Can, will the Federal Reserve lower rates? – Richard Mills

2026.06.24

New Federal Reserve Chair Kevin Warsh views inflation primarily as a monetary phenomenon, adhering to the Milton Friedman dictum that persistent price rises are a choice made by the central bank.

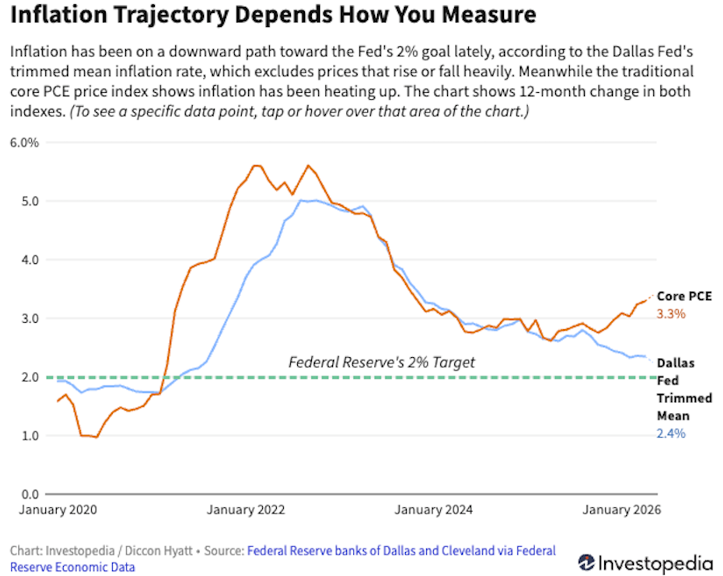

Warsh prefers to focus on “trimmed-mean” inflation metrics rather than the broader Consumer Price Index (CPI) or Personal Consumption Expenditures (PCE). He argues that trimmed averages better filter out one-time price shocks—such as those caused by geopolitical events or tariffs—to reveal the underlying inflation trend.

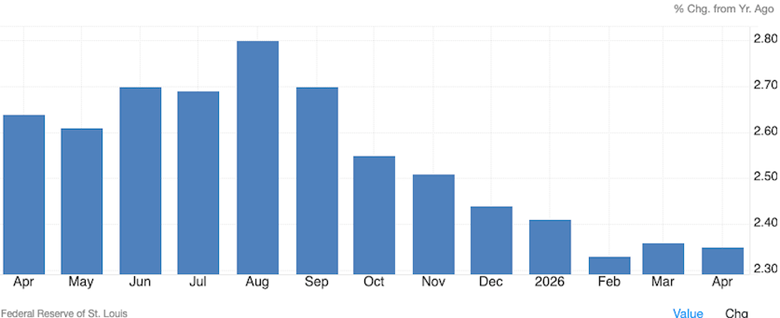

The annual Trimmed-Mean CPI for the United States increased to 2.9% in May 2026, up from 2.8% in April. Meanwhile, the Trimmed Mean PCE (Personal Consumption Expenditures) inflation rate—the Federal Reserve’s preferred trimmed measure—stood at 2.35% on an annual basis.

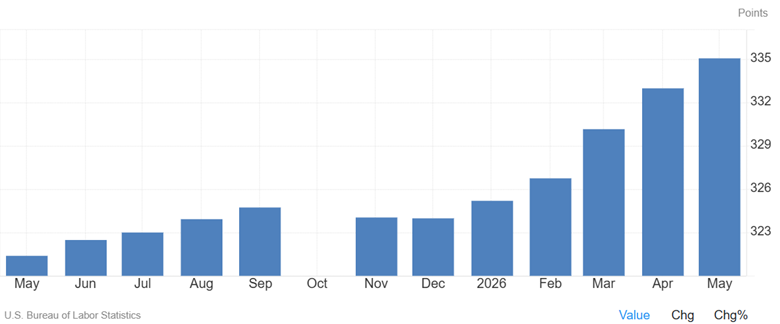

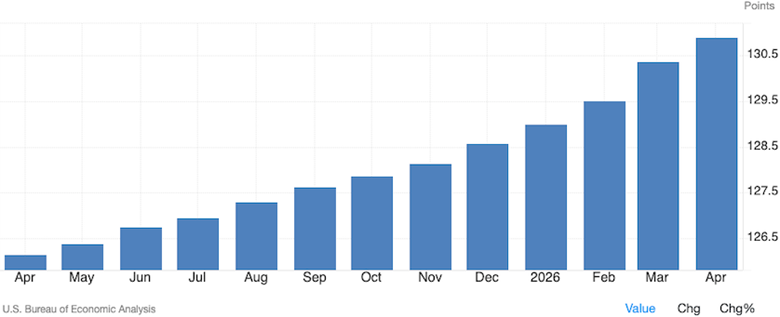

What’s clear is that inflation measures are sending different signals. The first chart below is the PCE Price Index. Remember this is the Fed’s preferred inflation measure.

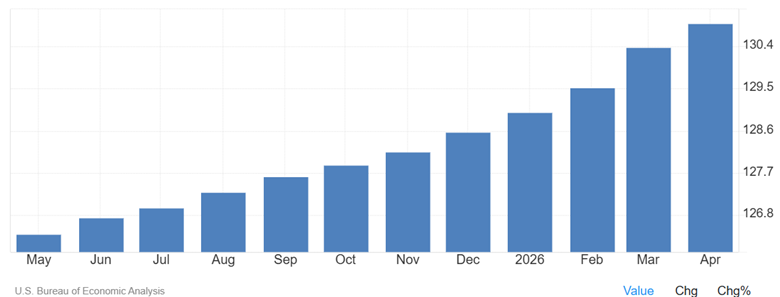

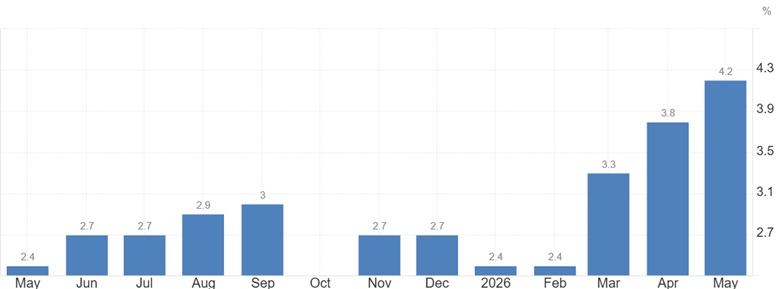

The Trimmed Mean PCE Inflation Rate in the graph below is practically the inverse of the PCE Price Index.

Source: Trading Economics

According to Investopedia, Warsh isn’t alone on the Federal Open Market Committee in his interest in using trimmed means as an inflation benchmark. As recently as January, Fed Governor Michelle Bowman pointed to trimmed-mean inflation indexes as evidence that inflation was cooling.

Warsh believes restoring the Fed’s credibility regarding price stability is paramount. He favors tightening monetary policy when necessary to ensure that temporary price shocks do not become embedded in long-term inflation expectations.

Say’s Law and the Quantity Theory of Money

Let’s dive into Warsh’s beliefs a bit more, they start with what inflation really is and what causes it.

Commodities are ultimately paid for not by money, but by other commodities. Money is merely the commonly used medium of exchange; it plays only an intermediary role. What the seller wants ultimately to receive in exchange for the commodities sold is other commodities.

This concept, famously articulated in classical economics, highlights the idea of a reciprocal exchange of goods. Essentially, every transaction is a form of barter, but with money acting as a convenient tool to split the transaction and overcome the limitations of a direct “double coincidence of wants.”

You exchange what you produce (your commodity or service) for money simply so you can exchange that money for what someone else produces. Ultimately, you are trading your labor or goods for their labor or goods.

Money is often described in this context as a “neutral veil” or a lubricant. It doesn’t create wealth on its own; it merely facilitates the exchange of real wealth (commodities) between individuals.

This forms the foundation of Say’s Law of Markets, which states that aggregate supply creates its own aggregate demand. Because people produce goods to trade them for other goods, the very act of production generates the purchasing power to consume elsewhere in the economy.

If the classical view is true—that commodities are ultimately paid for by other commodities and money is just an intermediary—then inflation is fundamentally caused by an oversupply of money relative to the production of actual goods.

When the classical concept holds true, inflation is not a sign that “goods” have magically become more valuable. Instead, it means the medium of exchange (money) has lost value.

This classical explanation of inflation relies on the Quantity Theory of Money, which explains the phenomenon through three primary concepts:

Money is Subject to Supply and Demand

Just like any commodity, the value of money is dictated by its scarcity. If a farmer brings a normal harvest of wheat to the market, but the central bank has suddenly doubled the amount of money in circulation, the relative value of wheat to money changes. Because there is too much money chasing too few goods, it now takes more units of that currency to buy the exact same bushel of wheat. The wheat didn’t change; the money became less scarce and therefore less valuable.

The Equation of Exchange

Classical economists and modern monetarists map this out using the famous Equation of Exchange:

M times V = P times Y

- M = Money Supply

- V = Velocity of money (how fast cash changes hands)

- P = Price Level (Inflation)

- Y = Real Economic Output (the actual commodities produced)

In the classical view, Y (real goods) is driven by technology and labor, and V (spending habits) stays relatively stable. Therefore, if the government increases M (money supply) faster than the economy can grow Y (goods), the only variable left that can rise to balance the equation is P (prices).

The “Veil of Money” Distortion

If commodities pay for commodities, an increase in paper currency does not create new real wealth. It merely alters the digital or paper accounting units used to measure that wealth.

Here is one of the clearest and most accurate explanations of demand-pull inflationand the monetary theory of inflation. Imagine the economy as a giant room of barter where people swap shoes for coats. If you give everyone a magical printer that copies the ticket vouchers used to claim the shoes, you haven’t actually created more shoes. You have only created a situation where it takes more ticket vouchers to claim a single pair of shoes.

As the economist Milton Friedman famously summarized, “Inflation is always and everywhere a monetary phenomenon.” It is an artificial expansion of the intermediary medium, money, causing the nominal price of real commodities to skyrocket.

The Difference Between a Supply Shock and Monetary Inflation

But an increase in the money supply does not cause isolated price spikes like the ones most recently in oil.

To understand why, it helps to separate a change in “relative prices” from true “monetary inflation”.

When a specific commodity like oil spikes due to geopolitical conflict—such as the recent naval bottlenecks blocking the Strait of Hormuz or the disruption of global reserves—this is a microeconomic supply shock, not a monetary phenomenon.

If the supply of oil drops dramatically but the money supply stays exactly the same, the price of oil will still shoot up. Oil has genuinely become scarcer and more valuable relative to everything else.

If the government prints double the amount of money but the physical supply of oil and all other goods remains identical, the price of oil will double. However, the price of milk, shoes, and rent will also double. The purchasing power of the dollar is what changed, not the scarcity of the items.

An oil spike feels like general inflation because oil is an input for almost everything else. When oil becomes expensive, shipping a plastic toy or running a factory becomes expensive. This causes a temporary bump in the Consumer Price Index (CPI). Because the use of oil is so heavily spread throughout our economy other prices rise.

However, if the central bank does not increase the money supply to match this oil spike, a fascinating shift occurs in the rest of the economy:

The Core Synthesis

Friedman’s maxim holds true for sustained, generalized price increases. A geopolitical crisis can make oil expensive overnight. But it only translates into long-term, economy-wide inflation if central banks panic and increase the money supply to help citizens pay for that expensive oil, effectively subsidizing the higher cost with printed currency.

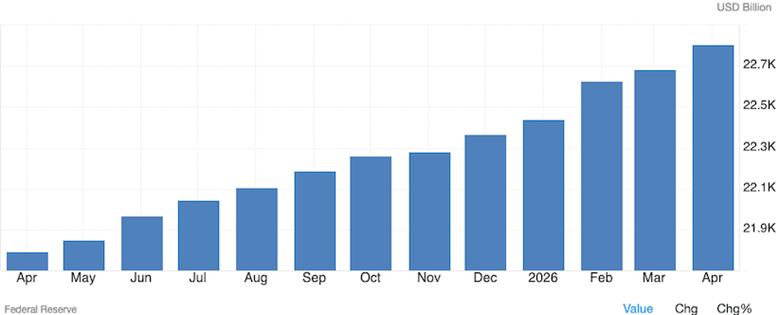

The US M2 money supply expanded to approximately $22.8 trillion by May 2026. This year-over-year (YoY) growth rate of roughly 4.7% to 4.8% is closely aligned with 2025 money supply increases, which also hovered in the low-to-mid single digits, signaling continued, gradual liquidity normalization.

When inflation spikes due to a supply-side shock—like higher oil prices and supply chain disruptions from the closure of the Strait of Hormuz—the traditional economic consensus is that central banks should maintain or even raise interest rates.

Central banks can absolutely lower interest rates after the strait reopens and oil prices decline. However, the decision to do so isn’t automatic; it depends heavily on how the initial supply shock impacts the rest of the economy.

Why Central Banks React (or Don’t React)

During an oil price spike, central banks face a stagflationary dilemma:

Because monetary policy operates with a lag of 12 to 18 months, raising rates to stop a short-term oil spike often doesn’t cool inflation in time. Instead of overreacting, Central Banks will typically hold rates steady, allowing the energy spike to pass through the system while focusing on underlying trends.

If the oil shock is severe, prolonged, or threatens to permanently embed higher inflation into the economy, central banks may raise rates to anchor public inflation expectations and avoid a wage-price spiral.

The Risks of Lowering Rates

Central banks cannot always automatically, quickly, cut rates when oil falls. They must remain cautious of two main risks:

Even if the strait reopens, supply chains, shipping lanes, and insurance rates may take months to normalize. Lowering interest rates too quickly into a recovering, yet still fragile, supply environment could re-stoke demand and trigger secondary inflation.

If the energy shock was prolonged enough that it forced businesses to permanently raise the prices of their end products (core inflation), cutting rates could lock those high prices into the economy, fueling persistent stagflation.

Warsh: More dove than hawk

Back to interest rates, an analyst quoted by Kitco said following the June 17 meeting that beneath the hawkish rhetoric of the FOMC being “unambiguous and unanimous” in its declaration of price stability (keeping inflation under control) were several signals suggesting a less restrictive path.

One signal is what Warsh said about housing prices. During the press conference, the Fed chair acknowledged that monetary policy appeared “somewhat restrictive” in housing. Translation: mortgage rates are too high and Warsh is concerned about it.

Rebecca Ivaldi, market strategist at FCT Capital Partners and a former Lehman Brothers analyst, also pointed to Warsh’s skepticism toward traditional inflation measures. While the Kitco article omits Trimmed Mean PCE Inflation, it reports that Warsh “announced a task force to examine new data sources…”

According to Ivaldi, that effort suggests the Fed may ultimately conclude that underlying inflation pressures are less severe than headline data currently indicate. She contends that once temporary energy-related distortions are removed, inflation is already much closer to the Fed’s target than widely believed.

The market is wrong

But this isn’t what the market is saying. Rates are priced 50 basis points higher in the US a year from now, while the Eurozone and UK are seen not far behind.

Fortune ran an article on Monday titled, ‘The Fed is fed up with inflation and will bring down the hammer with a series of rate hikes this year, reversing earlier cuts — BofA says’

While the mood is currently hawkish, an ING economist states the Federal Reserve could end up easing policy next year.

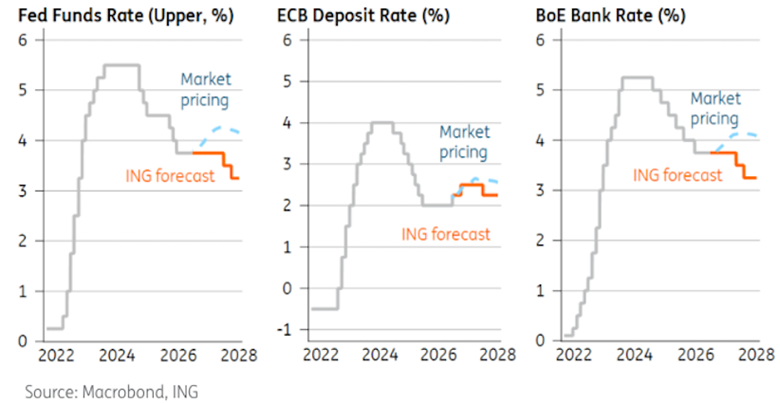

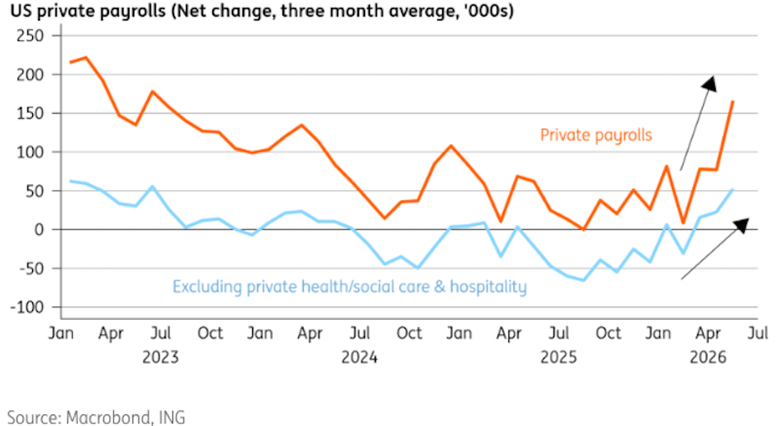

In a column, James Smith publishes three graphs from the Fed, the ECB and the Bank of England that show markets aren’t looking for rates to come down before 2028.

Again, the doomsday predictions are all about higher inflation. The case for rate hikes is based on a jobs market rebound despite lower immigration, and inflation at 4% and above the 2% target for five years.

Smith punches holes in both those arguments, stating that The jobs market recovery looks less impressive when you exclude private health/social care and hospitality. Those sectors account for only a quarter of jobs, but two thirds of jobs growth so far this year. Yes, hiring has improved elsewhere, but not nearly as rapidly as the headline figures imply. And crucially, there’s very little sign that this improvement is feeding into broader wage pressure.

That’s one reason why inflation fears should start to recede as the year goes on. Another is housing. Kevin Warsh himself acknowledged this week that policy still looks restrictive when you look at what’s happening there. And as James Knightley argues in his excellent piece today, rents are barely rising – something that should increasingly pull core CPI lower given housing’s huge weight in the index.

Add lower fuel prices, a reversal of recent air fare spikes and the fading impact of tariffs and the case for rate hikes looks much less compelling.

Which brings us back to markets. Right now, investors think rates are heading – and staying – higher. We suspect that by this time next year, central banks will be quietly preparing to explain why they’re going lower.

Another commentator found reports last Wednesday of the Fed being split on whether to raise interest rates puzzling, given that inflation conditions have changed since Iran was attacked in early March.

In a column titled ‘Why the Fed many need to stay patient’, Brian Levitt, chief global market strategist with Invesco, wrote:

Back in March, following the outbreak of the war with Iran, the inflation story was obvious. Oil prices surged. The 3‑year Treasury inflation breakeven pushed toward a 3% peak on March 18. The 5‑year breakeven climbed to 2.74% on the same date… the direction was clear. Inflation expectations were rising, and the Fed had reason to sound vigilant…

But that was March. Today’s environment is fundamentally different. Oil prices have dropped dramatically. Inflation break evens have followed. The 1‑year breakeven is now below 2%, a level that hardly suggests “overheating.” If anything, it may be the opposite. Inflation pressures have been fading, not accelerating.

So why exactly would the Fed be raising rates? It’s not as if the economy is running hot. Job growth has been relatively soft, despite the recent three‑month stretch of better‑than‑expected gains. Wage growth has been moderating. That’s why last Thursday’s Fed‑induced market selloff and the flattening of the yield curve left me scratching my head. The market seemed to react to a Fed that’s still fighting the war‑driven inflation scare of early spring rather than the reality of mid‑June. The stance feels backward‑looking, as if policymakers were anchored to the moment oil spiked rather than when it dropped dramatically…

In my view, the Fed remains on hold, and the next move (whenever it comes) may more likely be an easing than a hike. The current shape of the yield curve suggests policy may be restrictive. If the Fed were to tighten into this backdrop, it could risk contributing to a downturn it’s trying to avoid.

The upshot is that the cycle has continued. Peaks in oil, interest rates, and inflation expectations have often coincided with turning points that can support broader markets, not undermine them. Unless the data shifts meaningfully — and right now it has still shifted in the opposite direction of what a rate hike would require — the Fed’s most prudent course to me is patience.

Conclusion

Let’s be clear. Kevin Warsh’s first Fed meeting was less about the result — keeping the pause on rate hikes or cuts — than reshaping the Fed into a leaner organization that is less about the markets front-running the Fed, than the Fed digesting market data and making decisions tasked for it by Congress.

One of those decisions is interest rates. Which direction will the Fed go from here? While the market is hawkish, expecting at least one hike by year-end, I’m thinking the opposite. Warsh may hold for a little longer but I’m betting on a rate cut in late 2026 or possibly into 2027.

Much depends on whether the Iran war comes to end. Continued price increase predictions are tied to the price of oil. If the ceasefire between Iran and the US holds, and the Strait of Hormuz opens up, supposedly, for good, a large segment of inflation will be heading down — along with all the other commodities being held hostage by the war, including plastics, fertilizer, LNG, urea, aluminum, sulfuric acid, etc.

Warsh will have further justification to lower rates because of the new way the Fed will measure price increases. The Trimmed Mean PCE is falling, not rising. If they use this metric, it will hard for anyone to argue that inflation is an issue stopping rates from dropping.

The dot-plot will be gone, along with markets front-running the Fed based on a bunch of predictions that never come true. Unlike the self-important pontificating jawboning Powell and his predecessors, Fed Chair Warsh will simply go to the podium, announce the FOMC’s decision, then leave. No more tea leaves for the media and markets to read.

I agree with all that. At the end of the day, people need to understand that inflation is a symptom of excessive money-printing disease.

As the economist Milton Friedman famously summarized, “Inflation is always and everywhere a monetary phenomenon.” It is an artificial expansion of the intermediary medium, causing the nominal price of real commodities to skyrocket.

But an increase in the money supply does not cause isolated price spikes like the ones seen in oil.

To understand why, it helps to separate a change in “relative prices” from true “monetary inflation”.

When a specific commodity like oil spikes due to geopolitical conflict —such as the recent naval bottlenecks blocking the Strait of Hormuz or the disruption of global reserves — this is a microeconomic supply shock, not a monetary phenomenon.

Friedman’s maxim holds true for sustained, generalized price increases. A geopolitical crisis can make oil expensive overnight. But it only translates into long-term, economy-wide inflation if central banks panic and increase the money supply to help citizens pay for that expensive oil, effectively subsidizing the higher cost with printed currency.

When oil price spikes rippled through the economy, due to a supply-side shock, like higher oil prices and supply chain disruptions from the closure of the Strait of Hormuz, the wide spread consensus is that central banks should maintain or even raise interest rates.

We’re Ahead of the Herd and we are contrarians on rate raises. Warsh has signaled his intentions.

Richard (Rick) Mills

aheadoftheherd.com

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.

{kind=link}