Oil and gas vulnerability swaying countries to renewables – Richard Mills

2026.04.29

Despite Trump’s promise of a quick exit, the war in Iran has stretched into two months, with the Strait of Hormuz closure creating the worst oil supply shock since the 1973 OPEC embargo.

Many countries, especially those in Asia dependent on Middle Eastern imports, are struggling to get their hands on enough barrels and gigajoules to run their economies.

The Globe and Mail reports Pakistan and the Philippines have moved to a four-day work week for public officials, Bangladesh has closed universities, and various countries have mandated remote work for public servants and limited air conditioning in public buildings as a result of the energy shortage. Airlines across Asia are trimming flight schedules because they don’t have jet fuel.

Many countries now realize just how exposed they are to an energy shock, said Andrew Botterill, the global financial advisory leader for energy, resources and industrials at Deloitte.

Ed Crooks, vice-chair of Americas at commodities consultancy Wood Mackenzie, states “There will be a fundamental reassessment of energy security following this, just as there was after Russia’s invasion of Ukraine in 2022.”

The reassessment is likely to involve an acceleration of the global movement towards electrification and decarbonization. Renewables have their critics, but there is no disputing the fact that having them in a country’s mix of energy sources reduces reliance on oil and gas.

Forecasted demand for oil is expected to drop for the first time since the pandemic owing to what the International Energy Agency calls “the most severe oil supply shock in history.”

Blogger Chris Martenson says, “The worst energy shock on record is far worse than you think.” He adds the energy shock is set to get worse “even if the Iran conflict magically stops this minute.”

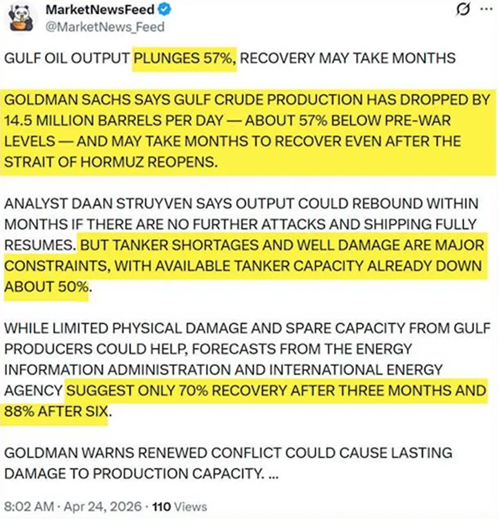

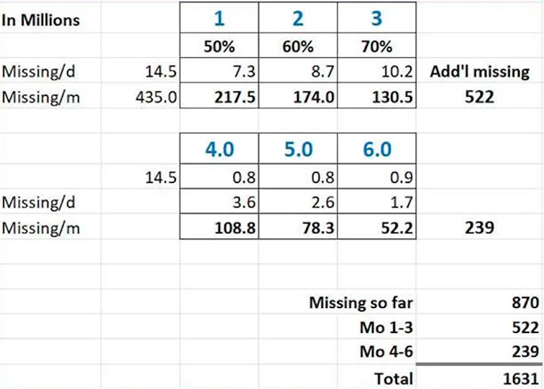

Quoting from a Goldman Sachs analysis detailed in the tweet below, Martenson notes 14.5 million barrels per day of oil+ products are missing. This works out of 435 million barrels a month, and 870 million barrels in the first two months of the war.

If the Strait of Hormuz were opened on Monday morning, April 24th, Goldman says the flow of Gulf oil would only be 70% restored after three months. That’s another 522 million barrels missing from the Gulf. The analysis says by month six, 88% of oil flows would be restored. That’s an additional 240 million missing barrels.

Add it all up, and the world will be missing 1.6 billion barrels (or 1600 million barrels). And that’s if and only if the Strait reopens on Monday. Each additional month of closure adds another 435 missing barrels to the total.

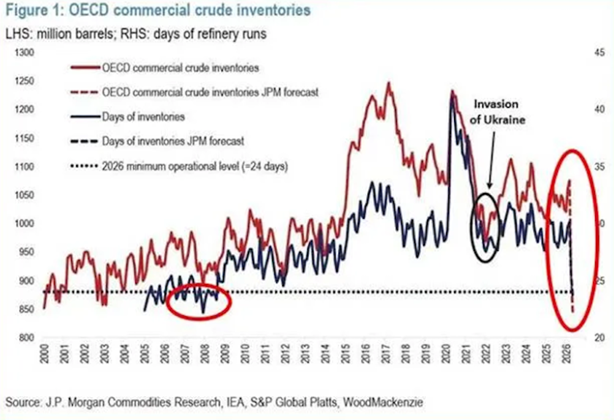

Meanwhile OECD commercial inventories are plummeting, as the chart below shows.

To counter these declines in commercial inventories, oil must be released from strategic reserves. The US, Japan, and OECD Europe have a combined 855 million barrels in reserve. The US wants to lower the price of oil, so it’s been selling its crude at subsidized prices. Total US crude oil and petroleum exports rose to a record 12.9 million barrels the week before last.

As Martenson writes, those extra exports from the US are not coming from additional oil production, but from stockpiles and inventories. In other words, the US energy reserves and buffers are being exported at subsidized prices to maintain the illusion that things are not as bad as they actually are.

That ends very badly, and suddenly someday. I give it 2-4 weeks, tops.

The bottom line is that the situation is already well beyond ‘dire’ and it is now only a matter of time before it all spools apart. Iran merely has to wait — the clock is on its side. The US desperately needs the situation to end, immediately, and desperate people do desperate things. [Like restarting hostilities — Rick]

On April 23, Faith Birol, secretary general of the IEA, told CNBC that the war in the Middle East and the closure of the Strait of Hormuz have created the largest energy security threat the world has ever faced.

“As of today, we’ve lost 13 million barrels per day of oil … and there are major disruptions in vital commodities,” Birol said.

Four days later, he repeated his concerns to The Guardian, stating

“There will be a significant boost to renewables and nuclear power and a further shift towards a more electrified future.” He added this would result in oil demand loss that will be permanent. (Oilprice.com)

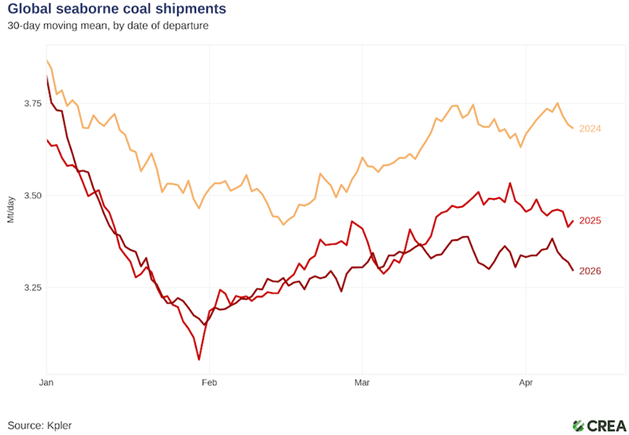

While many expected coal would benefit most from oil and gas price increases, in fact the greatest beneficiary has been renewables.

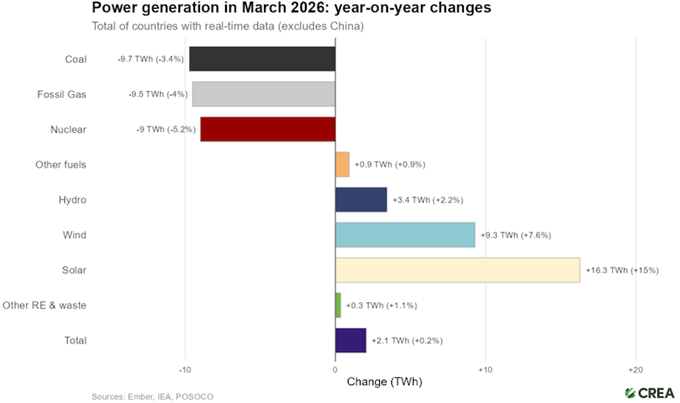

According to the Center for Research on Energy and Clean Air (CERA), power generation in March 2026 saw a 9.7 terawatt-hour (TWh) decrease in coal (-3.4%), followed closely be fossil gas, which dropped 9.5 TWh or 4%. Solar represented the largest increase by far, at a whopping +16.3 TWh or +15%. Wind was next at +9.3 TWh followed by hydro at +3.4 TWh.

CERA noted the fall in gas-fired power generation was offset by large increases in solar and wind power rather than coal. Seaborne coal transport volumes fell 3% to their lowest levels since 2021.

Also, the center observes that solar and wind power capacity added in 2025 alone generates twice as much electricity as all the LNG that was transported through the Strait of Hormuz before the closure.

The Globe quotes a recent paper by engineers at Stanford University, which found that switching the global energy system to electricity based on wind, hydro and solar would reduce the cost of energy.

Indeed, the cost of renewables has come down considerably. It is cheaper both in the efficiency of its production and in the lower cost of mining critical minerals than fossil fuels.

2024-25 data indicates that 90% of new renewable energy projects produce electricity at a lower cost than coal or gas alternatives.

Solar and wind are generally 41% to 53% cheaper than the lowest-cost fossil fuel options. Since 2010, the cost of solar and wind energy has dropped by over 80%.

Battery storage costs have fallen 89-93% since 2010. In 2024, renewable capacity additions saved an estimated USD$57 billion in fuel costs compared to fossil fuels.

According to the International Renewable Energy Agency (IRENA), renewables accounted for about 49% of global capacity by the end of 2025. (Zacks Investment Research)

In Europe, renewables are protecting some countries from rising electricity prices due to the Middle East conflict. But European countries with the least flexibility and the greatest marginal dependence on imported fuels are seeing the most impact in volatility and peak pricing, according to an analyst at energy research firm Rystad, via Reuters.

“Albania’s heavy reliance on renewable energy, particularly hydropower, has played a crucial role in cushioning the country from the worst effects of the crisis,” Albania’s energy ministry said in a statement.

France, which relies on nuclear for 70% of its electricity production, has seen its benchmark wholesale contract rise by less than half of Italy’s, which generates more than 40% of its electricity from natural gas and saw its benchmark increase over 20% since the war began. Spain’s prices dropped as renewables reached nearly 60% of total generation.

Natural gas-dependent Germany and Greece, which have some level of solar power production, are trying to build a long-term stack of renewables and long-term storage to offset gas.

Meanwhile, around 60 countries are meeting in Santa Marta, Colombia, this week to discuss how to phase out fossil fuels. The focus is on practical steps, not new targets.

The meeting includes Brazil, Germany, Canada and Nigeria. Top polluters China and the United States are absent, along with Saudi Arabia and other major Middle Eastern oil and gas producers.

“This war in the Middle East has ramifications all around the world because of our dependency on fossil fuels,” said Stientje van Veldhoven, climate minister for the Netherlands, which is co-organizing the meeting with Colombia. “The less you are dependent on it, the less vulnerable you are.”

Moneyweb notes around 80% of the oil trapped in the Persian Gulf is destined for the Asia Pacific region, prompting a switch to renewables due to skyrocketing electricity prices. For example, in Fiji, fuel import bills could rise to AUD$993 million, nearly triple the healthcare budget.

But while many compare the current energy crisis to the one in the early 1970s, the difference is that renewables have been deployed on a much larger scale. As mentioned they are also cheaper:

Since the 1970s, the price of solar panels has fallen 99.9%, while the cost of wind has fallen 91% since 1984. Battery prices have fallen 99% since 1991.

This means it’s now viable for many nations to switch to these alternatives.

France has doubled state aid to help households switch to EVs and electrify home heating, South Korea plans to double renewables capacity within four years, and new EV sales are hitting an all-time high in Australia after gasoline and diesel prices surged in March.

Batteries

The move away from fossil-fuel-powered vehicles to electric vehicles run on batteries is happening in almost every country. Governments are spending billions on EV charging infrastructure and subsidies to incentivize consumers to switch to hybrids and plug-in electric cars, vans and trucks.

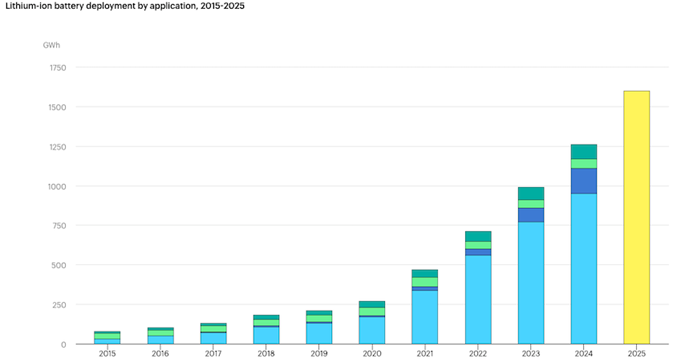

The global lithium-ion battery market exceeded $150 billion in 2025, an increase of over 20% from 2024. Demand is projected to grow over 30% annually through 2030. According to the IEA,

Batteries are becoming a cornerstone of the automotive sector, a critical source of flexibility for power systems, and an increasingly important source of back-up power for digital infrastructure, including data centres and artificial intelligence.

Beyond energy, batteries remain indispensable for a wide range of industrial and strategic applications, from portable electronics and unmanned defence systems to emerging technologies such as humanoid robots. As applications diversify and costs continue to fall, batteries are evolving into a foundational component of modern economies.

The IEA report says electric vehicles remain the dominant demand driver for batteries, accounting for more than 70% of total lithium-ion battery deployment, followed by energy storage at over 15%.

Lithium and graphite are essential for the lithium-ion batteries that go into EVs, storage systems, and other uses such as consumer electronics.

These batteries consist of an anode, cathode, separator, electrolyte and two current collectors (positive and negative). The cathode contains lithium, either in the form of lithium carbonate or lithium hydroxide, while the anode is made up of graphite.

One of the most successful lithium-ion battery systems is a cathode combination of nickel, manganese and cobalt (NMC).

NMC batteries are used in power tools and in power trains for vehicles because they offer higher energy density and therefore greater range. NMC batteries are also preferred for electric vehicles due to their better charging performance at low temperatures. This makes them more reliable and efficient in cold environments.

NMC chemistries have advanced well beyond the original one-third nickel, one-third manganese, one-third cobalt formulation, with today’s batteries adopting higher nickel ratios such as 5:3:2 and 6:2:2, alongside a growing shift toward manganese-rich chemistries to reduce cost, limit cobalt exposure, and enhance supply chain resilience.

The cathode combination ratio of a NMC battery is usually one-third nickel, one-third manganese and one-third cobalt, meaning that the raw material cost is lower than for other options.

By 2030, battery demand for manganese is set to triple as two key technologies scale:

- NMC batteries that use nickel, manganese and cobalt

- New sodium-ion batteries that also rely on manganese

According to the United States Geological Survey (USGS), the US is 100% dependent on imported supplies of manganese, since neither it nor Canada produces the critical mineral.

Manganese has gone from being perceived as a commonplace alloy metal primarily used in steel production to being a key metal in electric vehicles and energy storage due to its prominent role in lithium-ion battery formulations.

America therefore needs immediate action to build a secure mine-to-metal supply chain for manganese.

Electric Metals (USA) Limited (TSXV:EML, OTCQB:EMUS) has the highest-grade manganese deposit in North America and is poised to emerge as a low-cost producer of 100% domestically sourced, high-purity, battery grade, manganese products (HPMSM) for the electric vehicle battery and energy storage sectors.

The North Star Manganese Project is owned and operated by EML subsidiary North Star Manganese, and consists of exclusive exploration, mining and processing rights of manganese ores in the Cuyuna Iron Range, Crow Wing County, Minnesota.

Several historical drill holes have intersected grades above 50% manganese. Independent modeling of over 70 historical drill holes suggests a much larger deposit.

The project has been the subject of extensive technical evaluation, including a Preliminary Economic Assessment (PEA). Over $28 million has been invested to date.

It includes the construction of a 100,000 tonnes per year high-purity manganese sulfate monohydrate (HPMSM) plant at a yet-to-be determined location in the United States — a US first.

Electric Metals — Developing North America’s highest-grade manganese deposit — Richard Mills

The global lithium-ion battery anode market is projected to grow from roughly USD$19 billion in 2025 to over $81 billion by 2030, driven by a 33.6% CAGR as demand for high-performance material increases.

China has imposed restrictions on graphite exports. Exporters must apply for permits to ship synthetic and natural flake graphite.

Automakers and defense companies have been raising alarm bells over the fact that the United States hasn’t mined any graphite since the 1950s, and even if it had, it would need to be shipped to China for processing.

The electrification of the global transportation system doesn’t happen without graphite — the battery anode material with no substitutes.

Graphite is the largest component in batteries by weight, constituting 45% or more of the cell. Nearly four times more graphite feedstock is consumed in each battery cell than lithium and nine times more cobalt.

Aluminum and natural graphite are the two most used materials in the defence industry and can be found in aircraft (fighter, transport, maritime patrol, and unmanned), helicopters (combat and multi-role), aircraft and helicopter carriers, amphibious assault ships, corvettes, offshore patrol vessels, frigates, submarines, tanks, infantry fighter vehicles, artillery and missiles.

The US has no security of supply for graphite. It has clearly reached a point where much more graphite needs to be discovered and mined in the United States.

Fortunately, a large graphite mine is under development, along with a planned graphite anode manufacturing plant for all lithium batteries across all applications in Ohio.

Graphite One (TSXV:GPH, OTCQX:GPHOF) plans to build a graphite anode manufacturing plant in Trumbull County, Ohio that could supply 100% of the graphite demanded by the United States.

Consider: In 2025, the US imported 79,000 tons of natural graphite, of which 73.4% was flake and high purity.

Graphite One’s Graphite Creek Mine in Alaska would have capacity to produce 175,000 tonnes of graphite concentrate per year during its projected 20-year mine life.

Last June, the project, including the open-pit graphite mine and mineral processing plant, was accepted as a FAST-41 “covered project” to be listed on the FAST-41 Federal Permitting Dashboard.

FAST-41 streamlines the permitting process by providing improved timeliness and predictability by establishing publicly posted timelines and procedures for federal agencies, reducing unpredictability in the permitting process.

The Coordinated Project Plan established a 13.5-month schedule for the required federal environmental reviews and authorizations, with a projected completion date of September 29, 2026.

As of the latest dashboard update, the project remains “in progress” under the leadership of the U.S. Army Corps of Engineers.

Graphite One raising CAD$35M for Active Anode Materials plant — Richard Mills

US achieves security of graphite supply with G1 Feasibility Study – Richard Mills

Nuclear/ uranium

According to an AI Overview, global uranium demand is entering a strong growth phase, projected to rise 28% by 2030 and nearly double by 2040, driven by the expansion of nuclear energy for decarbonization and energy security. Demand is expected to rise from 67,000 tonnes in 2024 to over 150,000 tonnes annually by 2040, creating a significant supply-demand gap as aging reactors are extended and new units are constructed.

Global nuclear capacity is projected to increase by 13% by 2030 and nearly 87% by 2040, with massive growth in China and India.

Nuclear power is increasingly considered crucial for meeting carbon-free targets, with high demand from data centers and technology companies seeking reliable, clean power.

The market faces a severe supply-demand gap. By 2040, the cumulative uranium supply deficit is projected to reach 680,000 tonnes.

Growing supply risks and tightening markets have led to prices in 2025 reaching 14-year highs of USD$86.50 per pound.

The US is the top nuclear producer but relies heavily on imports, with 98% of its supply coming from foreign sources in 2026, notes the US Energy Information Administration.

Canada provides roughly 33% of US uranium, with 90% of Canadian production available for export.

According to the World Nuclear Association, just three countries — Kazakhstan, Canada and Namibia — control nearly 75% of global uranium production. “Such a high concentration of countries,” states Firstpost, “means these countries may have a veto over who can develop nuclear energy programmes — or nuclear weapons.”

The International Atomic Energy Agency indicates that sufficient uranium resources exist to support growth, but significant new investment in mining, exploration and processing is necessary to meet projected 2050 demand.

Enter Cosa Resources (TSXV:COSA, OTCQB:COSAF), a Canadian uranium exploration company operating in Saskatchewan’s Athabasca Basin, famous for its high grade at over 20 times global averages.

In January 2025, the company entered a strategic collaboration with Denison Mines (TSX:DML) that has secured Cosa access to several highly prospective eastern Athabasca uranium exploration projects.

Murphy Lake North (MLN) is a 70/30 joint venture between Cosa and Denison and is located at the northern end of the Larocque Lake Trend.

On March 24, 2026, Cosa reported that its first hole of the winter drill program at the Murphy Lake North Joint Venture intersected 5.0 meters of anomalous radioactivity.

Hole MLN26-013 registered up to 13,900 Counts Per Second (CPS) in the upper basement approximately 260 meters vertically from surface.

Drilling is ongoing and will test the immediate area around the radioactivity. Chemical assays from MLN26-013 are pending.

Conclusion

Many oil market observers have dismissed renewables for being unreliable baseload power due to the intermittency factor. Electricity can only be generated when the wind blows and the sun shines. Hydroelectricity is only possible when there is enough water to fill reservoirs to a level conducive to the operation of dams.

The war in Iran has shown the opposite, that oil and gas coming from the Middle East is unreliable due to Iran’s immediate closure of the Strait of Hormuz, creating the worst energy crisis in history. If Hormuz could be so easily blocked to shipping, so could other vital choke points like the Suez and Panama canals, or the Strait of Malacca.

Renewables may not be a substitute for rock-solid energy sources like coal, natural gas and nuclear, but they are becoming recognized as a good backup. In light of skyrocketing electricity prices due to fallout from the war, Europe and Asia are embracing renewables as a fail-safe option.

Countries like Albania, France and Spain, that have invested in renewables or nuclear, are finding themselves cushioned from the worst effects of the Middle East energy crisis. South Korea, ranked fourth or fifth among the world’s top oil importers, plans to double renewables capacity within four years. As fuel prices go berserk, Australia is seeing record purchases of electric vehicles.

Around 60 countries are meeting in Colombia this week to discuss how to phase out fossil fuels.

Batteries are energy storage devices. The switch to renewables requires critical minerals like manganese and graphite to manufacture batteries, and uranium, the nuclear fuel, to give us the clean base load electricity to charge the batteries. Companies exploring for these minerals are seeing increased interest from investors, who are beginning to realize that the shift from fossil fuels to renewables/ nuclear could be a permanent trend.

Richard (Rick) Mills

aheadoftheherd.com

Subscribe to AOTH’s free newsletter

Richard owns shares of Cosa Resource (TSXV:COSA) and Graphite One (TSXV:GPH). Richard does not own shares of Electric Metals (TSXV:EML).

COSA, GPH and EML are paid advertisers on his site aheadoftheherd.com

This article is issued on behalf of COSA, GPH and EML

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.

{kind=link}

{kind=link}

{kind=link}