Under the Spotlight – Brett Matich, CEO Max Resource and Brazil Iron Ore

Rick Mills, Editor/ Publisher, Ahead of the Herd:

Let’s talk about Sierra Azul first. Max still owns 100% of the Sierra Azul copper-silver project in Colombia. Max has an Earn-In Agreement (“EIA”) with Freeport-McMoRan Exploration Corporation (“Freeport”), a wholly- owned affiliate of Freeport-McMoRan Inc. (“NYSE: FCX”) relating to the Sierra Azul Project.

Under the terms of the EIA, Freeport has been granted a two-stage option to acquire up to an 80% ownership interest in the Sierra Azul Project by funding cumulative expenditures of C$50 million and making cash payments to Max of C$1.55 million.

RM: Where are we with the project today, please bring us up to date.

Brett Matich, CEO, Max Resource Corp.

The budget in 2024 was US$4.2 million, the budget for this year is US$4.8 million.

In relation to exploration, [Senior Technical Consultant] Bruce Counts is heading to Colombia and we’re waiting to see when we’re getting the next lot of assays come through. We’re going through a process in relation to drilling approval. We’ve got to go through those steps, we’re targeting 2025-year end to Q1 2026 for drilling.

RM: Okay, can you tell us about the results at AM currently? What have we found and what it is?

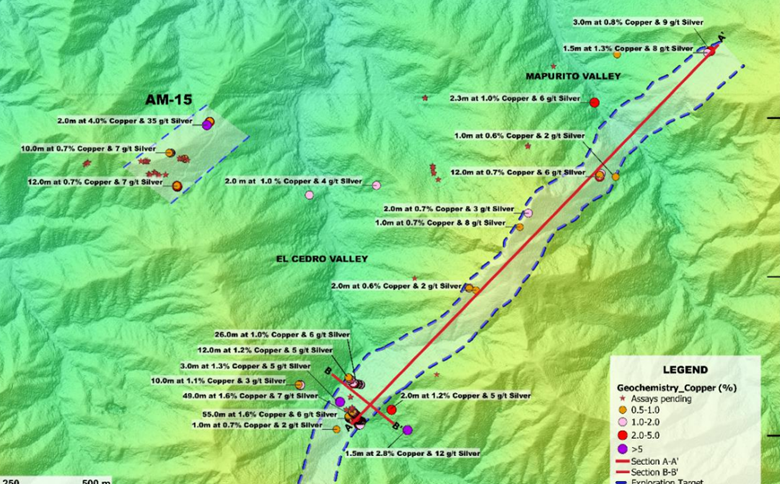

BM: As reported, the mineralization and alteration at AM-153 has been extended to over 1,500m long and 100m wide and is similar to deposits in the Tocopilla – Taltal region of northern Chile, a mineralized corridor that extends well over 100-km and hosts several economic deposits including Mantos Blancos (500 Mmt at 1.218% Copper and 12 g/t Silver – Rick).

Our second major discovery is AM-15 which is running parallel to AM-13. The new discovery, AM-15, is located about 1,000m northwest of AM-13. Early work suggests a large target footprint with five mineralized outcrops already identified over 100m by 300m and it is open in all directions. Exploration updates on AM-13 and AM-15 are due soon.

At Conejo located 30-km south of AM-13 is a high priority target with extensive mineralization. Mineralized outcrops have been discovered over 3.7-km at the primary target area. Surface samples averaged 4.9% copper (with a 2% cut-off). The two main areas are 1.3 kilometers apart and there’s been no exploration done in that 1.3 km. We anticipate that the regional geochemistry campaign will develop further targets, preliminary results are due soon.

RM: There is a manto expert from Chile working in Colombia on the project now?

BM: We’ve had site visits with manto experts, and we have someone there now who is an expert in this type of mineralization so we’re getting a lot of not just financial support but technical support from Freeport.

We haven’t forgotten about URU. We don’t just want to look at URU targets, we also plan to go back where we did our first drilling, those results were very positive.

RM: I thought our drill program in URU had good results. Over 2,200 meters of drilling in 12 holes, and 50% of them intersected significant mineralization.

BM: Yes, and we have gathered a lot more data; they’re gaining more knowledge of the geology from the regional sampling programs as well as the airborne survey. This was all unknown at the time of the drilling.

RM: Yes, they weren’t blind drill holes, but we certainly didn’t have the amount of knowledge back then that we do now.

BM: Correct.

RM: Let’s get into Max’s Florália DSO Project which is being put into a new company called Max Iron Brazil currently planning an IPO on the Australia Stock Exchange (ASX). So, you found an iron ore project, now it’s not just iron ore project but a DSO project, a Direct Shipping Ore project, hematite. You acquired this project in Minas Gerais, Brazil. Why is Minas Gerais one of the largest iron ore-producing areas in the world and why is Brazil so high up on everybody’s radar?

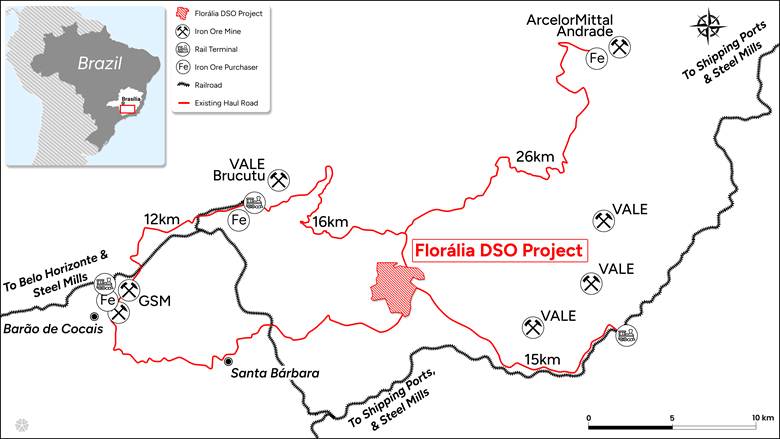

BM: Well, Brazil and Australia are the world’s largest producers of iron ore including DSO. Minas Gerais is where the large iron ore mines originally started and in conjunction there was a steel industry that was built there. Vale owned Brutucu is the largest iron ore mine in Minas Gerais located 10 km north of the Florália DSO project.

After that was the discovery of the Carajas iron ore region in the far north. In Carajas the DSO iron ore is predominantly exported. To bring it down to Minas Gerais has challenges, there’s no direct rail network available, so the steel mills in Minas Gerais are always looking to purchase local Direct Shipping Ore. Most the large mines have mined all the surface DSO, which is the higher grade of their deposits, so it’s not just the steel mills that are looking for the higher grade material but also the mature iron ore mines that are looking for the high grade for blending.

Florália DSO has the potential of producing hematite direct shipping ore (DSO), the friable hematite allows for free-dig (no blasting) open pit, low-cost dry processing, by crush, screen and dry magnetic separation. The privately owned GSM iron ore mine (17 km west) is free dig which saves conducting drilling and blasting, followed by crushing and screening to produce DSO that is trucked 20-km to Vale.

In relation to where we are, there is an existing 16 km road to Vale who purchase all of GSM’s DSO.

There is also an existing 26 km road to ArcelorMittal, and they are also buying DSO for blending. In addition, there is an existing 15 km southern road to a railway terminal. We’re in a position where we don’t have to depend on one company as a purchaser.

RM: Can you explain what blending is for our readers, what are they doing with the ore?

BM: What they do is they blend DSO with their production ore. A lot of their production ore is in the 30-40% range so they blend it to get the grade up. That’s part of their operation so they can utilize lower grades.

Trafigura have a dedicated iron ore port which can ship 50 million tonnes a year. They have spare capacity of over 20 million tonnes, so we could see DSO demand from the overseas market as well.

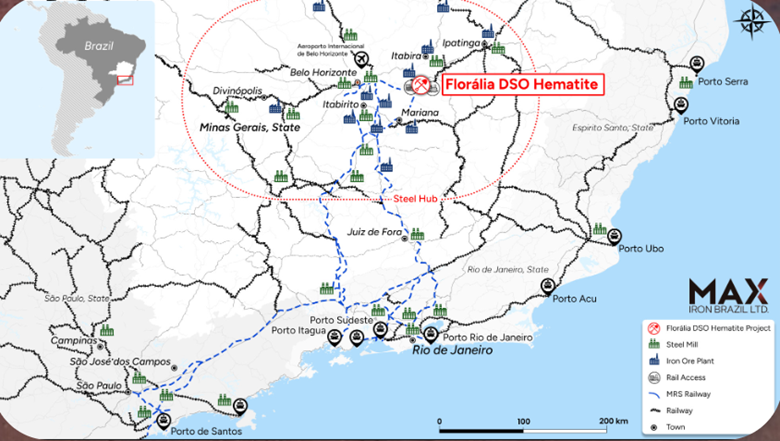

RM: When you compare an operation similar to Florália DSO that we’re envisioning in Minas Gerais, we’ve compared it to a lot of operations in Australia and the advantages are quite apparent when you think about everything you just said. Can you go over the advantages of being where Florália DSO is, versus say one in Australia?

BM: Western Australia produces almost all of the iron ore coming out of Australia. That’s an export market predominantly targeting Japan and China, but the rail networks are held predominately by the majors which are Rio Tinto, BHP, FMG, you’ve also got Hancock.

So, what’s happening with the deposits is, if you haven’t got rail access you have to truck it. If you’re within 100 kilometers and have shipping port access it likely works. The juniors tend to be between 200 and 500 kilometers by road, so the cost of delivering ore to the port in most cases is over 50% of their production costs. That’s the issue they’ve got there.

Whereas where have existing roads connected to established iron ore buyers Vale (16 km), ArcelorMittal (26 km), and the railway terminal (15 km), so that’s the game changer.

RM: What about a junior that has recently made it into production, what are their transportation costs?

BM: Fenix Resources is in production in Western Australia. They started off with as little as 7 million tonnes in reserve and they’re quite successful, but again they’re haulage cost is well over 60% and their market cap is around $230 million.

RM: So, let’s get into Floralia and talk about the deposit and how much we’ve been able to grow it since owning it.

BM: Max’s technical team has significantly expanded the Florália hematite Exploration Target ranging from 8 to 12 million tons at 58% Fe, upgraded to 50 to 70 million ton at 55%-61% Fe in early 2025.

We’re just finishing the maiden drilling campaign and we’re putting all the data together and modeling it to update the Exploration Target, of course under Australian reporting rules, JORC.

We just concluded dry magnetic separation study which was extremely successful as outlined in Max’s news release dated April 22, 2025.

So, we’re completing the upgraded Exploration Target and the independent geological model. We’re aiming in the next two weeks to get a chunk of that information out to the market.

RM: What are our plans for the rest of the year and into 2026?

BM: The rest of the year the plan is to complete the IPO and based on listing the IPO we have a two-year plan to complete a feasibility study and have all mining approvals and be ready to start development.

RM: Brett what are Max Resource highlights, reasons to invest, for investors?

BM: Well, the highlights for investors are in relation to the planned ASX listing of Max Iron Brazil, 100% owner of Floralia iron ore project. On listing, Max would be the largest shareholder.

In relation to Colombia, we are conducting an aggressive 2025 exploration program on Max’s 100% owned Sierra Azul Copper Silver project, and we plan to update the market shortly. We are also moving closer to achieving drilling approvals.

RM: Concerning Max Iron Brazil how could Max take part in a future financing, after the IPO, if one is ever needed?

BM: There are options, potentially get the offtake buyers to support a financing. That’s not uncommon.

There’s also debt as well so there’s two things where you don’t necessarily have to raise through issuing equity and it’s something that we do keep in mind when we’re talking to offtake partners. But to get signed offtake agreements you must be at a stage where we’ve got a resource put together.

RM: Was there anything else you wanted to say Brett?

BM: No that’s about it.

RM: Thanks Brett.

Richard (Rick) Mills

aheadoftheherd.com

Subscribe to AOTH’s free newsletter

Richard does own shares of Max Resource (TSX.V:MAX). MAX is a paid advertiser on his site aheadoftheherd.com

This article is issued on behalf of MAX

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.

Not impressed. So far I have lost over 90%of my investment. The stock continues to languish about 4 cents

Nice to finally see some information from MAX. The news has been very quiet and the share price is in the tank. It was looking very positive until the Freeport Agreement was announced. The capex at approximately $8 million is ridiculous but they should be able to keep exploring and bringing production up in Brazil with just the capital raise for Brazil. Shares outstanding in MAX should stay around the 200 million mark so share appreciation should materialize. Extreme patience seems to be the order of the day. Thanks for putting this together.