equity stake in Critical Metals, which owns Tanbreez, the largest, rare earths project in Greenland.

While no decision has yet been made, Investing News Network reported that three sources said a possible investment could stem from conversion of a pending $50 million Defense Production Act grant application into an equity position.

United States Antimony Corporation

Last month, United States Antimony Corporation said it secured a five-year contract worth up to $245 million from the U.S. Defense Logistics Agency to supply antimony metal ingots for the defense stockpile.

Used in munitions, batteries, flame retardants and military-grade compounds, antimony has been flagged by defense officials as a vulnerability in the US industrial base, Reuters stated on Sept. 23.

Graphite One (TSXV:GPH, OTCQX:GPHOF) has received significant grants and two letters of interest to provide up to $895 million in loans from the federal government, but Washington has yet to pony up an ownership stake in the Vancouver-based company.

Why this hasn’t happened is a mystery, considering the importance of graphite to lithium-ion batteries and their end uses, especially electrical vehicles and defense-related applications.

Also, Graphite One could play a crucial role in breaking US dependence on China for graphite imports.

Importance of graphite

A mineral found in metamorphic and igneous rocks; graphite is formed when carbon is subjected to high temperature and pressure in the Earth’s crust. Graphite is also one of the naturally occurring forms of crystalline carbon. It has a black or sometimes greyish color.

Graphite is soft and cleaves easily with light pressure. It is greasy and features low specific gravity.

Due to its natural strength and stiffness, graphite is an excellent conductor of heat and electricity. It is also stable over a wide range of temperatures.

Graphite is chemically inert, meaning it is not affected by a majority of reagents and acids.

Graphite is found all over the world in its natural form and in high quantities. It is usually classified into three forms — flake, crystalline, and amorphous — depending on the source of the mineral. (BYJU’S)

Graphite is ideal for defense purposes thanks to its unique ability to withstand high temperatures. It can be found in aircraft, helicopters, ships, submarines, tanks, infantry fighter vehicles, artillery and missiles.

A report from the Hague Centre for Strategic Studies found that natural graphite and aluminium are the materials most commonly used across military applications and are also subject to considerable supply security risks that stem from the lack of suppliers’ diversification and the instability associated with supplying countries.

The report says aluminum and natural graphite are the two most used materials in the defence industry and can be found in aircrafts (fighter, transport, maritime patrol, and unmanned), helicopters (combat and multi-role), aircraft and helicopter carriers, amphibious assault ships, corvettes, offshore patrol vessels, frigates, submarines, tanks, infantry fighter vehicles, artillery, and missiles. These materials are used in components such as airframe and propulsion systems of helicopters and aircrafts as well as onboard electronics of aircraft carriers, corvettes, submarines, tanks, and infantry fighter vehicles.

The impact of supply disruption would be significant, given the multiplicity of aluminum and natural graphite applications.

The electrification of the global transportation system doesn’t happen without graphite.

That’s because the lithium-ion batteries in electric vehicles are composed of an anode (negative) on one side and a cathode (positive) on the other. Graphite is used in the anode.

The cathode is where metals like lithium, nickel, manganese and cobalt are used, and depending on the battery chemistry, there are different options available to battery makers. Not so for graphite, a material for which there are no substitutes.

Graphite is the largest component in batteries by weight, constituting 45% or more of the cell. Nearly four times more graphite feedstock is consumed in each battery cell than lithium and nine times more cobalt.

Needless to say, graphite is indispensable to the EV, drone, portable electronics and robotics supply chain.

Besides being integral to electric car batteries, graphite is used in pencil lead, lubricants and repellants, paints and refractories.

The mineral is also found in a wide range of consumer devices, including smartphones, laptops, tablets and other wireless devices, earbuds and headsets.

Import dependence

Graphite is:

- One of 14 listed minerals for which the US is 100% import dependent.

- One of nine listed minerals meeting all six of the industrial/defense sector indicators identified by the US government report.

- One of four listed minerals for which the US is 100% import-dependent while meeting all six industrial/defense sector indicators.

- One of three listed minerals which meet all industrial/defense sector indicators — and for which China is the leading global producer and leading US supplier.

China is by far the biggest graphite producer at about 80% of global production. It also controls almost all graphite processing, establishing itself as a dominant player in every stage of the supply chain.

China accounts for 98% of announced anode manufacturing capacity expansions through 2030, according to the International Energy Agency.

The Asian nation also controls 80% of synthetic graphite production, which currently dominates the market over natural graphite. Synthetic graphite’s primary application is in the graphite electrodes used for electric arc furnace steelmaking, which accounts for 70-80% of graphite electrode consumption.

China has imposed restrictions on Chinese graphite exports. Exporters must apply for permits to ship synthetic and natural flake graphite.

Note that while export restrictions have been eased by China on rare earths, they remain in place for graphite.

The United States currently produces no graphite and therefore must rely solely on imports to satisfy domestic demand. Primary sources are China, Mexico and Canada.

Impending shortage

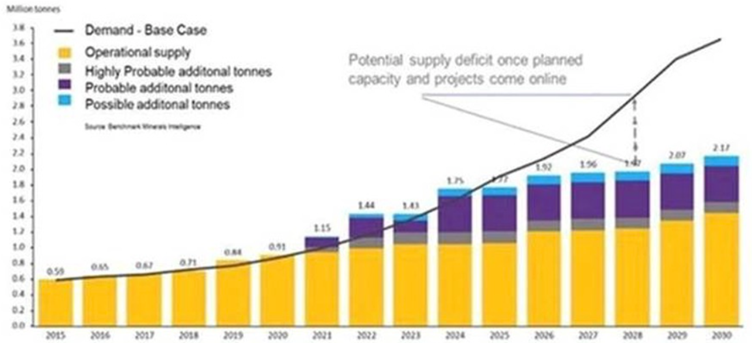

BloombergNEF expects graphite demand to quadruple by 2030.

The International Energy Agency (IEA) goes 10 years further out, predicting that growth in graphite demand could see an 8- to 25-fold increase between 2020 and 2040.

Given that demand for graphite is accelerating at a rate never seen before, the impending supply crunch could get serious.

Analysis by Benchmark Mineral Intelligence projects that natural graphite will have the largest supply shortfalls of all battery materials by 2030 — even more than that of lithium — with demand outstripping expected supplies by about 1.2 million tonnes.

And this is just counting EV battery use only; the mining industry still needs to supply other end-users. The automotive and steel industries remain the largest consumers of graphite today, with demand across both rising at 5% per annum.

BMI previously stated that flake graphite feedstock required to supply the world’s lithium-ion battery anode market is projected to reach 1.25 million tonnes per annum by 2025. For reference, the amount of mined graphite for all uses in 2024 was 1.6 million tonnes.

BMI has also said up to 97 average-sized graphite mines need to come online by 2035 to meet global demand.

Graphite One

The US has no security of supply for graphite. It has clearly reached a point where much more graphite needs to be discovered and mined IN THE US.

Fortunately, a large graphite mine is under development, along with a planned graphite anode manufacturing plant, for all lithium batteries across all applications, in Voltage Valley, Ohio.

Graphite One could supply a significant portion of the graphite demanded by the United States.

Consider: In 2024, the US imported 60,000 tons of natural graphite, of which 87.7% was flake and high purity. (Source: USGS)

Based on G1’s Feasibility Study (FS), released in April, the Graphite Creek mine in Alaska would have capacity to produce 175,000 tonnes of graphite concentrate per year during its projected 20-year mine life — a production rate triple that of two years ago.

This means Graphite One could have the capacity to not only meet the US’s annual graphite needs, but have extra to stockpile, in the neighborhood of 100,000 tonnes each year. This additional graphite could be put to domestic usage or built up to accommodate future demand growth.

US achieves security of graphite supply with G1 Feasibility Study – Richard Mills

Located on the Seward Peninsula, the Graphite Creek property comprises 9,600 hectares of State of Alaska mining claims. The claim block consists of 176 claims. G1’s deposit is entirely on state land.

The graphite zone is exposed on the surface and strikes east/northeast along the north face of the Kigluaik Mountains. The FS pit and mineral reserve and resources footprint represents just 1.9 km of the 15.3-km-long electromagnetic anomaly (Figure 1).

electromagnetic (EM) survey anomaly.

Indeed, there is plenty of expansion potential to drill for and include more graphite in the resource calculation, which currently sits at 4.796 million tonnes of graphite contained in the 104.7Mt measured and indicated resource graded at 4.6% Cg.

cut-off grade.

Graphite Creek in early 2021 was given High-Priority Infrastructure Project (HPIP) status by the Federal Permitting Improvement Steering Committee (FPISC). The HPIP designation allows Graphite One to list on the US government’s Federal Permitting Dashboard, which ensures that the various federal permitting agencies coordinate their reviews of projects as a means of streamlining the approval process.

Alaska Governor Mike Dunleavy noted in his 2025 State of the State address, “subject to securing project financing, construction could begin by 2027, and the mine could be producing as early as 2029.”

Shows of support

Graphite One in September received another show of support from the U.S. Export-Import Bank (EXIM) in the form of a USD$570 million Letter of Interest (LOI) to develop the company’s Graphite Creek mine in Alaska.

GPH announced that EXIM has extended a non-binding LOI for up to $570M to advance the mine. This is on top of EXIM’s $325M non-binding LOI in 2024, for the construction of the company’s Ohio-based anode manufacturing plant.

Total EXIM support now reaches a potential USD$895 million (CAD$1,230,759,250); that’s almost a billion dollars of potential funding towards accomplishing G1’s plans for a circular economy of mine to battery to EV for the US graphite supply chain.

Graphite One announces potential EXIM funding for up to USD$895 million – Richard Mills

Two Department of Defense grants have been awarded to Graphite One, one for $37.5 million – paying 75% of the cost of the Feasibility Study, the other for $4.7 million — the latter to develop an alternative to the current firefighting foam used by the US military and civilian firefighting agencies, using graphite sourced from Graphite Creek.

In addition, G1 qualifies for federal loan guarantees worth $72 billion.

On June 3 it was announced that the Graphite Creek project in Alaska — the upstream anchor for Graphite One’s complete US-based graphite supply chain — was accepted as a “covered project” on the US government’s “FAST-41 Permitting Dashboard”.

Graphite Creek is the first Alaskan mining project to be listed on the dashboard.

FAST-41 streamlines the permitting process by providing improved timeliness and predictability by establishing publicly posted timelines and procedures for federal agencies, reducing unpredictability in the permitting process. FAST-41 also provides issue resolution mechanisms, while the federal permitting dashboard allows all project stakeholders and the general public to track a project’s progress, including periods for public comment.

Graphite One has received strong support from the US government for developing its “made in America” graphite supply chain anchored by Graphite Creek, the largest graphite deposit in the country and one of the biggest in the world.

Graphite One plans to develop a “circular economy” for graphite. Its supply chain strategy involves mining, manufacturing and recycling, all done domestically — a US first.

Subject to financing, the company plans to invest $435 million to build a graphite product manufacturing plant in Trumbull County, Ohio, between Cleveland and Pittsburgh. The plant would produce Active Anode Materials (AAM), first using synthetic graphite, and then, once the Graphite Creek mine is in production, using natural graphite.

President Trump has signed several executive orders of relevance to Graphite One and Graphite Creek.

Regarding Trump’s March 20 executive order, Graphite One said it welcomes the EO, titled “Immediate Measures to Increase American Mineral Production.”

“This new Critical Minerals Executive Order serves as the strongest signal yet that the U.S. Government has not only recognized the national security need for critical minerals including graphite, but that there will now be a ‘whole of government’ engagement to accelerate domestic development,” Graphite One’s CEO Anthony Huston said.

The Critical Minerals EO follows three executive orders issued by President Trump on his first day in office: “Declaring a National Energy Emergency,” “Unleashing American Energy,” and “Unleashing Alaska’s Extraordinary Resource Potential” referenced in the Jan. 23 Graphite One press release.

Alaska senators, Alaska’s governor, and the Bering Straits Native Corporation all support the project. In 2023 G1 closed a $2 million private placement from BSNC to support development of the company’s Graphite Creek deposit.

Just this week, Graphite One announced a second strategic investment from two native corporations, Doyon Limited and Aleut, for aggregate gross proceeds of $5 million (approx. CAD$7 million).

The investment is in the form of a non-brokered private placement of 8,514,024 units at CAD$0.82 per unit.

The funds will be used to conduct environmental studies and other permitting-related activities on the Graphite Creek property.

“All of us at Graphite One are grateful for these investments from Doyon and Aleut Corp, joining Bering Straits Native Corporation, which made its strategic investment in G1 in 2023. We are pleased and honored to be the first Critical Mineral project to have direct investment from three Alaska Native Regional Corporations,” Huston said in the Oct. 6 news release. “We greatly appreciate the trust placed in us through these partnerships, together with your support, seek to make Graphite Creek a model of responsible development that brings long-term benefits to your communities and the State of Alaska.”

Conclusion

The Trump administration has made several recent investments in critical minerals projects throughout the country. Among the minerals being explored for by the five companies listed above (a sixth, MP Materials, is a producer), are rare earths, lithium, copper-zinc-lead-gold-silver VMS, a bornite-copper-cobalt carbonate replacement deposit (CRD), and antimony.

To us at AOTH, it would make perfect sense for graphite to be the next “mineral du jour” served on a gilded plate by the White House.

Graphite is a highly critical mineral because of its essential role in electric vehicle batteries, energy storage and defense applications, with demand projected to rise dramatically.

In the event of a mineral shortage, the US could not depend on its closest allies for critical raw materials. NATO has limited mineral production. The European Union imports between 75% and 100% of most metals it consumes, and neither the EU nor its member countries have mineral stockpiles. Nor do Canada or Great Britain.

The United States does not currently produce any graphite; most of it is imported from China.

Deficits are expected to kick in as early as this year, as new graphite mines fail to keep up with surging demand from automakers.

Some of the world’s largest auto and battery makers aren’t waiting until that happens. They, and the US government, are racing to secure graphite supplies ahead of a coming supply shortage.

Tesla (NASDAQ:TSLA) and Panasonic are among the companies that have signed graphite offtake agreements. Syrah Resources (ASX:SYR) has an offtake with Tesla to ship graphite from its mine in Mozambique to a processing facility in Louisiana.

BMI has said as many as 97 graphite mines need to come online by 2035 to meet global demand. That’s about eight new mines a year.

But Graphite One has stepped into the breach.

G1 could have the capacity to not only meet the US’s annual graphite needs but have extra to stockpile. Its recently released Feasibility Study triples the Graphite Creek mine’s annual capacity to 175,000 tonnes per year. In 2024, the US imported 60,000 tons of natural graphite.

Unfortunately, the White House does not seem to recognize the enormity of Graphite One’s accomplishment — i.e., single-handedly eliminating US dependence on China for graphite imports.

When it does, G1 could, and should, we at AOTH believe, be the next junior resource company to be on the receiving end of the government’s largesse.

Graphite One Inc.

TSXV:GPH, OTCQX:GPHOF

2025.10.08 Share Price: Cdn$1.38

Shares Outstanding: 146.2m

Market cap: Cdn$222.2m

GPH website

Richard (Rick) Mills

aheadoftheherd.com

Subscribe to AOTH’s free newsletter

Richard owns shares of Graphite One Inc. (TSXV:GPH). GPH is a paid advertiser on his site aheadoftheherd.com This article is issued on behalf of GPH.

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.

{kind=link}

{kind=link}