Under the Spotlight – Quinton Hennigh CEO San Cristobal

2026.06.13

Rick Mills, Editor/ Publisher, Ahead of the Herd:

I thought we’d talk a few copper stocks, one uranium and a manganese. Kind of get off the beaten path of gold and silver a little bit.

We’ve both been highly long-term bullish on copper, and we’ve predicted much higher prices due to growing structural deficits, soaring data center and AI demand, and a lack of new, economically viable mining projects.

Incentive prices, even if copper is now $12,000 a tonne, research has shown that they’re still too low to justify the massive capital costs required to build new mines.

Miners require an incentive price well above $12,000, $15,000 a tonne has been thrown around by a few people. The AI and the grid surge demand is exploding due to the rapid build-out of hyperscale data centers. These facilities are extremely copper-intensive.

I was reading they require, for the medium-sized ones, 50,000 tonnes of copper per facility. This increasing demand is all in the face of structural shortages. The decades of underinvestment and declining ore grades mean that supply will permanently lag behind increasing global demand.

I think it’s a good thing here today for us to be talking about copper.

Quinton Hennigh, CEO, San Cristobal Mining:

Look, I don’t have a large number of stats like you just rambled off.

I know a lot of the exploration side and the discovery side, and we haven’t found enough, I’ll call it quality copper deposits. There’s a lot of copper deposits that are in inventory, but we don’t have many copper deposits that are actually economic, that display the economics that justify a great deal of capital to develop these things. If you want to talk about a metal that’s challenging, it’s copper.

These are mostly capital-intensive projects that only big companies can tackle. It’s not something for the junior space, it’s not something for even the mid-tier space. You’ve got to find big deposits that justify spending literally billions of dollars to develop.

Have we found those? Have we found an Oyu Tolgoi recently? Have we found anything that’s worthwhile recently? Not really. It’s shocking. I mean, there’s Filo Corp. Filo’s pretty good. It was bought, look at the premiums. It was nearly a $5 billion takeover.

That’s awesome. But look at who’s developing it, BHP (NYSE:BHP), Lundin (TSX:LUN). You’ve got to have big-boy bank accounts to tackle those things.

RM: It was interesting to note that Coeur (TSX:CDE) came into the Southern Quesnel Trough and bought New Gold, a copper and gold mine, and of course Rainy River, a gold deposit, for $7 billion worth of stock.

That’s showing a hell of a lot of confidence in copper for a premier silver miner.

QH: Yes, it is. And it’s a bet that more companies are probably going to take. I think that future quality copper deposits that come to light are going to see premiums. They’re going to go for very high valuations.

RM: Tell us about Mogotes Metals (TSXV:MOG). I know we talked about it in early 2025, and they’ve discovered high-grade, shallow copper, gold, silver and moly at Filo.

Now, the thing about this Filo is it’s on strike to BHP and Lundin’s Filo del Sur discovery, which is a massive project itself. So, tell us about Mogotes and why you like it.

QH: Well, it’s just what you said. It is part of the same system that Filo’s part of. Basically, Los Mogotes and all the other targets that they have across the property are simply additional porphyry centers that are part of the overall porphyry complex in this district. That in itself is a very good sign.

This is not just a one-off porphyry. This is a cluster of porphyries that clearly each one is generating a world-class copper deposit. Don’t forget, NGEx Minerals (TSX:NGEX) is just north of Filo at BHP’s soon-to-be mine.

They have a couple of massive discoveries as well. So, this is a belt. This is a district-scale, very large, very well-endowed, high-grade copper-gold district.

Mogotes as a company has a very substantial portion of this district. The targets across this, are all of them going to play out? Are all of them going to produce a porphyry? I can’t tell you that. Nobody can until they drill them.

But they sure look very similar to what we see at Filo. The geophysical expression is almost identical. It’s not like they’re a random one-off hit somewhere. This thing is on strike. It looks like it’s actually part of the same structure that introduced the porphyry system.

It’s right next to a project that was bought for nearly $5 billion. So, hopefully they hit a home run here.

They’re drilling this year to see early-stage discovery. I’m going to say the results that they had a few weeks ago were definitely interesting. High-grade copper, gold, it’s better than some of the drilling I remember from Filo. So, let’s hope they’re onto something.

They didn’t get the full-scale discovery. It’s not like we’re going to see a continued run of news releases with very long intercepts of high-grade right now. It’s going to be next year because this year was all about discovery.

They’ve basically got a harpoon into the whale, and now money and horsepower could go at it in a very aggressive manner. I think we’re going to see great things out of Mogotes.

RM: It’s only trading at $0.50, that’s not a bad deal in that neighborhood.

QH: Exactly. Yes, it’s a very good deal.

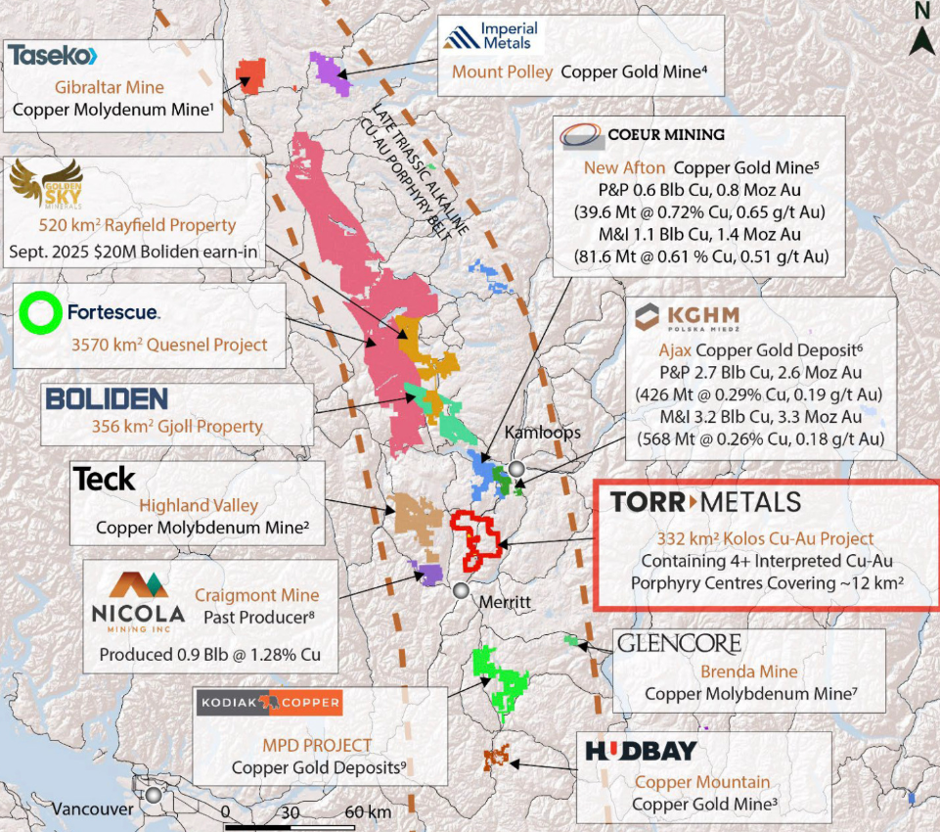

RM: The copper stock I wanted to talk about today is in the Southern Quesnel Trough. The reason I like it is, as I mentioned, Coeur bought New Gold.

But if you look at what’s in the area, Fortescue (ASX:FMG) just staked 300 square kilometers. It’s an incredibly large land package. Boliden’s in there. Teck (TSX:TECK.B), of course, is there. You’ve got Hudbay (TSX:HBM), Glencore (LSE:GLEN), KGHM, Coeur Mining, Imperial Metals (TSX:III) all grouped in this one area. And basically, for a junior to secure any kind of a land package in there is quite a feat.

Torr Metals (TSXV:TMET) has their Kolos Project and they’re going to be starting their first drill campaign imminently. Last year they drilled into Bertha South and proved the system is juiced.

It is native copper, supergene, much like a New Afton-style mineralization. I’m not saying it’s New Afton. I’m saying the style of mineralization with the native copper, the supergene is similar.

Some of the results suggest we’re on top of hypogene. Last years drilling looks like they are in the periphery of the core, the heat engine.

They have a vector, and are going to be drilling Bertha North, where they think the core is. It’s trading around 12 cents, it’s got a decent share structure. And like I said, a discovery in that area could ignite a fire, considering there’s so many mines and mills that need feed.

So that’s one of my picks for investor due diligence. Do you follow Torr Metals at all?

QH: I do. I follow a number of stories in the Quesnel Trough.

There’s a lot of porphyry stories right now that have started to catch attention. I don’t think we’ve seen the appreciation of stories as much as we will as time goes on. I think as more companies do more work, especially with all the names that you rambled off there, seeing that kind of money coming into a district is a very good sign.

It means that these big companies are hungry for a discovery. They want to grab the first thing, the first discovery that’s in sight.

I think strategically, it’s a very good opportunity to invest.

RM: That’s what I’m thinking. There’s some juniors in there that have very nice land positions and have proven that they’ve got copper on it.

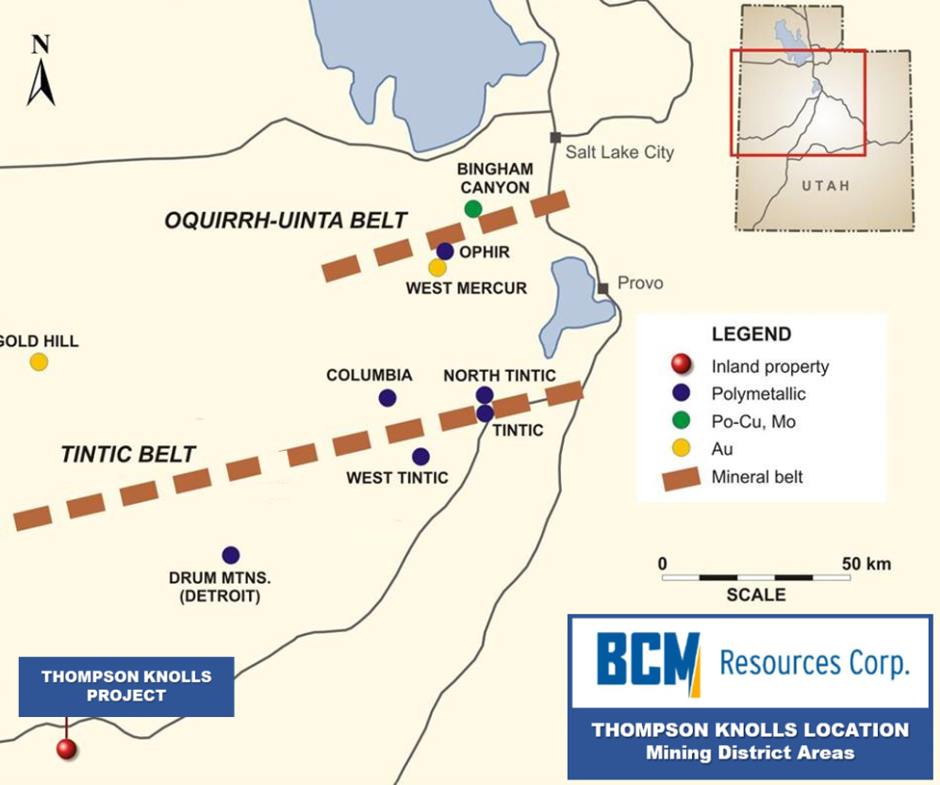

You like BCM Resources (TSXV:B). Now, the stock symbol is not BCM, it’s on the TSX Venture as B, and it’s copper in Utah’s Great Basin. We talked about this earlier in the year.

They drilled two holes. The first hole was down to 1,219 meters, and they just finished their second hole. Can you give us an update on this one?

QH: Yes. This company is run by Sergei Diakov. Sergei is a very famous geologist. He was the man who discovered Oyu Tolgoi in Mongolia.

He worked for BHP. He’s worked for a number of big companies, such as AngloGold Ashanti (NYYSE:AU). Sergei is probably one of the top geologists.

I certainly know, but I think everybody in the geology community would agree. He knows his copper systems. He knows how to chase these things.

He has a very clear perspective on how to explore for them. About five or six years ago, I remember when they first came to us when I was at Crescat Capital, and they proposed an investment. I remember looking at the geophysics and thinking, wow, this is a blind target, but it sure looks compelling.

We invested some money. They drilled a few holes. They did hit interesting mineralization.

It wasn’t a home run by any stretch, but in May of 2023, I think it was, they had an announcement about hole 8, that hit 155 meters of about 0.86% copper-equivalent. It was mostly copper, but there was a bit of gold and a bit of silver and a bit of moly. It was a very nice hit.

Now, it was actually in skarn. It was in the mineralization that would be considered proximal to a porphyry. The question is, what else is there? That in its own right is a discovery hole in my book.

Unfortunately, the market went to heck about that time, and it was just impossible to raise money. Here, the company had a discovery, and they had no ability to follow up. They languished for a while, but back in 2025, just a year ago, I started to work with Sergei.

We did some technical work down at the School of Mines here in Colorado, and we identified some clear vectors where we should be drilling some more holes. I helped Sergei get capitalized again.

We got their balance sheet cleared up, and they’re drilling now, which is a great story. That in its own right is what needs to happen in this mining world right now. Good drill programs run by good geologists.

They’ve drilled two holes. Both core holes look like they’re quite interesting. They’re definitely seeing lots of skarn, from what I can see in the releases.

Have they nailed it? We don’t know what the assays are yet. My hunch is that these holes will have mineralization in them, but I can’t tell you if it’s going to be long and continuous like hole 8. I actually looked at the vectoring, and I think there’s a lot of stuff we’ve got to learn here. One of the things that bugs me about hole 8 was that it ended in mineralization.

In my head, there’s also a vertical vector. Sergei and his team need to look straight underneath hole 8, but that’s a problem we’ll work on. They’ve got plenty of money to keep going.

I think they’re at hole 3 right now. They’re doing coring. We’ll just sit patiently and wait to see what they come up with. You’ve got Bingham to the north, Robinson to the west. This is the world of absolute mega, world-class porphyry systems. This is the hunting ground you want to be in.

RM: You could say that it’s a pretty rich neighborhood to be living in. You discover something there that even sniffs at one of those deposits, people are going to really start paying attention.

You can’t deny Sergei has massive street cred. When you invest in quality management, Sergei is right up there when it comes to copper discoveries. It’s hard to beat.

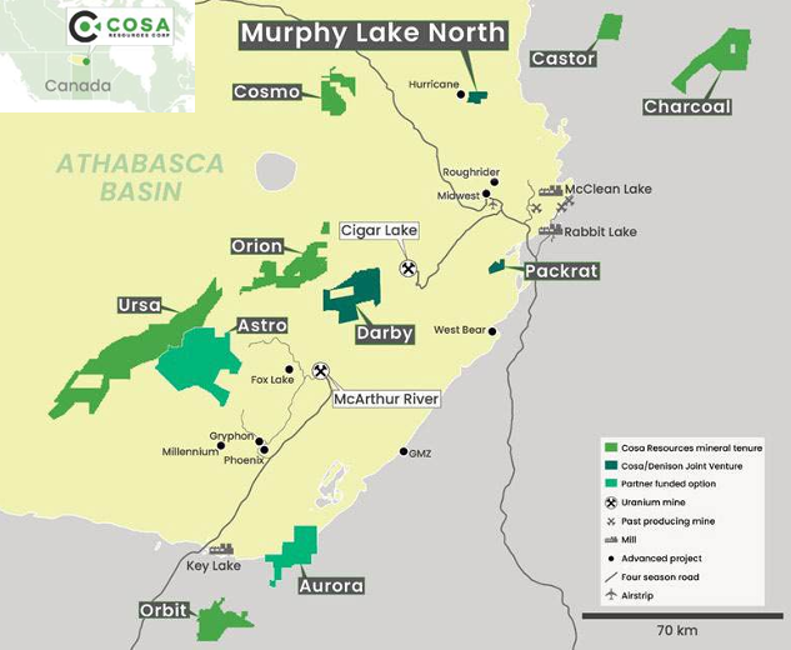

I want to talk about Cosa Resources (TSXV:COSA), it’s the same team — Isoenergy (TSX:ISO) — that discovered the Hurricane deposit. They’ve got a joint venture with Denison (TSX:DML). They took a couple of projects from Denison to work on.

They went out and formed their own company, Cosa, the same guys. This year, they’re concentrating in the Athabasca Basin, high-grade uranium.

Murphy Lake North and Darby are going to be drilled this year. The initial results from both projects are good enough that they have to go back in and drill.

Murphy Lake North is going to be the first to drill. They hit up to 1.75% U3O8 within an interval of 5m of 0.55% U308. Your global average uranium mine is probably less than half of 0.55%. When we’re talking about uranium in the Athabasca Basin, we’re talking about scintillator counts of 15,000 to 30,000. We’re talking +20% U308.

There is definitely Uranium at Murphy Lake North, I think they just missed the big grades by a little bit.

QH: The team’s a great team. They’re known explorers and these guys know what they’re doing. There’s no question.

As soon as I saw some of those radiometric counts in the news release, I can’t remember how long ago it was, I jumped in and bought stock right away. What you said is the key words here. When you see an interval like that that’s great.

In this part of the world, that is what we call a near miss; it’s very near something that’s probably bigger. The Athabasca Basin, if you look at the deposits, they’re actually small, compact.

They usually have some sort of structural control so they can be almost like a sausage. Think of a tiny sausage buried in the ground. These guys are near something.

I am a very strong believer that as they drill a few more holes, they’re probably going to lance one of these cigar-shaped deals in the subsurface.

You can go from being a small market-cap company to hundreds of millions of dollars market-cap very quickly in the Athabasca Basin. I love these stories. These are great outcomes usually.

RM: Uranium stocks are a little bit different than a lot of the stocks that we normally talk about. If you take Iso, when these guys discovered Hurricane, their stock was trading around $0.30 or something, and it went up.

When they hit that high-grade uranium, the world changed for them. They went from a $40 million market cap to a $700 million market cap.

They didn’t even have a resource estimate, an MRE, let alone a PEA. Nothing does that. Uranium, it’s insane what happens.

QH: Well, uranium, but it’s in the Athabasca Basin. I would actually argue that there’s a lot of uranium stores out there, and I don’t touch most of them because they’re low-grade. They’re jurisdictionally challenged.

There’s problems, but in the Athabasca Basin, if you find one of these high-grade deposits, you know it’s going to be in demand. It’s going to be bought, and quite frankly, these things make a lot of money. They’re like finding an uber-high-grade gold deposit.

They’re cash cows, so kudos to these guys. They’re good explorers, and they’re doing the right thing here.

RM: Yes, and the one thing I want to say is because we have these assay results, and we know the scintillator grades, the counts per second, I’m saying they calibrate their scintillators to the assay grades and the counts. The nice thing about these things is you can look at the scintillator counts per second, and you come back to if they have published grades, because they always put out the scintillator counts, and then they do the assays, and you can kind of compare, okay, 30,000 counts per second, based on that, nice high-grade uranium hit, and you can correlate in your mind what you’re getting.

So, you can actually follow almost real-time what’s happening here, and it’s just nice to have that and be in the Athabasca Basin and have Denison as your strategic partner. I think the world is going to be pretty good to Cosa in the future.

QH: I can’t agree more.

RM: You also want to talk about Barksdale (TSXV:BRO), another copper play. They’ve got near-surface hypogene chalcocite targets with a strong silver kicker at their Sunnyside property. Tell us about it.

QH: I’m a director, I’ve got to disclose that, and a shareholder, but look, we have been circling around this whole concept of chasing the extension of Taylor for a long time.

The company has basically been focused on the wrong prize, in retrospect, okay. Now, about two years ago, the geologist that I helped put in charge, Alan Roberts, who I’ve worked with for many years, he brought to my attention this concept of a chalcocite, copper-rich deposit in a shallower environment. And I was like, well, that looks interesting, but what do we know about it? Is there all that much data? Well, no, there’s a few drills from Asarco from way back, and it wasn’t really the key focus for us. Now, I let Alan do his work. He had just come into the company, built up the story, modeled it, and this year, when it came time to go drilling, we said, okay, Alan, you do what you think is necessary to turn this into a discovery.

And so, he started a program that’s been very effective, it was 14 or 15 holes. We have a lot of holes in the lab for assay.

Assays are slow at the moment, which is annoying, but I’m not too bothered by that, because right now, we can see we have a very large hypogene chalcocite orebody. Now, what does this mean? Well, hypogene means the fluids came up from below. Basically, the fluids were derived from a magma or something driving the system from below.

In this particular case, chalcocite, which is usually considered a supergene mineral, in other words, a product of weathering, like descending groundwaters, this is driven by something below. I think that’s very exciting, because it basically says there is some sort of mysterious porphyry that we have yet to likely identify down there, that is kicking off an absolute ton of copper, and it’s kicking it all the way up into the shallow environment. So, these assays from these subsequent holes are going to be very important.

I think they’ll show that we have a sizable chalcocite deposit in a shallow environment. That’s encouraging, but it also tells me that there’s something more going on here. Look at the world of porphyry copper deposits that have associated carbonate replacement deposits, you can look at the carbonate replacement deposit and go, okay, you know, it’s X millions of tons.

Therefore, the porphyry that’s associated with it should be, X size, you can kind of correlate the two. Well, here we have a district where you have this gigantic CRD system, a carbonate replacement deposit system, called Taylor, that is disproportionate to the porphyry in the district. Like, the porphyry can’t explain it.

I think this discovery is actually telling us we might be on to finding the mothership here. This is going to be an exciting story. It’s going to take a little while to unfold, but it’s going to deliver a lot of nice, juicy assays in the meantime.

I think we’re going to see this evolve into one of the great porphyry copper districts of Arizona. It’s a killer story.

RM: It’s cheap.

QH: And it’s cheap right now.

RM: It’s in a great area as well. I mean, that area is one of the best areas to explore and work in the US.

QH: That’s right, it is. I like it from that perspective.

It will take some time and patience to work out in Arizona, but I think this is a good jurisdiction. I think we’re in the right place.

RM: Do you think copper’s price is now permanent? The increase that we’ve had, do you think it’s justified by what’s going on in the world for demand and structural supply?

QH: I’m not an expert in copper prices, but what I’ve noticed is over my career that, regardless of the commodity, as metal prices increase, they do so in kind of a stair-step fashion.

There’s a lot of volatility here and there along the way, but when you see them break out of their local resistance, the resistance that we’ve seen in copper is around $4 and change, and then break upwards from there, usually it’s finding a new home. It’s probably not going to go back down into the sub-$4 range. I can’t promise anything, but in other words, $4 is the new floor and where do we land from here? I don’t know.

It might be a lot higher than this. Like you said at the beginning, the thesis behind copper is very compelling.

RM: You have to have the incentive pricing in the market for the majors to go build these mega-cost mines, mega-sized mines, and if you don’t have it, they’re not going to build it.

And if they’re not coming in to build these mega-mines, the deficit is just going to keep getting worse, something has to give here, and I think we’re seeing the beginning of it in the copper market now.

I want to talk to you about Electric Metals (TSXV:EML). This one’s off the beaten track. It’s high-grade manganese, and they’re going to build a processing plant to turn it into very valuable, value-added manganese products, not for steel, which is its biggest use, but for batteries. I like Brian Savage’s plan here to put all this together and build this.

It’s going to be an enormous effort, and it’s going to take some time, but I think the end result is going to be something that’s just like, whoa, what did he build, right?

QH: Exactly. Again, I’ve got to disclose, I’m a director of the company. I’ve known Brian for quite a while.

He went to the Colorado School of Mines like me. Brian is a very sharp businessman, and he’s also very sharp in the manganese space. There’s only a handful of people on the planet who are experts in manganese, and Brian happens to be one.

He’s an expert on the technical side. He’s also an expert on the business side. He knows what the markets are, what’s in most demand, what’s the highest value that you can achieve for a product in the manganese space, things like this.

And Brian has a very clear vision to basically not only develop our mine in Minnesota, but to build a company that becomes the go-to, the lead manganese provider in the battery space in North America. Give Brian about another six months, maybe a year, and I think he’s going to build something extraordinary. And he’s doing it at a time when manganese is still kind of a depressed commodity, which is interesting.

I love nothing more than building something when something’s cheap and then watching it increase in value. That’s what we did with San Cristobal. We picked it up when it was cheap, and now it’s worth extraordinary value.

Same thing here. I think whatever Brian builds today is going to have extraordinary intrinsic value once the manganese market and the demand picks up again. We see manganese as a very important part of the future in this electrification, the strategic metal side of things.

Eric Sprott is an investor. It’s very curious, because I remember talking to Eric the first time about manganese maybe a year ago, and he actually came in as an investor. I was absolutely surprised to hear Eric even consider manganese. But he’s like, have you seen the manganese prices? It’s just low as can be.

This is the time to come into manganese. And quite frankly, he’s right. That’s a very good approach.

And it’s going to pay off well. So we’re going to be hopefully the best investment that he has in manganese.

RM: Well, it’s a critical metal. We’re 100% reliant on the advanced products from China. And it might not be obvious in the US, but the world is turning to batteries. There’s absolutely no doubt the electrification and decarbonization that Obama started in 2009 has taken the macro trend here.

It’s batteries. Manganese gives your battery better range, it’s cheaper. Lithium was the first mover. I think adding manganese to these batteries is your second technology that’s going to happen. It’s fun to get in on the bottom of building something like this. To me, that’s the bottom line. It’s just going to be a great adventure.

QH: Exactly.

RM: As always, thank you for your time, Quinton.

QH: Thanks Rick.

Richard (Rick) Mills

aheadoftheherd.com

Subscribe to AOTH’s free newsletter

Richard owns shares of Torr Metals (TSXV:TMET), Cosa Resources (TSXV:COSA).

Quinton owns shares of Cosa Resources (TSXV:COSA), Electric Metals (TSXV:EML), Barksdale (TSXV:BRO), BCM Resources (TSXV:B), Mogotes Metals (TSXV:MOG).

TMET, COSA and EML are paid advertisers on his site aheadoftheherd.com. This article is issued on behalf of TMET, COSA and EML.

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.