Copper price riding $6 wave on supply concerns, sulfuric acid crisis – Richard Mills

2026.07.17

Copper futures climbed above $6.30 per pound Thursday, hitting over three-week highs as production in Chile declined due to a combination of water shortages, lower ore grades, unplanned maintenance, the transition from oxide to sulfide mining and labor disputes.

Chile’s monthly economic activity index has recorded consecutive declines this year, largely reflecting weaker mining activity and reduced copper output across several major operations. Chile accounts for roughly 50% of global copper exports, with the metal contributing more than 10% of the country’s GDP.

Copper prices also benefited from softer-than-expected US inflation data that eased concerns for imminent Federal Reserve interest rate hikes. Meanwhile, traders continued to monitor escalating tensions in the Middle East, with the resulting demand shock offsetting concerns over potential supply disruptions. (Trading Economics)

US copper futures are up 42% since Aug. 1, 2025.

Why is copper above $6 a pound and is the price sustainable? In this article we’re taking a deep dive into the copper market.

Structural deficit

The copper industry is entering a structural deficit, with demand from electrification and AI expected to outpace new mine development. Recycling is essential for filling this gap, but it is not currently capable of meeting the entire deficit on its own.

Why we’re running out of copper — Richard Mills

While the copper market was roughly balanced in 2025, meaning that refined production met consumption, mine supply was severely disrupted and will likely create a deficit in 2026, states the International Institute for Strategic Studies (IISS).

A significant long-term deficit is projected, potentially exceeding 6 million tonnes annually by the early 2030s. Total output from copper mines in 2025 was 23 million tonnes, according to the USGS.

A study released on Jan. 8 by S&P Global Market Intelligence and S&P Global Energy found that copper supply is expected to fall 10Mt short of demand by 2040, putting at risk industries such as artificial intelligence, defense spending and electrification.

The shortage would be 23.8% shy of the projected demand of 42Mt, even as copper recycling doubles to 10Mt. AOTH research has found that copper supply has not been able to meet demand without recycling for the past several years.

Demand drivers

The four sectors underpinning a stronger outlook for the copper market are: the rapid expansion of data centers; geopolitical tensions ratcheting up spending on defense and boosting infrastructure resilience; low-carbon energy projects consuming record amounts of copper; and Southeast Asia and India becoming major consumers of copper as they rapidly industrialize.

Data centers use between 20 to 50 tons of copper per megawatt of installed power capacity, with high-performance AI and hyperscale facilities requiring tens of thousands of tons per site. These massive quantities are primarily consumed by heavy power distribution units, cooling systems and thousands of server rack connections.

Chile’s output plummets

Mined output remains tight due to ongoing supply disruptions. The world’s second largest copper mine, Grasberg in Indonesia, is still underutilized due to a mudslide last September that triggered a force majeure. Meanwhile, production guidance at Chile’s Quebrada Blanca mine has been downgraded due to operational challenges.

Copper output in the Andean nation, which is the top copper producer, fell 12.9% year-on-year in May to 423,623 tonnes.

The Chilean government just cut its 2026 GDP growth forecast to 1.8% from a previous 2.1%, and raised its average copper price forecast to $5.90 per pound this year from $5.46 previously.

State-run copper miner Codelco expects flat production in the coming years. When asked if the company was on track to meet its 1.7Mt per year target by 2030, chairman Bernardo Fontaine reportedly said Codelco expects production to stay similar to current levels.

The miner is working to recover from a slump in 2022 and 2023 when production fell to two-decade lows. Last year’s production at Codelco’s own mines stood at 1.33 million tons…

He added that the company’s structural projects, designed to counter declining ore grades, had faced unexpected delays and costs.

US tariffs exacerbating shortage

The US tariff structure is causing structural tightness and price volatility in the copper market, pushing the metal near historic highs of nearly $14,000 per tonne. By heavily taxing semi-finished imported goods and threatening future duties on raw refined copper, the tariffs are forcing a massive stockpiling of metal in US warehouses and driving up costs for domestic manufacturers.

Since 2025, a 50% tariff has applied to semi-finished copper products, including pipe, wire, and rod, while refined copper cathode, the primary input for wire mills, smelters, and fabricators, remains exempt. A Presidential Proclamation directed the Department of Commerce to determine whether refined copper cathode should face a phased tariff of 15% from January 2027, rising to 30% in January 2028. The recommendation was due by June 30, 2026, but the deadline passed without a public determination, giving importers more time to move copper into the US ahead of any tariff announcement and reducing available supply in other markets. (Crux Investor)

Crux points out the connection between an expected tariff on refined copper cathode, and copper inventories:

An estimated 900,000 tonnes of copper have moved into US warehouses this year, as traders position themselves ahead of a potential tariffs, reducing available supply outside the US.

Goldman Sachs revised its 2026 copper outlook from a 490,000-tonne global surplus in April to a 640,000-tonne deficit outside the US by June, as tariff-driven stockpiling redirected metal into US warehouses.

The June forecast also projected a further 170,000-tonne deficit in 2027, alongside a 900,000-tonne increase in US inventories to roughly 1.8 million tonnes by year-end.

Sulfuric acid shortage

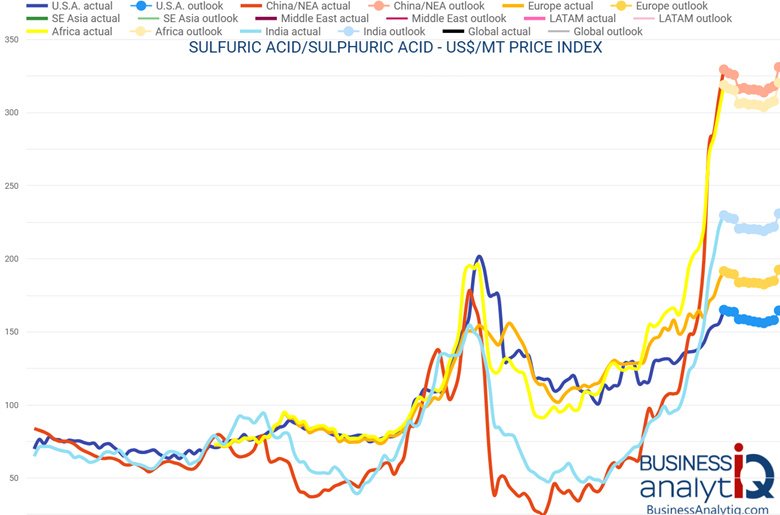

The closure of the Strait of Hormuz has caused a global sulfur crisis, as the Persian Gulf accounts for roughly half of the world’s seaborne sulfur trade. Prices have skyrocketed (up over 40% to $600+ per metric ton in some regions) because the blockade has halted essential byproduct exports from Gulf refineries.

Sulfur chokepoint threatens critical minerals supply — Richard Mills

Tit for tat attacks between the Houthis and Saudi Arabia have just taken place. If the Houthis close the Strait of Bab-el-Mandeb over a third of the world’s seaborne oil will be stuck in ports or at anchor in two straits.

The closure of the Bab el-Mandeb strait would severely exacerbate the sulfur crisis. Because 92% of the world’s sulfur is a byproduct of oil and gas refining, Middle East waterways are critical arteries for the chemical’s export. Blocking both Bab el-Mandeb and the Strait of Hormuz creates a disastrous dual-chokepoint that entirely cuts off global supply chains for fertilizers, battery metals and water treatment.

(Sulfur compounds like sulfuric acid and sulfur dioxide are essential for pH adjustment, disinfection, and chemical processing.)

Even after the Strait of Hormuz reopens, experts estimate the global sulfur crisis will take 6 to 12 months to fully normalize. The massive backlog, infrastructural damage and cascading policy changes mean the crisis will not resolve immediately upon the resumption of traffic.

Outdoor stockpiles of elemental sulfur can help alleviate regional supply crunches for fertilizers and industrial metals, but processing these reserves is complicated by strict logistical bottlenecks and environmental regulations.

Outdoor sulfur is contaminated and must be reprocessed. There is a huge shortage of covered railcars and processing facilities are limited.

Sulfur is essential in mineral processing primarily because it is the foundational building block for sulfuric acid. Often called the “King of Chemicals,” sulfuric acid is the most heavily consumed chemical in the world and is the workhorse used to dissolve, separate, and recover valuable critical minerals from raw ore.

Sulfuric acid is a core reagent in the heap leaching and solvent extraction-electrowinning (SX/EW) process used to produce copper from oxide ores and certain secondary sulfide ores. This hydrometallurgical method is essential for the economic recovery of low-grade deposits and is widely employed across major copper-producing regions worldwide.

The top countries utilizing sulfuric acid for hydrometallurgical processing (heap leaching and SX-EW) are Chile, the Democratic Republic of the Congo (DRC), Peru, Zambia and the United States.

Unsurprisingly, Chile is the top copper producer and the largest user of sulfuric acid for copper heap leaching, with a significant portion of its cathode production derived from solvent extraction and electrowinning (SX/EW), a two-stage hydrometallurgical process used to produce high-purity copper from oxide and low-grade ores.

Heap-leached cathodes account for roughly 40% of Chile’s total copper exports.

Heap-leach operations supply roughly one-fifth of the world’s refined copper, an amount approximating 4 million tonnes per year. According to the USGS, global refined copper production last year was 29 million tonnes, so heap leaching using sulfuric acid represents almost 14% of the total.

The global sulfuric acid shortage has driven copper prices to historic highs exceeding $14,000 per ton, while directly threatening up to 20% of global mine production. The squeeze stems from shipping disruptions in the Strait of Hormuz and China’s total halt on acid exports to protect domestic agriculture.

The crisis has caused severe, uneven impacts across the industry:

- Price Spikes: Spot prices for sulfuric acid in key import hubs like Chile have roughly doubled. Overall, acid prices have surged by as much as 156%.

- Leaching Operations at Risk: Roughly 20% of global copper output uses solvent extraction and electrowinning (SX-EW) to extract metal from oxide ores. These mines are facing production curtailments and spiking operating costs due to the acid deficit.

- Smelter Profits: Conversely, copper smelters are seeing increased margins because sulfuric acid is a profitable byproduct of the smelting process.

- Market Exposure: Import-reliant nations like Australia and Chile face much higher risks than countries with robust domestic sulfiur supplies like the US.

China’s export ban

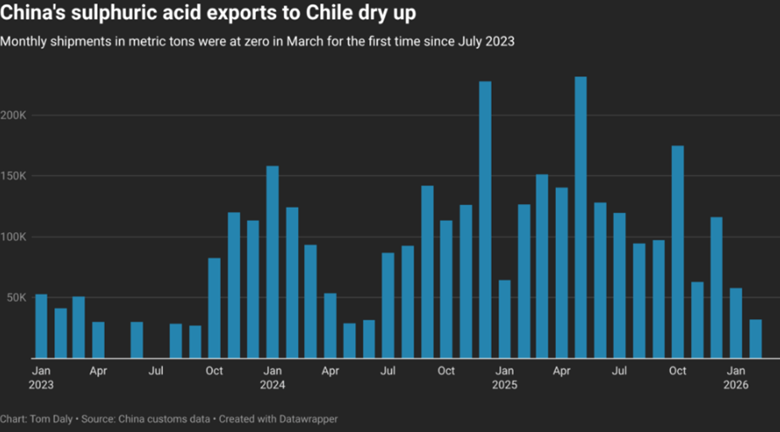

The closure of the Strait of Hormuz has been accompanied by China’s complete ban on sulfuric acid exports, worsening the crisis.

Reuters reported in April that China’s exports of sulfuric acid to Chile dwindled to zero in March.

Since Chile does not produce enough acid of its own, it depends on imports, 37% of which come from China, according to HSBC. It thus partly relies on Chinese smelters that purchase its ore to send back the acid for leaching so it can make more metal.

But relations between mining companies and China’s smelters have been strained recently as tight ore supplies have meant treatment charges – the fees paid to process ore – have been heavily in the miners’ favour.

“If sulphur supply tightens, acid availability becomes more constrained and expensive,” Alexis Urbani, a sulphuric acid trader with Incotrade Chile, told Reuters.

“That can directly impact cathode production, especially for operations relying on secondary sulphides or lower-grade ores, where acid consumption is higher.”…

Chile is particularly vulnerable to supply fluctuations, Bold Baatar – chief commercial officer at Rio Tinto, co-owner of the country’s giant Escondida mine – told a conference on Wednesday.

“The most exposed country is Chile in terms of need for sulphuric acid imports, because that’s where the highest amount of leached copper is,” he said.

On May 1 China halted exports of sulfuric acid to ensure its domestic fertilizer industry does not face a shortage.

China has been the world’s largest exporter of sulfuric acid. In 2025, Chinese exports surged 73% to 4.65 million tonnes. Much of that acid is a byproduct of copper smelting: about 40% of these exports stem from metal smelting. Over the past two decades, China built nearly half the world’s copper smelting capacity…

The closure of the Strait of Hormuz has blocked seaborne sulfur from the Persian Gulf. Russia has extended its own export ban through June 2026. Turkey has announced restrictions. The DRC has cut volumes. And China, facing a domestic deficit, has halted sulfuric acid exports entirely to protect fertilizer production. From record exports to a near-total ban in less than a year. Chile imports more than a million tonnes of Chinese sulfuric acid annually for the heap-leach operations that produce roughly a fifth of global copper. Spot prices for acid delivered to Chile have doubled since February. The same squeeze is hitting miners in the DRC and Zambia. (Mining.com Op-Ed)

Conclusion

Copper prices rallied to record highs at the start of the year, hitting $6.26 per pound in January. Although copper slumped in March on fears of slowing economic growth due to the Iran war, prices have picked up. From $5.27 on March 20, US copper futures have climbed 18% to reclaim January’s record-high $6.26.

At the top of the article, we asked: Is $6 copper sustainable?

The answer, in my view is yes. A combination of factors underpin a bullish narrative.

First is the supply-demand imbalance. Mine supply was severely disrupted in 2025 and will likely create a deficit in 2026. Operational issues continue, especially in number one producer Chile. State miner Codelco forecasts flat production over the next few years despite attempts to bring on new projects that address declining ore grades.

Second is the global sulfuric acid shortage, which has driven copper prices to historic highs exceeding $14,000 per ton, while directly threatening up to 20% of global mine production. Because so much of Chile’s operations are heap-leach, it is the country most vulnerable to sulfuric acid supply hiccups.

Spot prices for sulfuric acid in key import hubs like Chile have roughly doubled. Overall, acid prices have surged by as much as 156%. That’s with the Strait of Hormuz closed. If the Houthis block the Strait of Bab el-Mandeb, the crisis will worsen considerably.

Blocking both Bab el-Mandeb and the Strait of Hormuz creates a disastrous dual-chokepoint that entirely cuts off global supply chains for metals that are processed using sulfuric acid.

On top of this, China since May 1 has implemented a complete ban on sulfuric acid exports to protect its domestic fertilizer supply.

Chile imports more than a million tonnes of Chinese sulfuric acid annually for the heap-leach operations that produce roughly a fifth of global copper.

According to the International Energy Agency, copper mines producing more than a seventh of the world’s primary supply are now hostage to a sulfuric acid market thrown into chaos by the Middle East conflict and Beijing’s export ban. (Mining.com)

The bottom line is, without a resolution to the Iran war, or indeed with an escalation of it, the world’s top copper mining countries needing sulfuric acid for metals extraction will be forced to cut production, further widening the current gap between demand and supply.

Third is stockpiling ahead of a US tariff on refined copper cathodes in January 2027. An estimated 900,000 tonnes of copper have moved into US warehouses this year, as traders position themselves ahead of the potential tariff, reducing available supply outside the US.

Goldman Sachs revised its 2026 copper outlook from a 490,000-tonne global surplus in April to a 640,000-tonne deficit outside the US by June, as tariff-driven stockpiling redirected metal into US warehouses.

The June forecast also projected a further 170,000-tonne deficit in 2027, alongside a 900,000-tonne increase in US inventories to roughly 1.8 million tonnes by year-end.

The already tight copper market is getting tighter. Copper futures have risen 42% since Aug. 1, 2025, and are likely to remain above $6 for some time.

Richard (Rick) Mills

aheadoftheherd.com

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.