Uranium market fundamentals bullish

2026.07.10

The uranium market is experiencing a divergence between stable physical prices and a recent selloff in mining equities, driven by a structural long-term supply deficit and surging power demands from tech companies.

Market dynamics and key drivers

- Spot Prices: Uranium holds steady in the mid-$85 per pound range, following a cooldown from earlier speculative rallies.

- Big Tech Integration: Major data center operators (including Microsoft, Amazon and Google) are actively signing power purchase agreements and securing nuclear capacity to fuel future AI workloads.

- Supply Deficit: Fundamentals point to a prolonged global supply deficit as utilities increasingly lock in higher long-term contracts to ensure secure fuel supplies.

US government support

Uranium was designated as a critical mineral in November 2025, when the US Geological Survey (USGS) officially released the final 2025 List of Critical Minerals.

President Donald Trump supports the nuclear industry with aggressive executive actions, deregulation, and loans aimed at quadrupling domestic nuclear capacity. His administration views nuclear energy as a critical component for American energy sovereignty and a vital power source for surging Artificial Intelligence (AI) data centers.

Specific support initiatives include:

- The Reactor Pilot Program: Trump issued executive orders setting a deadline for American companies to build and switch on advanced, experimental commercial micro-reactors. Several companies, including Deployable Energy, Valar Atomics and Aalo Atomics met these operational milestones by going critical.

- Financial Backing: The Department of Energy has committed to massive loan programs, including $17.5 billion in loans to spur the construction of large-scale reactors. Additionally, an $80 billion agreement was signed with Westinghouse Electric Company to build large-scale plants.

- Regulatory Overhaul: The administration has rewritten Nuclear Regulatory Commission rules and proposed eliminating longtime radiation safety principles—such as the ALARA (As Low As Reasonably Achievable) standard — in an effort to cut red tape and accelerate deployment.

- Military Integration: The US Army is exploring portable nuclear reactors to secure operational continuity for bases during grid disruptions, lessening the military’s dependence on diesel.

Demand

According to the World Nuclear Organization, about 440 reactors with combined capacity of 390 GWe (gigawatt electric) require 80,000 tonnes of uranium oxide concentrate containing about 67,500 tonnes of uranium from mines (or the equivalent from stockpiles or secondary sources) each year.

Because of the cost structure of nuclear power generation, with high capital and low fuel costs, the demand for uranium fuel is more predictable than probably any other mineral commodity. Once reactors are built, it is cost-effective to keep them running at high capacity and for utilities to make any adjustments to load trends by cutting back on fossil fuel use. Demand forecasts for uranium thus depend largely on installed and operable capacity, regardless of economic fluctuations.

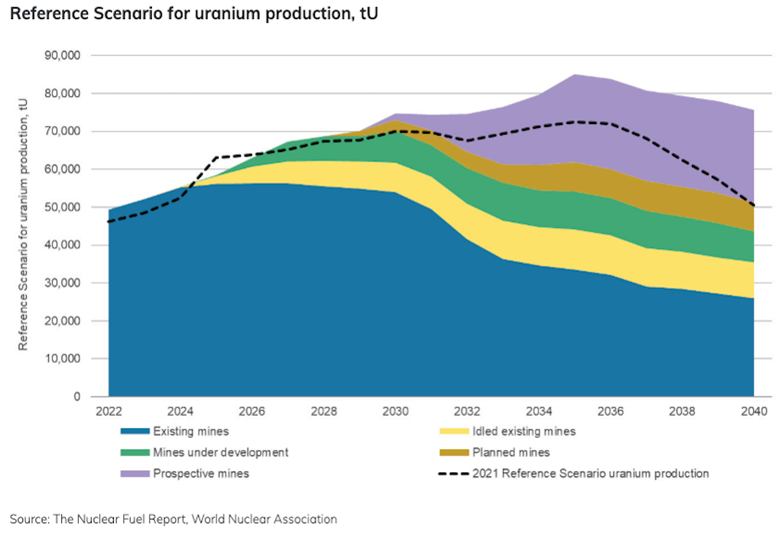

Looking 10 years ahead, the market is expected to grow. The Reference Scenario of the 2023 edition of the World Nuclear Association’s Nuclear Fuel Report shows a 28% increase in uranium demand over 2023-30 (for an 18% increase in reactor capacity – many new cores will be required). Demand thereafter will depend on new plants being built and the rate at which older plants are retired. The Reference Scenario has a 51% increase in uranium demand for the decade 2031-2040.

Licensing of plant lifetime extensions and the economic attractiveness of continued operation of older reactors are critical factors in the medium-term uranium market. However, with electricity demand by 2040 potentially increasing by about 50% from that of 2022, based on the International Energy Agency’s World Energy Outlook 2023 report, there is plenty of scope for growth in nuclear capacity in a world concerned with limiting carbon emissions.

Supply

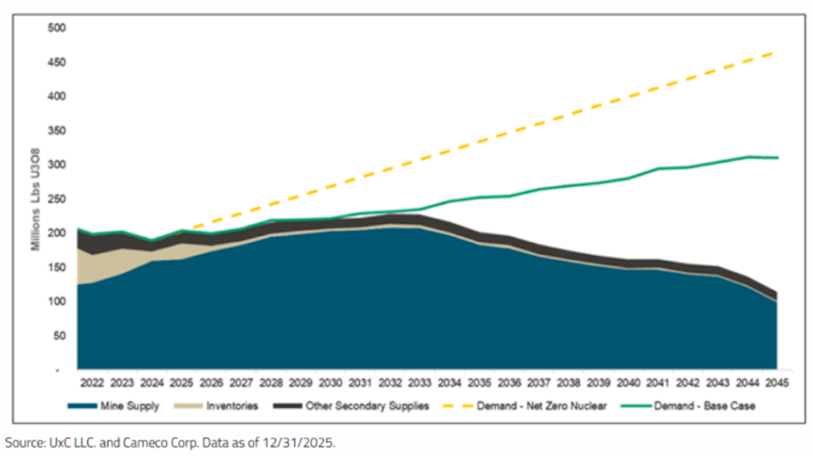

Global uranium mines supplied an estimated 48,000 to 52,000 tonnes (105 million to 115 million pounds) of U3O8 in 2025. This total primary mine supply was well short of the estimated 65,000 tonnes needed to meet global reactor requirements, resulting in a significant structural market deficit. (see section below)

As well as existing and likely new mines, nuclear fuel supply may be from secondary sources including:

- Recycled uranium and plutonium from used fuel as mixed oxide (MOX) fuel.

- Re-enriched depleted uranium tails.

- Ex-military weapons-grade uranium blended down.

- Civil stockpiles.

- Ex-military weapons-grade plutonium as MOX fuel.

The following graph suggests how these various sources of supply might look in the decades ahead. To meet the Reference Scenario requirements from early in the next decade, in addition to restarted idled mines, mines under development, planned mines and prospective mines, other new projects will need to be brought into production.

United States

In a recent report, the Energy Information Administration (EIA) said US production last year more than tripled to 2.1 million pounds of U3O8, a 223% increase over the total produced in 2024.

Among the factors for the increased supply were higher spot uranium prices, government support for nuclear energy and uranium mining, and increasing data center demand for nuclear power.

The report also showed exploration drilling for uranium in 2025 increased almost 66% to just over a million feet, 500 holes more than were drilled in 2024. Combined exploration drilling and development drilling reached the highest levels since 2013.

In June, EnCore Energy (TSXV: EU) received federal approval to build its Dewey Burdock In-Site Recovery (ISR) site in South Dakota, while in April, Ur-Energy (TSX:URE) restarted production at its Shirley Basin mine, shuttered since 1992.

As for uranium imports, the EIA said the top source in 2024 was Canada at 36% of total deliveries, followed closely by Kazakhstan and Australia with 24% and 17% respectively.

Canada

Indeed, Canada is the world’s second largest producer of uranium, accounting for roughly 13% of total global output, states Natural Resources Canada.

The country’s uranium resources are the fourth largest in the world, after those of Australia, Kazakhstan and Russia.

Most of Canada’s reserves are located in the Athabasca Basin of northern Saskatchewan, which hosts the world’s largest high-grade deposits, with grades up to 100 times greater than the average grade of deposits mined elsewhere.

The key producers are Cameco Corporation (TSX:CCO) and Orano Canada Inc.

About 85% of Canada’s uranium production is exported — chiefly to the United States, Europe and Asia.

The remaining uranium is used to fuel domestic CANDU reactors, which currently supply about 15% of the electricity used in Canada. Of the 19 operating CANDU reactors in Canada, 18 are located in Ontario and one is in New Brunswick.

The world’s largest and Canada’s only uranium refinery is located at Blind River, Ontario, where uranium ore concentrates from Canada and abroad are refined to produce uranium trioxide. This product is shipped to a conversion facility in Port Hope, ON, which produces uranium hexafluoride, and also the world’s only commercial supply of fuel-grade natural uranium dioxide. Uranium hexafluoride is exported to produce enriched uranium fuel for light-water reactors in the United States and elsewhere.

Uranium dioxide is shipped to fuel fabrication facilities in Port Hope, Toronto and Peterborough, Ontario, to produce natural uranium fuel for CANDU reactors.

Global

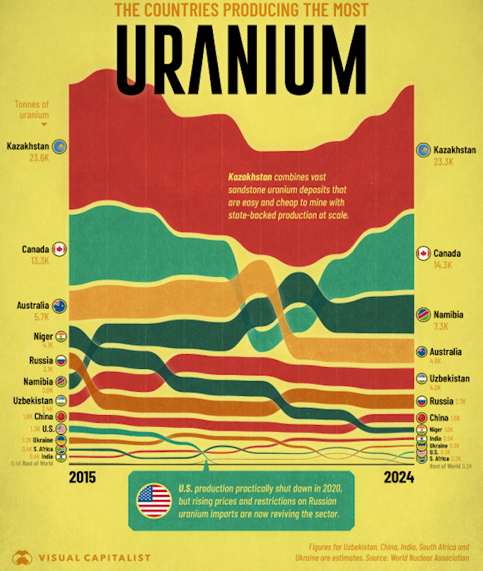

According to Visual Capitalist, Kazakhstan is the world’s dominant uranium producer thanks to low-cost deposits and state-backed scale. The next four biggest producers are Canada, Namibia, Australia and Uzbekistan.

In 2024 the central Asian country produced 23,260 tonnes representing more than one-third of global output.

The country combines large sandstone uranium deposits with low-cost in-situ recovery mining techniques, which are generally cheaper and less labor-intensive than conventional mining. State-backed producer Kazatomprom has also helped scale production efficiently over the last decade.

Visual Capitalist notes that uranium production in Canada had collapsed in 2020 due to mine shutdowns and weak market conditions, but the restart of major projects such as Cigar Lake and McArthur River helped drive a sharp recovery.

US uranium production nearly disappeared in 2020, falling to just 6 tonnes, but the sector has started recovering amid higher prices and geopolitical concerns surrounding global supply chains. Restrictions on Russian uranium imports have also increased interest in rebuilding domestic production capacity.

Even with the recent rebound, US production remains far below historical levels. In 2024, the country produced just 260 tonnes of uranium, a fraction of Kazakhstan’s output, the site states.

Another factor concerns Niger, the world’s eighth largest producer.

One source reports the Republic of Niger has revoked any rights that French state-owned Orano had to the Arlit deposit in northern Niger. The revocation of Arlit effectively locks Orano out of future uranium development in the region.

More importantly,

Niger has increasingly moved toward the Russia-backed Alliance of Sahel States, while at the same time Chinese and Russian influence across African uranium districts continues expanding. Namibia has already seen increasing ownership by Eastern-aligned companies while countries like Zambia and Botswana remain among the few large African uranium jurisdictions still substantially controlled by Western interests.

That raises a broader strategic question. Where will Western utilities secure future uranium supply? Australia holds the world’s largest uranium reserves but still faces various legal and permitting constraints across several states. Canada meanwhile remains one of the most mining friendly jurisdictions globally and hosts the world’s highest grade uranium deposits, though even Canada has recently faced operational disruptions from flooding and wildfires in Saskatchewan’s Athabasca Basin.

For investors, this matters because uranium is increasingly becoming a strategic geopolitical resource rather than simply a commodity. As Western access to global supply narrows, high quality projects in stable jurisdictions such as Canada, the United States and Australia become materially more valuable.

Shortage forecast

As mentioned, the demand for uranium is outstripping supply.

In January, research by Teniz Capital said the global uranium market is entering a “tipping point” where sustained demand for the nuclear fuel and supply constraints could see prices rally in the coming years.

The UAE-based investment bank put out a report saying the market has reached what analysts believe to be an acute structural deficit that is incapable of meeting demand due to the slow pace of mine development and years of underinvestment. Demand, meanwhile, is projected to rise 28% by the end of the decade and double by 2040.

According to Teniz, mines can only cover 74-90% of current needs. While in the past the gap could be met with secondary sources, now these have largely been depleted as well.

The current project pipeline is effectively exhausted and developing new mines could take 10-15 years, it added.

“The supply deficit in the 2030s is already programmed. It cannot be eliminated by any political decisions or investments. The physical constraints of time are insurmountable,” the report said, warning that even higher uranium prices would not offer a quick fix.

According to Sprott Asset Management, via Canadian Mining Journal, the global uranium market entered 2026 with great momentum. Spot prices surged by about a quarter in January, rising above $100 a pound for the first time in two years.

Sprott analyst pointed to the Trump administration’s Section 232 framework on critical minerals as a key catalyst, as it explicitly proclaims uranium’s importance to US energy and national security.

A heightened strategic status could lead to further policy support and tangible actions taken by the US government, such as the recently announced $2.7 billion funding to strengthen domestic

uranium enrichment services over the next decade, the report noted.

“More broadly, these actions sit within a clear ambition to quadruple US nuclear capacity by 2050, including another target to have 10 new large reactors under construction by 2030. If the US were to quadruple nuclear capacity, it would require an extraordinary amount of incremental uranium supply,” Sprott’s ETF products director Jacob White wrote.

White hypothesized that the US government could begin taking equity stakes in uranium miners in exchange for offtake agreements, and that supply would be constrained in the coming year unless higher uranium prices are realized.

Sprott’s report also highlighted the slow pace of mine development and an underinvested supply base are set to widen the market deficit.

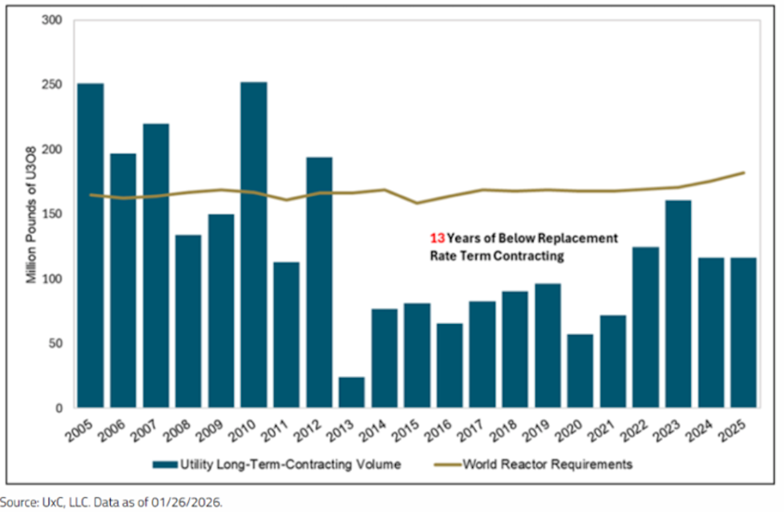

Furthermore, contracting is in catch-up mode. Nuclear utilities buy uranium ahead of time through long-term contracts. But contracting undershot the replacement rate for a 13th straight year in 2025, pushing uncovered needs into the future.

Price forecasts

“Major financial institutions are generally forecasting uranium to stay elevated over the next few years, with most calls clustering in the roughly $65 to $110 per pound range, and some bullish banks seeing spikes to $125 to $135 per pound.”

That quote accurately reflects the consensus. Financial institutions —including Bank of America and Sprott Asset Management — foresee elevated uranium prices driven by fundamental supply and demand imbalances.

Here are the key factors underpinning these elevated price forecasts:

- Structural Supply Deficits: Global nuclear capacity consumes roughly 180 million pounds of U3O8 annually, while mine production delivers only about 150 million pounds. New mine supply is slow to develop, requiring years to permit and build.

- Utility Contracting Catch-Up: Years of under-contracting have resulted in coverage gaps for utilities. With competition rising, long-term contracting has moved above the $85 per pound threshold.

- Policy Tailwinds & AI Demand: Uranium was added to the US critical materials list, and energy-hungry AI data centers have spurred significant new investments in nuclear capacity.

According to Trading Economics,

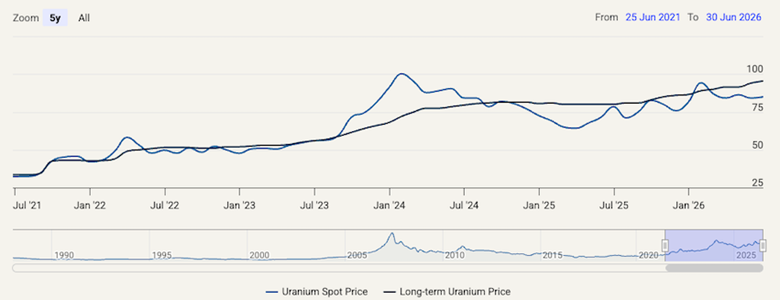

Uranium futures in the US remained near $85 per pound, trading in a narrow range since early April after erasing the surge from earlier in the year. The cooldown from the speculative rally was combined with muted levels of spot buying by utilities, which have allocated from long-term contracts since the war between Russia and Ukraine raised short-term trade uncertainty. Yellowcake prices were lifted by geopolitical tension driving power markets in major economies to be increasingly volatile, sparking interest in nuclear power by governments and power-hungry AI hyperscalers that develop datacenters. Italy was the latest to express interest to approve a legal framework to restore nuclear power, in line with measures from the US and Japan as power consumers expand sources for generation to account for the higher demand from data center projects. Meta, Amazon, and Microsoft signed agreements to gain fresh nuclear capacity for their future AI data center operations.

In the uranium market, the spot price represents immediate, short-term physical deliveries (usually within 12 months), while the term price applies to multi-year contracts for delivery stretching out over two to 10+ years. Buyers and sellers negotiate contracts privately.

Spot pricing is highly volatile, whereas term pricing reflects structural supply and utility procurement strategies.

The spot market is thin and primarily driven by financial institutions (like the Sprott Physical Uranium Trust) and traders. Because it handles a much smaller volume, a sudden influx of buying or dumping of inventory can cause rapid, sharp swings in the spot price.

Historically, the spot price has often traded at a discount to the term price because term contracts include a premium for supply security.

At the end of May, the long-term uranium price jumped sharply to $93 per pound, up $3 in a single month which is one of the largest monthly increases in recent history.

One source said this “continues to reinforce the growing disconnect between near term spot fluctuations and the much more strategically important long term contracting market.

“Forward pricing also remained firm, with the three-year forward price sitting at $100 and the five-year forward price at $107, suggesting utilities and fuel buyers continue to anticipate materially tighter supply conditions ahead.

“For investors, the key takeaway is that while spot prices may continue to fluctuate week to week, the long-term market is quietly sending a much stronger signal about future uranium scarcity and utility urgency.”

Enrichment and conversion

Uranium conversion and enrichment capabilities are highly concentrated globally. Russia (via Rosatom) possesses the most significant combined capacity, holding approximately 46% of global enrichment and 20% to 40% of conversion capacity. Other major global players include China, France (via Orano), the United States, and the Urenco consortium (operating in the UK, Netherlands, and Germany).

Canada

Uranium mined in the Athabasca Basin is the highest-grade in the world, but it is not directly usable in most reactors. Conversion and enrichment are required to transform the raw mined product into nuclear fuel, and to secure a reliable supply chain for the West.

Before the enrichment process can occur, uranium must first go through conversion. The processed yellowcake is transformed into uranium hexafluoride gas, which is the required physical state for enrichment facilities to separate the U-235 isotopes.

- Security of Supply: The Athabasca Basin accounts for approximately 20% of the world’s primary uranium supply. Developing domestic and Western conversion and enrichment capacity is critical to energy independence.

- Reducing Reliance: Geopolitical tensions have highlighted a vulnerability in the West’s nuclear fuel supply chain, as foreign entities historically control large percentages of global conversion and enrichment capacity. Expanding these stages of the fuel cycle ensures energy security.

United States

US commercial enrichment capacity is approximately 4.8 million SWU (Separative Work Units) annually. This is supplied entirely by the Urenco USA facility in Eunice, New Mexico, meeting about one-third of current US reactor demand.

In May, two nuclear energy giants, NextEra and Dominion Energy, merged to create the world’s largest electric utility by market capitalization. The combined company will control 15 nuclear reactors across eight power stations throughout the southern United States.

According to the above-cited source, “the merger… highlights a growing problem that the uranium market keeps circling back to. Where will the fuel come from?

“The United States currently produces only a fraction of the uranium it consumes and remains heavily dependent on imports. While domestic uranium production has begun recovering modestly, it remains nowhere near sufficient to support a major expansion of the reactor fleet. That means future demand growth likely pushes the U.S. further toward allied uranium suppliers such as Canada and Australia.

“At the same time, Australia still faces regulatory and political hurdles to significantly expanding production, while new uranium mines globally continue facing long permitting timelines, capital intensity and growing geopolitical complexity.

“The reality is that new reactors, whether conventional large scale plants or emerging SMR fleets, cannot materialize at scale without corresponding growth in uranium mining and fuel cycle infrastructure.”

However, the United States has been moving to revive domestic uranium enrichment through a $1.07 billion nuclear fuel push.

According to Interesting Engineering, a new Department of Energy contract positions Centrus Energy (NYSE:LEU) to scale High-Assay, Low-Enriched Uranium (HALEU) production in Ohio, with commercial operations expected later this decade.

The $1.07B contract is a major step in the country’s effort to rebuild its uranium enrichment industry. The agreement includes a $900 million order for commercial-scale enrichment infrastructure and also gives the DoE options to purchase up to $170 million worth of HALEU.

Interesting Engineering notes the award shifts Centrus from a government-backed demonstration program to commercial production. The company expects its first new large-scale enrichment capacity to enter service in 2029.

Centrus plans to build commercial HALEU production capacity at its American Centrifuge Plant in Piketon, Ohio. The first phase aims to produce 12 metric tons of HALEU annually while also adding enough conventional low-enriched uranium (LEU) capacity to address the company’s existing $2.4 billion LEU order backlog.

Cosa Resources (TSXV:COSA, OTCQB:COSAF)

Murphy Lake North is a 70/30 joint venture between Cosa Resources (TSXV:COSA, OTCQB:COSAF) and Denison Mines (TSX:DML), located at the northern end of the Larocque Lake Trend, in the Eastern Athabasca Basin of Saskatchewan.

The project is within 3 kilometers of and on trend with the Hurricane deposit, discovered in 2018 by Cosa’s management; Hurricane currently holds the title as the world’s highest-grade Indicated uranium resource.

On March 24, 2026, Cosa reported that its first hole of the winter drill program at Murphy Lake North intersected 5.0 meters of anomalous radioactivity. Chemical assays showed 1.7% triuranium octoxide (U3O8) within a broader interval of 5.0m of 0.55% U3O8.

Cosa has started its largest-ever drill program at Murphy Lake North. Summer drilling is expected to comprise approximately 15 drill holes totaling 6,000 meters, and will follow up winter 2026 drilling, which saw multiple intersections of unconformity-related uranium mineralization.

The mineralization remains open along strike for 600 meters in both directions. Drilling will focus on step-out tests of the Cyclone Trend mineralization about 265 meters below surface.

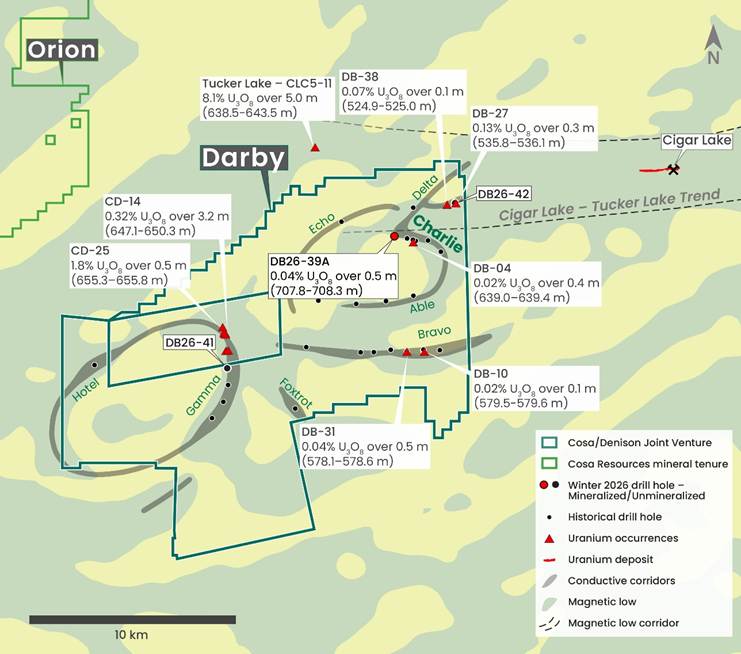

The roughly two-month program will be followed by drilling at the company’s Darby Joint Venture. Ownership in this project is also split 70/30, with Cosa holding the majority stake and Denison 30%.

Drilling at Darby is planned to comprise up to 2,000 meters at the Gamma and Bravo trends.

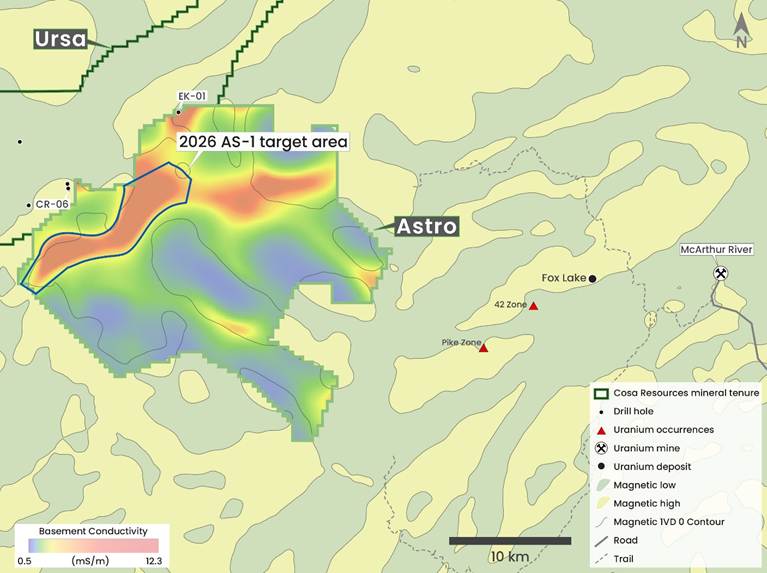

In April 2025, Cosa announced the signing of an option agreement to allow Global Uranium (CSE:GURN) to earn up to 80% of the company’s Astro Project over five phases. The four-year deal commits Global to spend CAD$9.5 million on exploration and complete cash and share payments.

On June 26, Cosa announced the start of an ambient noise tomography (ANT) survey at Astro, located about 28 km west of Cameco’s McArthur River uranium mine. The Global-funded survey and supporting work will identify seismic anomalies potentially attributable to prospective geological features including unconformity offsets and zones of strong hydrothermal alteration.

Results of the survey will guide proposed follow-up ground EM surveying and an inaugural drill program targeted for 2027.

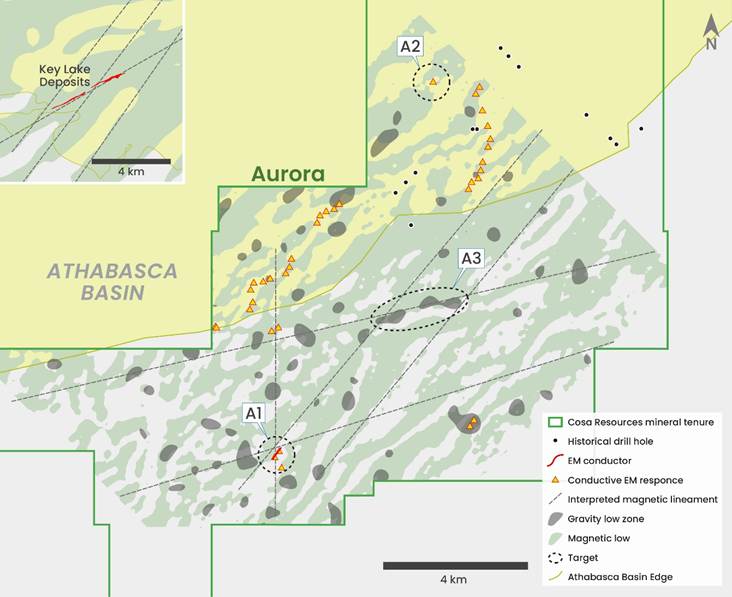

On June 25, Cosa announced the start of a property-wide airborne radiometric survey at the Aurora Project, located in the southeastern Athabasca Basin approximately 16 km east of Cameco’s Key Lake Mill and historical mine.

Aurora is under option by Traction Uranium (CSE:TRAC), which can earn 80% of the project by spending over CAD$9 million in exploration, plus cash and share payments totaling $1.5 million and 5 million shares.

The Traction-funded radiometric survey will be flown at 50-meter line spacings with the objective of identifying radiometric anomalies potentially indicative of near-surface uranium mineralization.

The results will be used to guide a proposed 100% partner-funded fall drill program at Aurora — following the completion of drilling at Murphy Lake North and Darby.

Cosa is fully funded for 2026 exploration and beyond, especially considering that two of the four projects slated for drilling are being funded by option agreement partners. Denison will cover the exploration costs at Murphy Lake North and Darby to the point where they retain their 30% interest in both properties.

On June 24, the company said it had closed its previously announced bought deal private placement, upsized to CAD$12 million.

Cosa’s largest shareholder, Denison Mines, participated in the offering pursuant to its pre-emptive and top-up rights under the investor rights agreement between Denison and Cosa dated Jan. 14, 2025. Following the closing of the offering, Denison owns 17.7% of Cosa on a partially diluted basis.

Cosa’s mantra seems to be “drill, baby drill” and with four projects slated to be drilled this year or next, it appears they won’t stop until they make a discovery.

Cosa is getting exposure to retail investors not only through my site, but through Rick Rule’s 2026 Rule Symposium on Natural Resource Investing being held in Boca Raton, Florida, July 6-10. CEO Keith Bodnarchuk is attending.

You can’t just sign up to exhibit at Rule’s conference; you must be invited. It’s another indication that Cosa Resources is onto something substantial and is being recognized by Rule, one of the industry’s most well-respected investors and conference speakers.

Remember, Cosa has already hit 1.7% U3O8 within a 5-meter interval at Murphy Lake North after receiving scintillator counts (a measure of radioactivity) reaching 13,900 CPS.

Presumably, the “scint” counts will be released as Cosa drills and investors can interpret them and make their decisions accordingly.

I’m excited at the prospect of four drill programs in the Athabasca Basin and possibly making a discovery rivaling the Hurricane deposit.

Cosa Resources Corp.

TSXV:COSA, OTCQB:COSAF

Cdn$0.65 2026.07.08

Shares Outstanding 116.1m

Market Cap Cdn$87.1m

COSA website

Richard (Rick) Mills

aheadoftheherd.com

Subscribe to AOTH’s free newsletter

Richard owns shares of Cosa Resources Corp. TSXV:COSA

COSA is a paid advertiser on his site aheadoftheherd.com.

This article is issued on behalf of COSA.

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.

{kind=link}

{kind=link}

{kind=link}