Nuclear making a comeback but uranium supply squeezed – Richard Mills

2026.05.14

Forecasted demand for oil is expected to drop for the first time since the pandemic owing to what the International Energy Agency calls “the most severe oil supply shock in history.”

On April 23, Faith Birol, secretary general of the IEA, told CNBC that the war in the Middle East and the closure of the Strait of Hormuz have created the largest energy security threat the world has ever faced.

“As of today, we’ve lost 13 million barrels per day of oil … and there are major disruptions in vital commodities,” Birol said.

Four days later, he repeated his concerns to The Guardian, stating

“There will be a significant boost to renewables and nuclear power and a further shift towards a more electrified future.” He added this would result in oil demand loss that will be permanent. (Oilprice.com)

Oil and gas vulnerability swaying countries to renewables — Richard Mills

A nuclear renaissance

Global nuclear capacity is projected to increase by 13% by 2030 and nearly 87% by 2040, with massive growth in China and India.

Nuclear power is increasingly considered crucial for meeting carbon-free targets, with high demand from data centers and technology companies seeking reliable, clean power.

Grant Isaac, President and COO of Cameco (TSX:CCO), which mines uranium and builds nuclear reactors through its 49%-owned Westinghouse Electric joint venture, recently told the Northern Miner “I’ve never been more excited about the prospects for nuclear new builds globally and in particular in the West.”

Isaac noted the last time the West built out fleet-scale gigawatt reactors was during the Middle East energy crisis in the 1970s — a crisis seemingly repeating itself with the US/Israel war with Iran.

“Now we’re worried about climate security, worried about where our alternative energy is coming from, and in the grips of a national security conversation around the need for 24-hour, carbon-free electrons for things like the data race and the onshoring of supply chains. That combination of climate, energy and national security is a great backdrop for strengthening the tailwinds to nuclear new build.”

Demand drivers

To fully understand the market for nuclear energy and uranium, the primary feedstock for nuclear reactors, we need to back up a few years.

The 1986 Chernobyl disaster and the Three Mile Island accident a few years prior, sowed fear and doubts about nuclear power, which had earned a safe reputation since the first plants were built in the 1950s.

Then came the 2011 Fukushima nuclear meltdown in Japan, when powerful tsunami waves cut power to the complex, swamped the cooling systems and caused hydrogen explosions in three of the units.

Trust in nuclear took a huge hit, with Germany vowing to close all its nuclear plants, Japan, which relies heavily on the technology, temporarily shuttering all its plants for safety inspections, and the uranium price cratering.

A revival began in 2022 with increased demand for nuclear and higher uranium prices. Some mothballed projects were restarted.

In 2023, nuclear output finally crept past its 2010 peak.

According to the World Nuclear Association, electricity demand is increasing about twice as fast as overall energy use and is likely to rise by more than half between 2022 and 2040.

Nuclear power provides about 10% of the world’s electricity.

The need for nuclear energy is based upon a simple premise: the expected rise in population and their hunger for commodities.

WNA states that growth in the world’s population and economy, coupled with rapid urbanization, will result in a substantial increase in energy demand over the coming years. The United Nations estimates that the world’s population will grow from about 8 billion in 2024 to around 9.8 billion by 2050.

Increased electrification of end-uses – such as transport, space cooling, large appliances, and ICT [Information and Communication Technologies] – are key contributors to rising electricity demand… despite significant progress, around 9.6% of the world’s population – about 760 million people – living mostly in rural areas, were without access in 2022…

The WHO [World Health Organization] estimates that about seven million people die prematurely as a result of air pollution. Much of the fine particulate matter in polluted areas arises from industrial sources such as power generation or from indoor air pollution which could be averted by electricity use.

Nuclear energy is a low-emitting source of electricity production and is also specifically low-carbon, emitting among the lowest amount of carbon dioxide equivalent per unit of energy produced when considering total life-cycle emissions. It is the second largest source of low-carbon electricity production globally (after hydropower) and provided about 26% of all low-carbon electricity generated in 2022. Almost all reports on future energy supply from major organizations suggest an expanded role for nuclear power is required…

WNA cites the characteristics of nuclear power that make it particularly valuable:

- Fuel is a low proportion of power cost, giving power price stability, its fuel is on site (not depending on continuous delivery), it is dispatchable on demand, it has fairly quick ramp-up, it contributes to clean air and low-CO2 objectives, and it gives good voltage support for grid stability.

- Apart from hydropower in the few places where it is very plentiful, all the renewables have limitations, either intrinsically or economically, in potential use for large-scale power generation where continuous, reliable supply is needed.

Source: World Nuclear Association

- Natural gas is increasingly used as fuel for electricity generation in many countries. The challenges associated with transport over long distances and storage are to an extent alleviated through liquefaction. However, much storage remains underground in depleted oilfields, especially in the US, and this can be dangerous. In 2015 the Aliso Canyon storage field in California leaked for months, releasing about 66 tonnes of methane per hour, causing widespread evacuation and neutralizing the state’s efforts to curb carbon emissions (methane has over 25 times greater global warming potential than carbon dioxide).

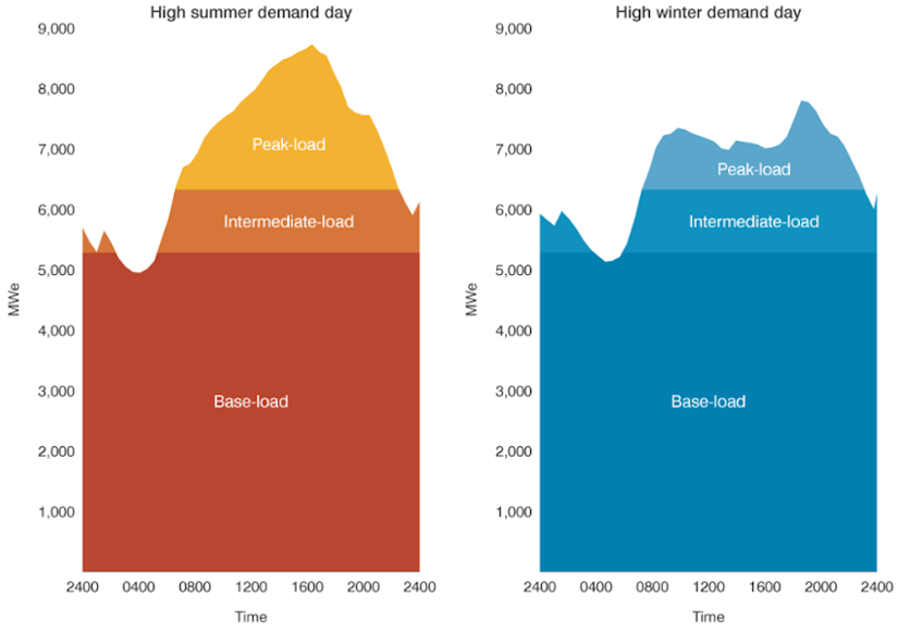

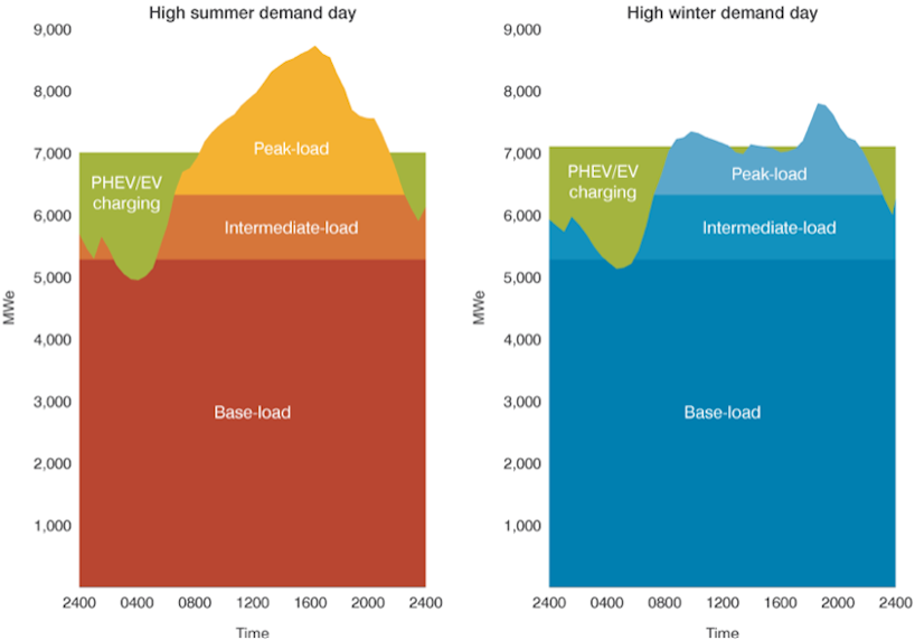

- Overnight charging of electric vehicles will greatly increase the proportion of system capacity to be covered by baseload power generation — either nuclear or coal. In a typical system this might increase from about 50-60% to 70-80% of the total, as shown in the figures below.

- This then has significant implications for the cost of electricity. Baseload power is generated much more cheaply than intermediate- and peak-load power, so the average cost of electricity will be lower than with the present pattern of use. And any such major increase in baseload capacity requirement will have a major upside potential for nuclear power if there are constraints on carbon emissions.

- A major topic on many political agendas is security of supply, as countries realize how vulnerable they are to interrupted deliveries of oil and gas. The abundance of naturally occurring uranium makes nuclear power attractive from an energy security standpoint. As carbon emission reductions are encouraged through various forms of government incentives and trading schemes, the economic benefits of nuclear power will increase further.

The Associated Press writes that, 40 years after Chernobyl, more countries are turning to nuclear power, “a trend that has been given a big boost by war in the Middle East.”

(Statista reports, and displays in an infographic, that one of the most common responses to the war has been the introduction of emergency subsidies and direct financial support. Several governments have also implemented temporary fuel price caps to limit the impact of rising costs on households and businesses. Others have turned to demand-reduction policies such as shorter work weeks. The most severe responses involve direct intervention in fuel distribution. India and Bangladesh, for example, have introduced export restrictions and prioritized fuel allocation to essential sectors.)

Over 400 nuclear reactors are operational in 31 countries, while about 70 more are under construction. Nuclear power accounts for producing about 10% of the world’s electricity, equivalent to about a quarter of all sources of low-carbon power…

The United States is the world’s largest producer of nuclear power, with 94 operational reactors accounting for about 30% of global generation of nuclear electricity. And it is increasing efforts to develop nuclear energy capacity with a goal to quadruple it by 2050.

“The world cannot power its industries, meet the demands of artificial intelligence, or secure its energy future without nuclear power,” U.S. Undersecretary of State Thomas DiNanno said last month.

China operates 61 nuclear reactors and is leading the world in building new units, with nearly 40 under construction with a goal to surpass the U.S. and become the global leader in nuclear capacity.

European Commission chief Ursula von der Leyen has acknowledged that it was Europe’s “strategic mistake” to cut nuclear energy and outlined new initiatives to encourage building power plants.

Russia, meanwhile, has taken a strong lead in exporting its nuclear know-how, building 20 reactors worldwide…

Ukraine still relies heavily on nuclear plants to generate about half of its electricity…

Japan has restarted 15 reactors after reviewing the lessons of the earthquake and tsunami that damaged the Fukushima plant, and 10 more are in the process of getting approval to restart…

With 57 reactors at 19 plants, France relies on nuclear power for nearly 70% of its electricity… In 2022, President Emmanuel Macron announced plans to build six new pressurized water reactors…

The COVID-19 pandemic, combined with the gas supply crunch triggered by the conflict in Ukraine, “revealed the limits of deploying renewable electricity and Europe’s dependence on gas,” said Nicolas Goldberg, a partner at Paris-based Colombus Consulting.

Who’s building?

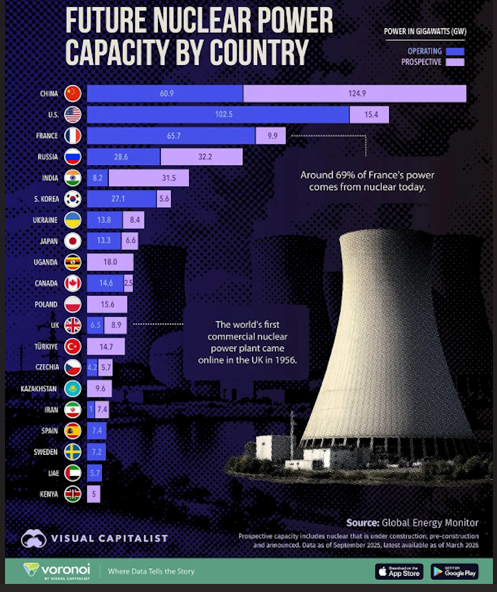

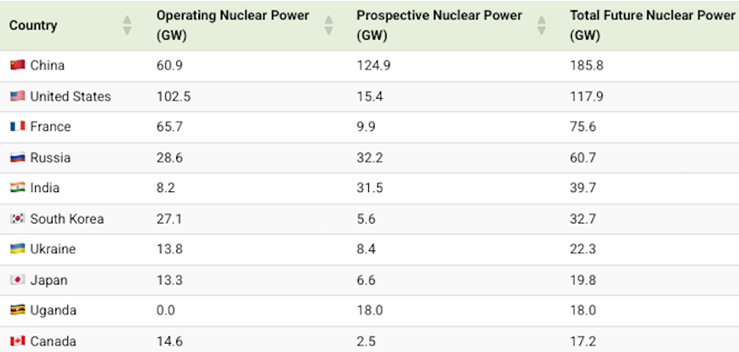

The below infographic by Visual Capitalist ranks the countries building the most nuclear power.

While the United States currently leads the pack, China is set to become the dominant nuclear power producer. Based on existing and planned projects, its total capacity could reach 186 gigawatts compared to the US’s 118 GW and France’s 75,590 megawatts.

India reportedly has 24 operating reactors and a current generating capacity of about 8 gigawatts. The country is planning to deploy dozens more to reach 100 gigawatts by 2047.

New Delhi has already selected six Westinghouse-made AP1000 reactors as part of its strategy, and other orders are likely, the above-mentioned Cameco Chief Operating Officer Grant Isaac said.

SMRs and Big Tech

Oilprice.com describes small modular reactors (SMRs) as advanced nuclear reactors with a power capacity of up to 300 MW(e) per unit, equivalent to about one-third the generating capacity of a conventional nuclear reactor. SMRs are much smaller than traditional reactors and are modular, making it easier to assemble them in factories and transport them to the site. Because of their smaller size, SMRs can be installed on sites that are not suitable for conventional reactors. They are also significantly cheaper and faster to build than traditional nuclear reactors and can be constructed incrementally to meet the growing energy demand of a site…

Small modular reactors gaining traction powered by AI — Richard Mills

Demand for them is being driven by the exponential increase in computing power demanded by artificial intelligence, particularly data centers. A single hyperscale data center can demand 100 megawatts or more, with a monthly consumption equivalent to the annual electricity demand of thousands of homes. (AI Overview)

Big Tech sees nuclear as the solution to their electricity needs and is investing billions of dollars in both conventional nuclear and SMRs.

Google became the first company to sign an agreement with Kairos Power, a developer of molten salt-based SMRs.

The deal paves the way for up to 500 megawatts of nuclear-generated electricity to power Google’s data centers.

Three nuclear companies are leading the race to build small nuclear reactors in the US. They are TerraPower, X-Energy and Kairos Power.

All of them are private but with significant financial backing, often from tech companies, and customers lined up, states CNBC.

TerraPower broke ground on its first plant, near a former coal site in Wyoming, in 2024. The company aims to start dispatching power by the end of 2030 to Warren Buffett’s PacifiCorp. The Natrium reactor has a power capacity of 345 megawatts, enough for more than 250,000 homes.

The same year, Holtec International secured a $1.5 billion loan guarantee from the US Department of Energy to reopen the Palisades nuclear plant in Michigan which was closed in 2022. According to Wall Street commodities investment firm Goehring & Rozencwajg (G&R), Holtec plans to install two SMRs on the site, adding 600 megawatts of new capacity while leveraging existing infrastructure.

X-Energy secured hundreds of millions of dollars from Amazon to build its Xe-100 reactor. The Xe-100 is an 80-megawatt reactor sold in a pack of four units to construct 320 megawatts in total.

Amazon’s investment will finance four Xe-100 reactors in Washington state that will be built, owned and operated by Energy Northwest, a utility, with plants coming online in the early 2030s. The intent is to scale up to a dozen Xe-100s in Washington.

X-Energy is also working with Dow to deploy four reactors at the chemical company’s manufacturing in Seadrift, Texas, CNBC states.

Kairos Power signed a contract with Alphabet’s Google unit to deploy multiple advanced reactors, aiming to supply YouTube with 500 megawatts of power. The first reactor is expected to come online in 2030, with additional deployments through 2035.

CNBC notes the 75-megawatt Kairos’ reactor will be deployed in pairs to provide 150 megawatts of total power. Kairos is building a low-power, demonstration reactor in Oak Ridge, Tennessee to showcase its ability “to deliver clean, safe, and affordable nuclear heat.”

Meta Platforms, which owns Facebook, is apparently exploring various deals for carbon-free energy, with SMRs high on the list.

Conventional nuclear power plants haven’t been left out of Big Tech’s moves to secure more electricity for its data centers. Microsoft is reportedly working with Constellation Energy to reopen the Three Mile Island Unit 1 reactor which has been shuttered since 2019. The tech giant would purchase all the electricity generated by the plant at a rumored +100% premium above wholesale prices.

In a summation, G&R writes:

These announcements underscore a simple but powerful truth: long-maligned and underutilized nuclear power is the only viable solution for the energy-intensive demands of the modern world. Over the past several years, we’ve had to increase our uranium demand estimates by nearly 40 million pounds as plant closures have been deferred and new-build plans have accelerated. With the introduction of SMRs, offering even greater efficiency and safety, the nuclear industry is poised to take another transformative leap.

US government support

The US government has also been working to accelerate nuclear’s rebound through various supports.

President Trump in a 2025 executive order aimed to quadruple American’s nuclear energy capacity to ~400 gigawatts by 2050.

Last October, Washington announced it is partnering with Westinghouse Electric to build at least $80 billion in nuclear reactors. The agreement is with Westinghouse Electric’s owners, Canadian uranium miner Cameco and Brookfield Asset Management.

In March of this year, President Trump and the Japanese Prime Minister, Sanae Takaichi, announced a nuclear power project in the southern US that is part of a $550 billion fund the two countries agreed to when negotiating a trade truce. A White House fact sheet says GE Vernova and Hitachi will build BWRX-300 SMRs in Tennessee and Alabama at a cost of up to $40 billion.

Mining.com reported that nuclear regulatory authorities in April approved a 20-year licence renewal for the two pressurized water reactors at California’s Diablo Canyon nuclear power plant — the 100th such extension in several years.

The most recent initiative is the DoE’s “Nuclear Dominance – 3 by 33” campaign, through which a consortium of 90+ companies aims by 2033 to catalyze a secure and cost-competitive domestic fuel supply chain and accelerate advanced reactor deployment.

Uranium supply deficit is here

Like the nuclear industry, the uranium market is also on the cusp of a remarkable transformation.

Uranium is benefiting from a paucity of supply compared to demand.

Current global uranium usage is about 180 million pounds a year. But mines only produce 130 million pounds, leaving a 50-million-pound shortage..

Meanwhile, demand is about to explode, with the World Nuclear Association projecting uranium demand will jump 28% by 2030.

A Mining.com infographic identifies which regions host the most nuclear reactors in operation and under construction, and how much uranium is required to keep them running.

Globally there are 438 operating reactors, with East Asia edging out North America by 117 to 113. Third is the European Union at 99. East Asia has by far the most under construction at 38. North America has none being built.

By 2030, East Asia will have the most installed nuclear generating capacity, @ 157.8 GWe (gigawatt electric) net, and the most annual reactor-related uranium requirements @ 25,448 tonnes U/yr. Next is North America, followed by the European Union, non-EU Europe, the Middle East, Central Asia and South Asia grouping, and Africa.

The World Nuclear Association says its 2025 base-case scenario of 398 GWe of installed nuclear generating capacity is expected to reach 746 GWe by 2040, a 90% increase from current levels.

Uranium fuel requirements are predicted to also rise by 90%, with reactor demand reaching 330 million pounds by 2040, compared to 179.1 million pounds this year.

In an upper-case scenario, fuel requirements could hit 530 million pounds.

Even the most conservative projection puts 2040 demand at 278 million pounds — almost 100 million pounds more than current consumption.

G&R, the Wall Street commodities investment firm, says Given these enormous growth assumptions, the expansion of uranium supply over the next fifteen years will be critical.

But there’s a problem.

G&R notes the uranium market fell into deficit in 2025 and expects the same in 2026, with uranium supply down and reactor demand up.

Identified supply problems include Kazatomprom struggling to expand its production base. The world’s largest uranium producer now expects to produce only 62 million pounds of uranium in 2026 — 5 million pounds less than the 2025 level — and a massive reduction from the 85-million-pound figure once presented as achievable.

Meanwhile, the West’s largest uranium producer, Cameco, has also been forced to trim its 2025 production guidance for the McArthur River mine, lowering its forecast to 14-15 million pounds due to development delays and slowed progress on ground-freezing operations.

This week, Cameco temporarily halted production at its Key Lake mill and reduced activity at the mine after flooding in northern Saskatchewan damaged transportation infrastructure.

As for new supply, G&R expects there will be construction delays at NexGen Energy’s Arrow/Rook I project in Saskatchewan. Despite getting all the permits required except one, authorization from the Canadian Nuclear Safety Commission, which, if granted, would imply initial uranium output in early 2030, we believe there is a meaningful risk that Rook’s schedule will slip

NexGen is confident it can meet its aggressive timetable. But given the realities of northern Saskatchewan—its climate, its infrastructure limitations, its logistical constraints — we believe holding to that schedule will be extremely difficult.

The firm notes the last uranium mine built in Canada, Cameco’s Cigar Lake, was eight years behind schedule.

Rook is projected to begin production at 21 million pounds per year, ramping to as much as 30 million pounds — a contribution unmatched by any other new uranium project over the next decade. Any delay in achieving those volumes will further widen the global uranium market’s structural deficit, particularly as demand accelerates into the 2030s.

Growing supply risks and tightening markets have led to prices in 2025 reaching USD$86.50 per pound.

World Nuclear Association data confirms uranium demand already outpaces production by 50 to 60 million pounds a year. Worldwide demand for uranium is projected to triple by 2040.

The Northern Miner cites RBC Capital Markets mining analyst Andrew Wong, who wrote, “Uranium market fundamentals remain tight.” Wong predicts “accelerating momentum in nuclear new builds.”

In a $1.9 billion deal, Cameco in March agreed to supply almost 22 million pounds of uranium ore concentrate to India over nine years. Deliveries would start in 2027 and run through 2035.

New Delhi’s decision to buy uranium from Cameco and Kazatomprom “sends a very bullish signal,” Sprott Asset Management CEO John Ciampaglia, who runs the world’s biggest physical uranium fund, said in an interview posted on the firm’s website.

“This should signal to the market that everybody needs to get in line to lock down their own supply because these big state-owned entities are doing exactly that.”

In another sign of supply tightness, data compiled by Cameco says uncovered requirements by global utilities are estimated at about 3.1 million pounds of uranium concentrate through 2045. The shortfall “is bigger than it’s ever been in the history of the uranium market,” Cameco’s COO Grant Isaac says.

Uncovered uranium requirements refer to the large volume of fuel needed by nuclear utilities that is not yet secured through long-term contracts.

US uranium dependency

The US is the top nuclear producer but relies heavily on imports, with 98% of its supply coming from foreign sources in 2026, notes the US Energy Information Administration.

Canada provides roughly 33% of US uranium, with 90% of Canadian production available for export.

According to the World Nuclear Association, just three countries — Kazakhstan, Canada and Namibia — control nearly 75% of global uranium production. “Such a high concentration of countries,” states Firstpost, “means these countries may have a veto over who can develop nuclear energy programmes — or nuclear weapons.”

Another vulnerability from a US standpoint is Russia, which dominates the small but highly strategic market for enriched uranium.

The global market for enriched uranium is expected to expand significantly in coming decades as several countries invest in nuclear expansions. Oilprice.com reported:

A report published by the World Nuclear Association in September said that the global demand for uranium is expected to increase by almost a third to around 86,000 tonnes by 2030 and to rise to 150,000 tonnes by 2040. However, to meet this demand while decreasing reliance on Russian uranium, several countries will need to invest in accelerated permitting, mining innovations, and new exploration for uranium…

[The US] commenced large-scale exploration drilling activities in 2024, in a bid to reduce reliance on Russia, drilling 1,324 holes. Under the Biden administration, the U.S. Department of Energy worked to expand domestic commercial LEU [Low Enriched Uranium]. Before leaving office, in December [2024], Biden announced the selection of six companies from which it can sign contracts to procure LEU to incentivise the development of new uranium production capacity in the United States…

The global demand for enriched uranium is expected to grow significantly in the coming decades in response to a nuclear revival in several countries. However, producing the uranium needed to fuel a new nuclear era will be extremely complex, due to the strict sectoral regulations and the current limited global production capacity. Greater funding must be invested in research and development, as well as into new production facilities around the globe to support the world’s nuclear energy aims.

Pricing

US uranium futures are currently trading at $86.30 a pound, about one-third higher than a year ago. In January of this year uranium was within $0.50 of hitting $100 a pound, and about $5 from the 10-year high of $104.89 reached on Jan. 22, 2024.

Trading Economics states that “recovery in broad risk sentiment was combined with the signs of strong longer-term demand in nuclear power.”

According to Moomoo Technologies, “As of May 2026, the global uranium market is at a critical juncture transitioning from ‘cyclical fluctuations’ to ‘structural shortages.’ After experiencing intense volatility earlier in 2026, uranium prices are now showing stabilized spot prices and robust long-term contract prices.”

Other points made by Moomoo’s in-depth analysis of the global uranium market’s fundamentals and price trends:

- Currently, long-term contract prices have climbed to $90/lb, hitting their highest level since 2008. The fact that long-term contract prices are higher than spot prices (at a premium) indicates that utility companies (power plants) are far more concerned about future supply security than short-term price fluctuations.

- Industry analysts generally believe that to incentivize sufficient new mine development to meet the projected gap post-2030, uranium prices need to remain in the $125 – $150/lb range over the long term.

- As the world’s largest producer, Kazatoprom’s 2026 production target has been reduced by approximately **10%. This reduction is mainly due to shortages of sulfuric acid (a key consumable for lithium/uranium extraction), geopolitical transportation risks, and delays in the progress of new mine construction.

- The restart progress of Cameco’s flagship McArthur River project is slower than expected. Although Cameco reported impressive Q1 2026 earnings (with significant net profit growth), its inventory costs have risen to around $50/lb, reflecting an overall upward shift in the industry’s cost base.

- Driven by policy subsidies (such as a $2.7 billion grant from the Department of Energy), domestic in-situ recovery (ISR) projects in the U.S. (e.g., URC, EnCore) are accelerating their restarts. However, with development cycles lasting 7-10 years, these efforts will struggle to fill the global supply gap in the short term.

- Tech giants such as Meta, Microsoft, Amazon emerged as new forces in uranium demand in 2026. To provide 24/7 uninterrupted zero-carbon electricity to large AI data centers, these companies began directly securing hydrogen or nuclear agreements (such as Microsoft’s deal model with Constellation), breaking the previous pattern where purchases were solely made by power plants.

- The World Nuclear Association (WNA) forecasts that global uranium demand will reach 87,000 metric tons by 2030, marking a 28% increase from 2024.

- Utility company inventories are at multi-year lows, with insufficient long-term contract coverage.

- The US full ban on Russian enriched uranium (effective 2028) is forcing supply chains to shift westward.

- Inflation and environmental requirements have significantly driven up incentive prices.

- In summary, 2026 will be the year when the uranium market transitions from ‘speculative anticipation’ to ‘substantial delivery pressures.’ In the short term, the spot market may fluctuate with macro sentiment, but the continuous rise in long-term contract prices highlights the fundamental supply-demand imbalance within the industry.

Conclusion

Faith Birol, secretary general of the International Energy Agency, says the war in Iran has created the largest energy security threat the world has ever faced, and that “There will be a significant boost to renewables and nuclear power and a further shift towards a more electrified future.”

Over the past four years, nuclear power has experienced something of a renaissance, with increased demand for nuclear and higher uranium prices. Some mothballed projects were restarted, such as Cameco’s McArthur River mine in Saskatchewan.

However, demand for nuclear power, driven in large part by the “Magnificent Seven” tech companies, who seek to develop small modular reactors for their power-hungry data centers, and are planning to restart mothballed US conventional nuclear plants, is outpacing uranium supply.

China is set to become the dominant nuclear power producer. Based on existing and planned projects, its total capacity could reach 186 gigawatts compared to the US’s 118 GW and France’s 75,590 megawatts.

Current global uranium usage is about 180 million pounds a year. But mines only produce 130 million pounds, leaving a 50-million-pound shortage.

The uranium market fell into deficit in 2025 and the same is expected in 2026, with uranium supply down and reactor demand up.

The World Nuclear Association projects uranium demand will jump 28% by 2030.

Even the most conservative projection puts 2040 demand at 278 million pounds — almost 100 million pounds more than current consumption.

The West clearly needs to build more uranium mines to prevent shortages of the nuclear fuel as nuclear demand skyrockets due to population pressures, increased electrification as the world decarbonizes, and low-carbon government mandates on power plants.

Nuclear is the second-largest source of low-carbon electricity production after hydropower.

Nuclear is competing with renewables but even with increased battery storage capacity, and reduced costs, solar and wind can’t hold a candle to nuclear in terms of delivering 24/7/365 baseload power.

Almost all reports on future energy supply suggest an expanded role for nuclear power is required.

Richard (Rick) Mills

aheadoftheherd.com

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}