Kodiak Copper aiming to bridge the valuation gap with its peers – Richard Mills

2026.06.07

Kodiak Copper (TSXV:KDK, OTCQB:KDKCF, Frankfurt:5DD1) had a phenomenal 2025, releasing a maiden resource estimate on its MPD Project in south-central British Columbia, and the share price tripling from $0.35 in early January 2025 to $1.05 at the end of the year.

We predicted the initial mineral resource estimate (MRE) would be a catalyst for share price appreciation, and we were right. The MRE came in two phases — phase one was released last June, on four of the seven mineralized zones, with the remaining three zones, and the full, yet far from finished in my opinion MRE, released in December 2025.

Kodiak Copper publishes sizeable maiden resource estimate with lots of room to grow — Richard Mills

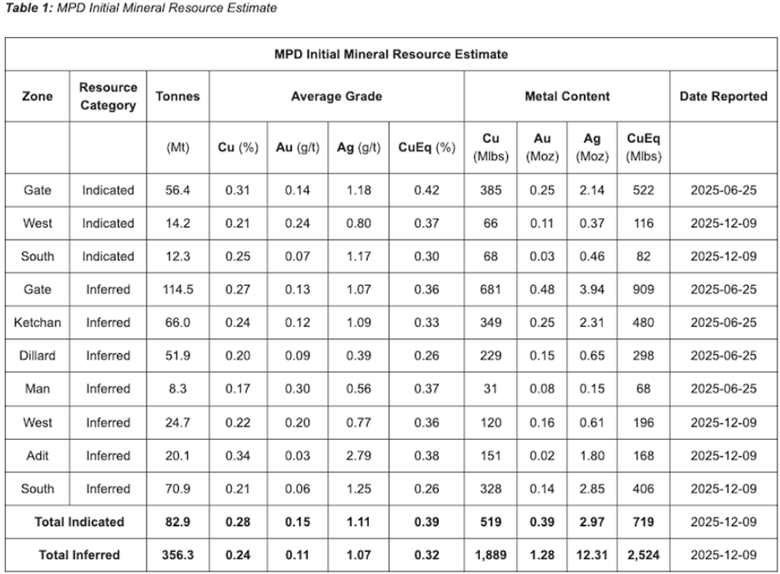

The Indicated is 82.9 million tonnes grading 0.39% copper equivalent (CuEq) for 519 million pounds of copper and 390,000 ounces of gold.

The Inferred is 356.3 million tonnes grading 0.32% CuEq for 1.889 billion pounds of copper and 1.28 million ounces of gold.

Between the Indicated and Inferred categories, the resource amounts to 2.408 billion pounds of copper and 1.67 million ounces of gold.

Or in copper-equivalent terms, 0.719 million pounds of Indicated CuEq and 2.524 million pounds Inferred.

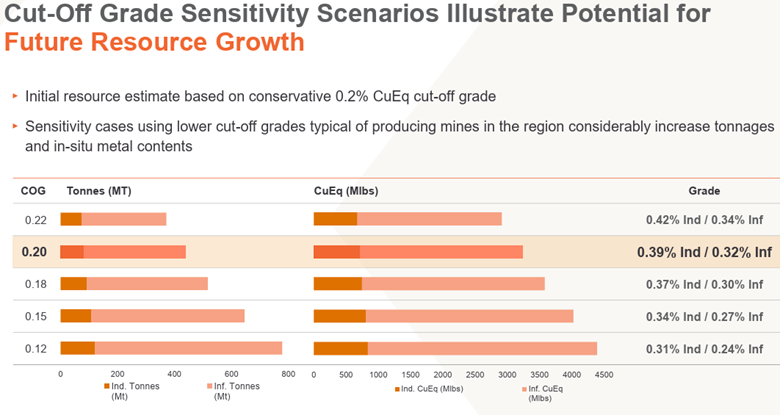

The MRE is defined using a cutoff grade of 0.2% CuEq.

Junior resource company stock prices move on the successful completion of the various stages necessary to develop a discovery into a mine. An initial mineral resource estimation is one of the key steps and Kodiak Copper obviously pleased the market with theirs.

The market liked what it saw, and re-rated KDK with the stock climbing from 35 cents at the beginning of the year to over a dollar a share upon the MRE’s release in December.

Share structure

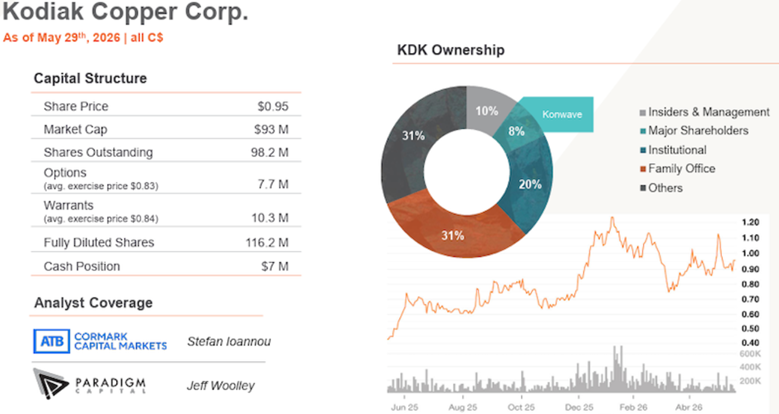

The number of outstanding shares is an important metric for junior resource investors to study. Stock dilution is the decrease in a shareholder’s ownership percentage when the company issues new shares. It reduces each investor’s proportional stake.

In Kodiak Copper’s case, it only has 98.2 million shares outstanding, and a strong cash position of $7 million — money it can use for 2026 exploration and increasing the existing resource. More on that below.

On June 2, 2026, Kodiak announced an upsized financing of up to approximately CAD$13.1 million. A larger treasury lengthens Kodiak’s runway of what it can accomplish during this year’s exploration season.

Peer comparisons

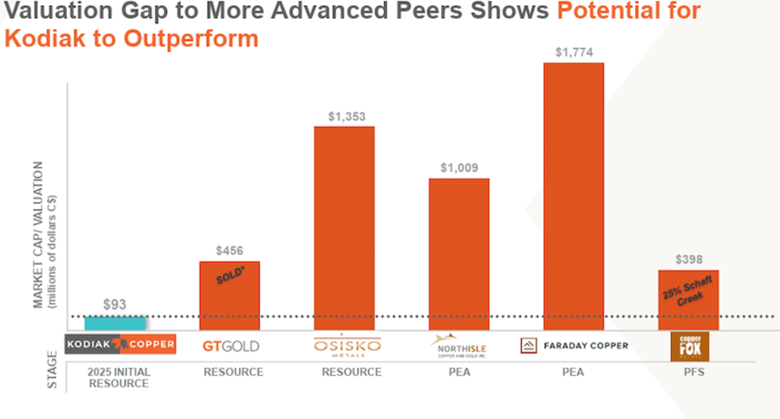

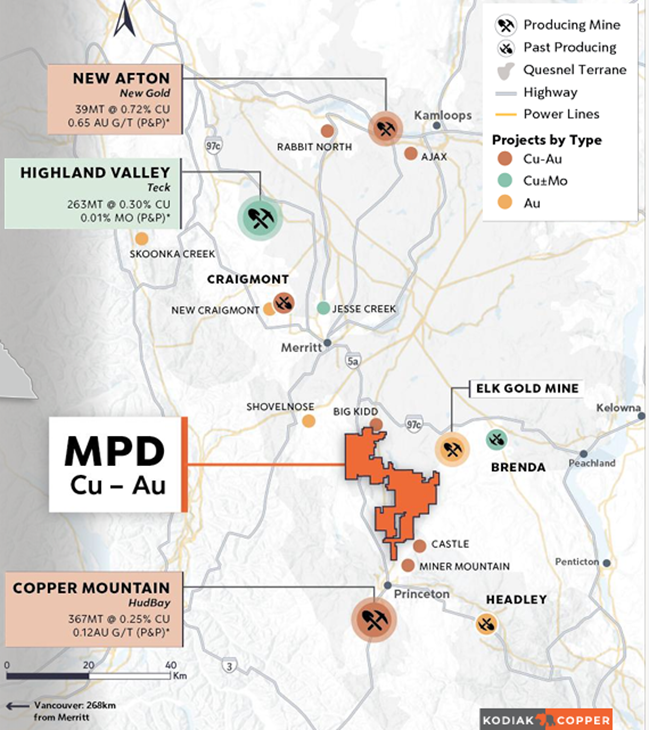

Along with completion milestones, junior resource companies are also rated based on peer comparisons. There are five copper companies KDK uses for this purpose. Kodiak isn’t hiding this information, in fact it forms an important part of the corporate presentation.

All five are farther along the development path because they started earlier — two to five years. Kodiak Copper sees them as aspirational — they represent the direction in which Kodiak wants to go. The way to get to where their peers are today is to increase the resource and eventually publish a Preliminary Economic Assessment (PEA), another major milestone on the development path.

The first slide shows Kodiak’s May 29 market capitalization of $93 million is below GT Gold’s (acquired by Newmont Mining (NYSE:NEM)) $456 million, Osisko Metals’ (TSX:OM) $1.353 billion, NorthIsle Copper and Gold’s (TSXV:NCX) $1.009 billion, Faraday Copper’s (TSX:FDY) 1.774 billion, and Copper Fox Metals’ (TSXV:CUU) 25% share of the Schaft Creek Joint Venture with Teck Resources (TSX.B:TECK), worth $393 million. (all numbers in CAD$)

The answer why is obvious. Kodiak “only” has an initial (combined Indicated and Inferred) resource of 2.408 billion pounds of copper and 1.67 million ounces of gold. (0.7 Blbs Indicated and 2.5Blbs Inferred, in copper-equivalent)

Newmont and Osisko both have larger resources. Newmont’s Saddle North Project MRE comprises a copper-equivalent resource of 3.1 billion pounds Indicated and 4.9 Blbs Inferred.

The updated MRE for Osisko Metals’ Gaspe Copper Project in Quebec show an Indicated 12.8 Blbs CuEq and 2.4 Blbs Inferred.

NorthIsle Copper and Gold has a PEA on its North Island Project on Vancouver Island, British Columbia. Its CuEq resource is an Indicated 6.3 Blbs Indicated and 1.2 Blbs Inferred.

Faraday Copper also has a PEA. Its Copper Creek Project, Arizona, combined open pit and underground, contains 4.6 CuEq Blbs in the Measured and Indicated category, and 0.7 Blbs Inferred.

Finally, the Schaft Creek Joint Venture which is 75% owned by Teck Resources and 25% by Copper Fox. Copper Fox’s interest in the project works out to a Measured and Indicated reserve of 2.9 Blbs and 0.5 Blbs of Inferred, copper equivalent. At the prefeasibility (PFS) stage, this project is the furthest advanced.

To get a clearer picture of these comparisons we need to look at the cutoff grades. A cutoff grade is the minimum concentration of a mineral required to classify extracted material as valuable ore rather than worthless waste.

Kodiak’s maiden resource estimate has a cutoff of grade of 0.2% CuEq.

A higher cutoff grade lessens the amount of ore a miner can glean from the gangue, or rock that surrounds the ore, but implies a more conservative evaluation of the amount of ore than can be extracted.

In Kodiak’s case, the 0.2% is seen as high enough to survive the lows of mining’s economic cycles.

Its peer comparisons have lower cutoff grades, meaning they can include more ore (pounds and ounces) in their resource calculations.

For example, Newmont’s MRE on Saddle North has an NSR (Net Smelter Returns) cutoff grade of 0.13% CuEq; the North Island Project’s MRE base-case cutoff is $11.50 NSR per tonne of resource estimation, North Island uses between 0.1% and 0.18% for their deposits; the Copper Creek Project’s MRE for the pit shell-constrained resources are 0.13% CuEq for oxide material and 0.14% CuEq for sulfide material; Osisko’s MRE for its Gaspe Copper Project has a cutoff grade of 0.13% Cu; and the Schaft Creek Joint Venture uses an NSR cutoff of $5.50/tonne for its MRE, which equates to a CuEq cutoff grade of 0.11% to 0.15%.

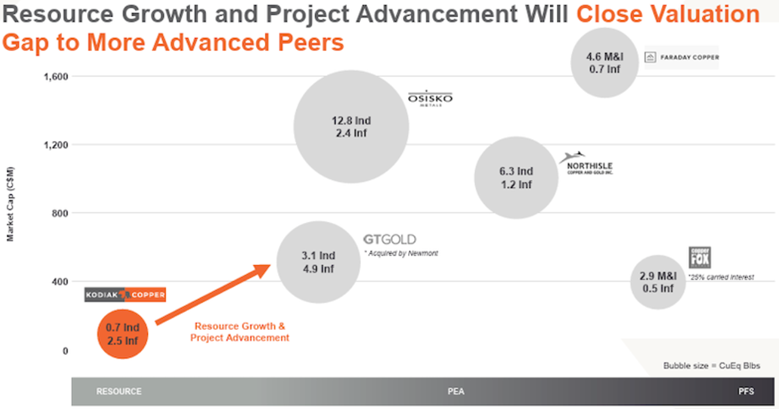

Closing the valuation gap

The question is how does KDK catch up to its peers, with their higher market capitalization (MC) based on higher resource estimates in the case of GT Gold/ Newmont and Osisko Mining, PEAs in the case of NorthIsle Copper and Gold and Faraday Copper, and a PFS in the case of the Schaft Creek Joint Venture between Copper Fox and Teck?

The answer is quite simply to do more exploration and more drilling. Kodiak believes that resource growth and project advancement will close the valuation gap to its more advanced peers and we, at AOTH, believe that will result in a significant stock re-rating.

2026 exploration

The fully funded 2026 exploration program at MPD includes drilling aimed at expanding the maiden resource estimate, and field investigations to advance multiple exploration targets.

The program started at the end of April.

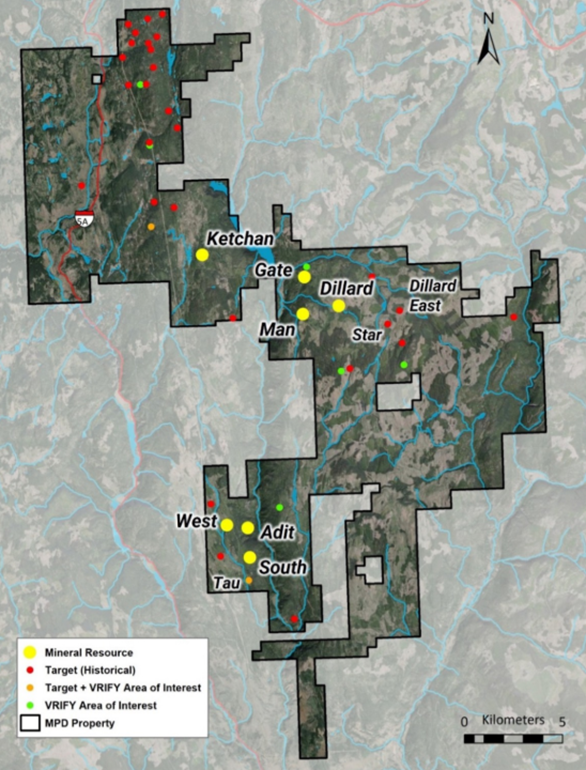

It will involve core drilling, 3D induced polarization (IP) and audio- magnetotelluric (AMT) geophysical surveying, geological mapping and prospecting. Core drilling will commence at the Ketchan deposit, which has not previously been drilled by Kodiak. The 2026 drill program is anticipated to total 6,500 meters, with scope for expansion as the program progresses.

Further exploration activities will focus on target evaluation and prioritization in support of drill planning, on both the known deposits and prospective exploration targets of interest.

Kodiak Copper has successfully highlighted a large, open-pit initial mineral resource estimate, which shows the scale and potential of MPD and lays the foundation for future resource growth and development.

The West, Adit and South deposits all feature shallow mineralization and favorable geometry, characteristics that are expected to support low strip ratios in future economic evaluations. West and Adit host higher-grade mineralization from surface, while South is a large bulk tonnage deposit over 1 km in length that is still underexplored.

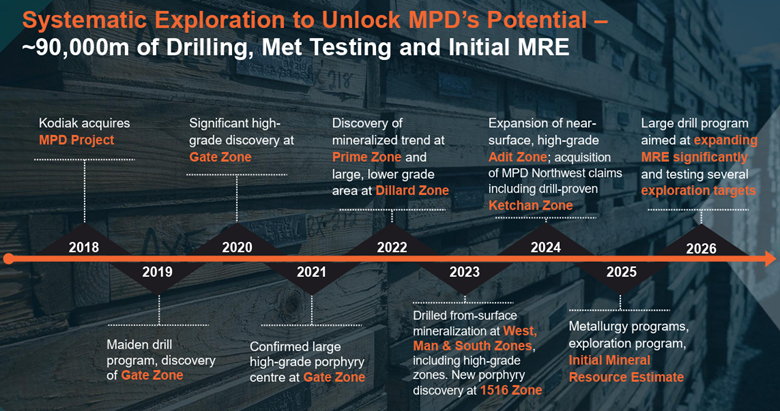

The resource on the MPD Project is based on decades of historical exploration and Kodiak’s drilling from 2019 to 2025 totaling approximately 90,000 meters.

In February, Kodiak reported soil geochemical and prospecting results from the 2025 exploration program, which confirmed numerous historical high-grade targets, identified new targets, and highlighted the potential to expand the MRE reported for the Ketchan deposit.

The best prospecting grab sample assayed 11.4 % Cu, 23.8 g/t Au and 43.6 g/t Ag. The sample was from historical workings at the Tomcat area in MPD Northwest.

While the company has identified multiple mineralization deposits, it remains committing to continued exploration to further grow the project, both through deposit expansion and the testing of new targets.

All deposits at MPD remain open for expansion within and beyond the MRE pit shells, most in multiple directions and at depth.

Kodiak has identified opportunities to expand all seven deposits in the MRE, including potential extensions beyond the current mineralized zones and gaps within the MRE models.

It is expected that most of the seven deposits will be drilled in 2026.

In 2025 Kodiak identified 16 new exploration targets, including historical showings on recently acquired claims, prospects from the 2025 regional exploration program, and Areas of Interest generated by VRIFY Artificial Intelligence (AI) assisted targeting.

This brings the total of prospective targets that have been identified for follow-up, to date, to 36. Kodiak plans to advance or drill several of these targets, including the Dillard East, Star and Tau targets.

“We are pleased to commence our 2026 exploration program at MPD, building on the success of last year’s maiden resource, President and CEO Claudia Tornquist said in the April 28 news release. “Our focus is to expand known deposits and advance a strong pipeline of high-quality targets that offer meaningful discovery potential. With a clear path to resource growth and new discoveries, we believe this program will be a key driver in unlocking further value at MPD.”

Conclusion

Kodiak Copper has an MRE in hand, money in the bank, and a tight share structure that implies minimal dilution has taken place despite multiple financings over the years.

Kodiak is over a month into a 6,500-meter drill program at MPD that has the potential to make a meaningful addition to the maiden resource of 2.408 billion pounds copper and 1.67 million ounces gold. I suspect that after the on-going financing is closed the size of the 2026 drill program will increase significantly.

It is expected that most of the seven deposits will be drilled in 2026.

All seven remain open for expansion within and beyond the MRE pit shells, most in multiple directions and at depth. The company has identified 36 prospective targets that have been pinpointed for follow-up.

Kodiak Copper is drilling and exploring MPD in a bull market for copper. Demand is exceeding supply and copper is hitting all-time highs.

Along with all the usual applications for copper — in construction, transportation and telecommunications — demand is being driven by ongoing electrification and decarbonization of the transportation system and the exponential growth in battery storage.

Furthermore, copper is vital to artificial intelligence and the infrastructure that supports AI. The associated increase in data centers is causing an explosion in electricity demand, requiring substantial copper for new infrastructure and power transmission.

This all boils down to everything driving the world’s economies needs more copper, in the face of persistent constraints on mine supply.

Why we’re running out of copper — Richard Mills

While the copper market was roughly balanced in 2025, meaning that refined production met consumption, mine supply was severely disrupted and will likely create a deficit in 2026, states the International Institute for Strategic Studies (IISS).

A significant long-term deficit is projected, potentially exceeding 6 million tonnes annually by the early 2030s. Total output from copper mines in 2025 was 23Mt, according to the US Geological Survey.

The completion of the maiden resource estimate was a major catalyst for share price appreciation in 2025. The next catalyst is closing the valuation gap with Kodiak Copper’s peers. Kodiak thinks that by doing more drilling and resource expansion it can catch up, and I agree.

We had the initial pop because of last year’s copper bull market, which is continuing, and the resource estimate. Now Kodiak is working to increase that resource through expansion drilling on the existing deposits and hopefully making more discoveries. The goal, other than expanding the resource, is to work towards a PEA — the next evaluation standard after an MRE.

This gets Kodiak towards its peers. You can see where Kodiak is potentially going by looking at its peers. They’re farther along the development path because they started sooner. But what Kodiak needs to do to catch up is to keep piling pounds and ounces onto that initial resource.

KDK is doing the same work its peers have been doing but are doing it in a better copper market.

Why invest in Kodiak? The thesis is quite simple. Because the company is following a step-by-step process of moving the project forward, where it gets re-evaluated each time it is successful.

Kodiak has taken the first step in making a discovery at MPD. The second step was compiling an initial resource. Now KDK needs to build that resource out. The next milestone is a PEA. Stay tuned for plenty of news flow between now and then.

Kodiak Copper

TSXV:KDK, OTCQB:KDKCF, Frankfurt:5DD1

Cdn$0.80, 2026.06.05

Shares Outstanding 98.1m

Market Cap Cdn$78.6m

KDK website

Richard (Rick) Mills

aheadoftheherd.com

Subscribe to AOTH’s free newsletter

Richard does not own shares of Kodiak Copper (TSXV:KDK). KDK is a paid advertiser on his site aheadoftheherd.com.

This article is issued on behalf of KDK

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.