One man, one missile – Richard Mills

2026.04.18

Before the war in Iran, the biggest risk to maritime shipping in the Persian Guld was the Houthis in Yemen. The Houthis are an Iran-aligned rebel group that attacked, and continue to attack, though on a much lesser scale, freighters in the Red Sea to pressure Israel to stop its military campaign in Gaza.

After the October 2023 Gaza war began, the Houthis declared any Israel-linked, or US/UK-linked ship in the Bab-el-Mandeb Strait a target in support of Palestinians. (AI Overview).

According to the Royal United Services Institute, the Houthis use a variety of weaponry, including anti-ship cruise missiles, anti-ship ballistic missiles, one-way attack drones, uncrewed surface vessels, and fast boat attacks.

Fast boat attacks are a low-tech way to sink a commercial vessel. Armed speedboats use small arms and rocket-propelled grenades to directly attack ships, often in conjunction with drones.

It takes a surprisingly small group to carry out these attacks.

According to Naval News, Houthi rebels attacked the Greek-operated bulk carrier Magic Seas in the Red Sea using a coordinated multi-asset assault that included eight high-speed boats, unmanned surface vessels (USVs), and rocket-propelled grenades (RPGs).

In 2024, reports indicated the Houthis began employing shoulder-launched RPGs in attacks against commercial shipping vessels in the Red Sea, often using speed boats for close-range assaults. (Wikipedia).

One sharp-shooting militant firing a shoulder-launched RPG could do severe damage to a vessel, especially at close range.

One man, one missile

A video describes in terrifying detail how these attacks are carried out:

The assaults typically begin under the veil of early dawn or the cover of dusk—times when visibility is low and the crew least expects an ambush. Small, fast-moving boats—often indistinguishable from local fishing vessels at a distance—approach the target ship at high speed.

Manned by armed Houthi fighters, these boats circle the larger vessel like wolves stalking their prey. Within moments, they unleash a barrage of rocket-propelled grenades also called RPGs and small arms fire, aiming at the bridge, engines, and other critical control points.

While the ship is under attack from the sea, the threat escalates from above. Bomb-laden drones, controlled remotely from miles away, dive toward the ship in a series of one-way, kamikaze-style strikes. These unmanned aerial vehicles are loaded with explosives and guided with deadly precision toward key areas of the vessel. The resulting explosions echo across the sea—disabling communications, igniting fires, and in some cases, blowing holes below the waterline. Under such relentless assault, the crew often has no choice but to issue distress calls and abandon ship.

The point of this description is to demonstrate how easy it is to disable a commercial ship, and how vulnerable shipping is to “black swan” events, especially in the world’s choke points.

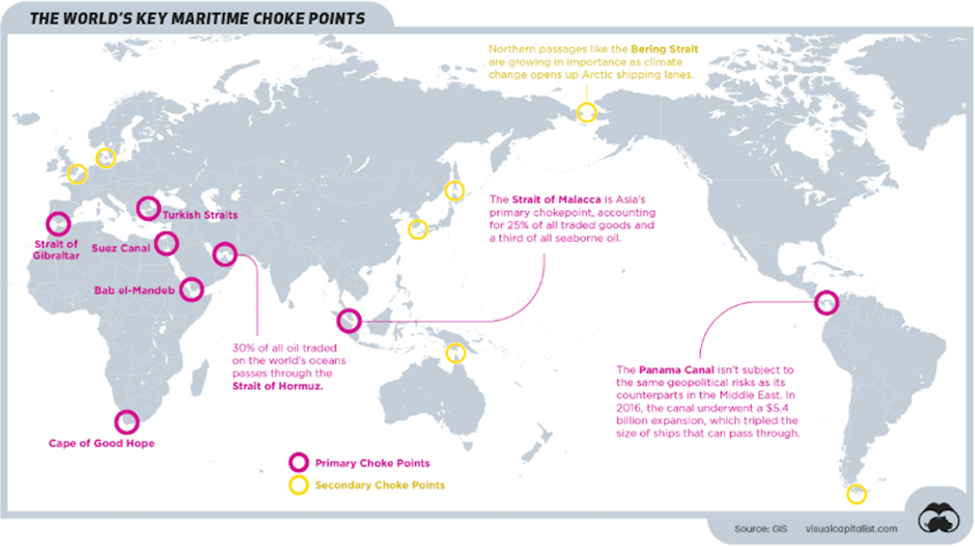

By now we are all familiar with the Strait of Hormuz and the Bab-el-Mandeb Strait. Visual Capitalist published an infographic showing these important trade routes and others, including the Suez Canal, the Panama Canal, the Strait of Malacca, the Strait of Gibraltar, the Turkish Straits, and the Cape of Good Hope. Not included on the map, but equally as important, are the Taiwan Strait and the Scarborough Shoal, both of which are vulnerable to blockades by China.

China is reportedly employing ships and a barrier to tighten control of the entrance to the Scarborough Shoal in the South China Sea amid roiling tension with the Philippines over the disputed feature.

The death of Just-In-Time (JIT)

Iran’s closure of the Strait of Hormuz has had a profound impact on the prices of oil, natural gas, and other key industrial commodities.

Before the war, 20 million barrels of oil flowed through the strait daily, or about a fifth of global oil consumption. Significant volumes of aluminum, LNG, distillates such as gasoline and jet fuel, fertilizer, and sulfuric acid used in metal refining, also normally transit the narrow waterway, but are trapped in the Persian Gulf due to the conflict. The closing of the Strait of Hormuz has also severely disrupted global helium supply, halting roughly 30%–33% of global supply originating from Qatar. This shortage, compounded by damage to Qatari facilities, is spiking prices—potentially up to $2,000/Mcf—and directly impacts crucial sectors, including semiconductor manufacturing (AI/chips), MRI cooling, and aerospace

The US blockade of Iranian ports has only tightened the noose on the transportation of goods by sea. More than a dozen US warships are involved, with at least 13 ships reported turned back in the initial days.

The war is changing the way we look at supply chains. Consider the introductory paragraph to a recent article by Supply Chain Brain:

The escalating conflict in Iran has already started to ripple through global supply chains, as disrupted shipping lanes, rising insurance costs and the effective closure of the Strait of Hormuz have forced carriers to suspend transits, reroute vessels and brace for higher transportation costs across global trade lanes.

That article goes on to make the following points:

- Roughly 11% of global freight passes through the Strait of Hormuz annually, as well as a third of all seaborne oil.

- Without the ability to send tankers through the Strait of Hormuz, Middle Eastern countries have cut more than two-thirds of their oil production.

- Crude oil is far more than simply an energy input, as it’s used in the manufacturing of tires, plastics, pharmaceuticals and a number of other synthetic materials. Any long-term oil shortages could lead to broad price increases for a variety of sectors.

- Some 44% of sulfur exports and 18% of ammonia come out of the Persian Gulf, both of which are key components used in semiconductor production.

- A third of the world’s fertilizer supply passes through the strait, too. That’s had the agricultural industry raising alarms about the availability of fertilizer to grow crops, right as planting season begins for many farmers in the US.

- Straining shipping costs even further has been an increase in attacks against commercial ships by Iran, making maritime risk insurance prohibitively expensive for carriers.

- Those additional premiums can add hundreds of thousands of dollars to the cost of a single voyage, sticking carriers with a bill that’s ultimately passed down the supply chain to cargo owners and consumers alike.

The blog Tarangya goes further, positing that the era of “Just-in-Time (JIT)” supply chains is over, replaced by “Just-in-Case”.

A just-in-time (JIT) supply chain is a lean management strategy where materials and products are received only as needed for production or customer demand, rather than being stockpiled. This approach minimizes inventory holding costs, reduces waste, and improves cash flow by aligning production with demand. Originating from the Toyota Production System, JIT relies on efficient, synchronized suppliers.

(AI Overview)

Tarangya’s first two paragraphs sum up the situation quite well:

The landscape of global trade in early 2026 looks nothing like the world we inhabited just two years ago. For decades, the logistics industry worshipped at the altar of efficiency. We optimized every second, shaved every cent, and prided ourselves on “Lean” operations. But as the dust begins to settle on the recent regional conflict, the heavy silence at the once-bustling docks tells a different story. The old playbook has been shredded.

For freight forwarders, exporters, and importers, the shift from Just-in-Time to Just-in-Case is not a choice; it is a survival mechanism. Supply chains after the Iran war are characterized by a profound sense of caution. We have moved from an era of “minimum viable stock” to an era of “maximum viable resilience.”

Stockpiling

In other words, stockpiling.

For example, there is evidence that China is stockpiling silver.

Kitco News reported that China’s silver imports reached an eight-year high in the first two months of 2026. The country brought in 790 tonnes of the precious metal, customs data showed, with February alone accounting for a year-on-year record of 470 tonnes.

“Disruption risk may prompt participants to secure their own stockpiles rather than share buffers globally,” analysts at Goldman Sachs said. “This shift from a pooled global system to isolated regional inventories would create an inefficient structure — transforming a smooth, integrated market into one prone to sharp, localized price swings.”

Aljazeera reports that major nations are releasing and managing strategic petroleum reserves following Strait of Hormuz disruptions, with Japan, South Korea, Germany, France, Spain, Australia and the UK all releasing reserves via the International Energy Agency. China is “heavily stockpiling,” holding an estimated 1.2 billion barrels — equivalent to about 109 days of seaborne import cover.

The US House Select Committee reported on March 31 that China has continued to buy and stockpile oil from sanctioned countries like Russia, Iran and Venezuela.

The IEA said on Thursday, April 16 that Europe is six weeks away from running out of jet fuel.

Why did JIT fail? Tarangya observes that the philosophy was built around a predictable world, with strategic waterways always open, bunker fuel prices stable, and black swan events happening once a decade, not once every quarter.

When war broke out in Iran, shipments that were timed to the hour were suddenly trapped behind naval blockades or diverted 4,000 miles around the Cape of Good Hope.

The “Lean” supply chain had no fat to live off of. Within weeks, assembly lines in Europe and North America ground to a halt not because they lacked vision, but because they lacked a two-week supply of $5 valves. This was the catalyst for the historic pivot toward Just-in-Time to Just-in-Case.

The new era of inventory management sees warehouses no longer as “cost centers” but as insurance policies. In 2024, inventory buffers were calculated in three to five days. The new buffer especially for critical electronics and medical equipment is 60-90 days. According to Tarangya, Forwarders are seeing a surge in demand for bonded warehouse in “Safe Zone” hubs like Oman, Singapore and the UAE, where goods can be staged close to their final destinations without being subject to the immediate volatility of a conflict zone.

The Council on Foreign Relations points out that For years, foreign policy experts argued that complex interdependence would make wars less likely because of the extensive financial damage they would inflict on economically linked states. The theory claimed that global supply chains are too delicate to risk large-scale warfare, especially near critical choke points in the global system.

However, that theory failed to consider leaders who take decidedly narrower views of their interests, decline to consult others, and embark on risky actions they are convinced will be quickly resolved. [Hmmm— Rick]

According to Morgan Stanley Capital International (MSCI), What makes supply-chain exposure particularly consequential is its cascading nature… each affected industry feeds inputs into hundreds of others, turning one shock into many.

Sulfur squeeze

A good example of that is sulfur.

Sulfur is used to make sulfuric acid, a critical input for copper and cobalt leaching, as well as nickel and lithium refining.

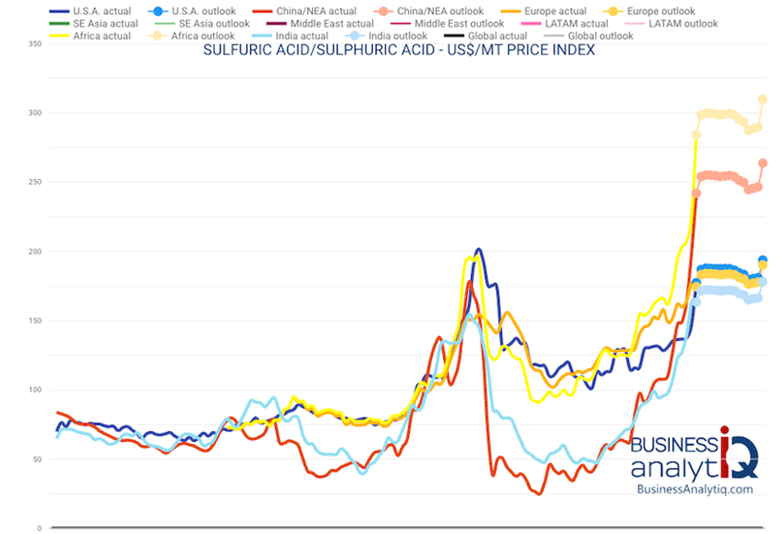

According to Argus Media, Roughly half of global seaborne sulphur trade transits the strait of Hormuz. With Middle Eastern refinery operations disrupted and shipping largely halted, global sulphur availability has tightened sharply.

As the war grinds on, there could be long-lasting effects on battery metals production.

Mining Technology notes that Because sulphur is also a by-product of oil and gas refining, disruption across the Middle East can affect both production and trade availability, creating a secondary supply shock for mining and metals processing.

Copper

Sulfuric acid is a core reagent in the heap leaching and solvent extraction–electrowinning (SX/EW) process used to produce copper from oxide ores and certain secondary sulfide ores. This hydrometallurgical method is essential for the economic recovery of low‑grade deposits and is widely employed across major copper‑producing regions worldwide.

Heap-leach operations supply roughly one-fifth of the world’s refined copper, an amount approximating 4 million tonnes per year. According to the US Geological Survey, global refined copper production last year was 29 million tonnes, so heap leaching using sulfuric acid represents almost 14% of the total.

Sulfuric acid is used in African countries to heap leach copper. When these countries run out of sulfur/ acid they will no longer be able to extract copper, causing a shortage.

The Central African Copperbelt (CACB) produces around 6 million tonnes per year of sulfuric acid, much of which is used in the DRC — Africa’s largest copper miner — for high-grade oxide leaching.

Africa is particularly exposed to the war in Iran. According to Argus Media, nearly all sulfur imported by southern African buyers last year originated in the Middle East.

Ivanhoe Mines (TSX:IVN) founder Robert Friedland recently warned that a prolonged closure of the Strait of Hormuz could hobble copper producers by driving up sulfur/ sulfuric acid prices and causing shortages.

Quoting from an IVN news release, Mining.com reported Friedland saying that “If the closure of the Strait of Hormuz continues, we are especially concerned about the availability of precursor materials necessary for the mining industry to continue operating,” noting that about half of the global seaborne sulfur supply is cut off.

Indeed, the Middle East accounts for about 40% of global sulfur exports. Making matters worse, China is about to slap a ban on sulfuric acid exports starting May 1.

Ivanhoe said on March 31 that realized prices for sulfuric acid have risen past $500 a tonne in recent weeks amid supply constraints.

The threat to refined copper supply due to the very real possibility of running out of sulfuric acid, feeds into the copper deficit narrative that I’ve been warning my readers about.

Sulfur chokepoint threatens critical minerals supply — Richard Mills

If sulfur and sulfuric acid fail to make it to the refineries, we are talking about 4 million tonnes/yr stripped from global copper supply, around 14% of a refined copper market of 29 million tonnes. That’s huge.

Silver

Silver will also be affected, since about 30% of global silver production is sourced as a byproduct of copper mining. If 14% less copper is being refined due to a shortage of sulfuric acid, it means less silver will be refined, too. Silver is entering its sixth year of deficits.

The silver shortage is real — Richard Mills

Fertilizer

The sulfur squeeze is also affecting phosphate fertilizer makers, which account for over half of the demand (54% in 2024) for the commodity.

Chemistry World notes that the Gulf exports large amounts of phosphate fertilizers, especially to Asian countries without much natural gas such as India, Pakistan and Bangladesh — natural gas is used to make fertilizer.

The publication also says that the Middle East is the largest supplier of sulfur to Morocco’s state-owned OCP, the world’s biggest phosphate producer; and that in March, China began restricting exports. Food The war in Ukraine doubled fertilizer prices in 2022 due to disrupted natural gas supplies and the Russian military blockading Ukraine’s ports that export agricultural products. Key fertilizers like urea saw record-setting spikes.

In the Iran war, what started as an energy shock is fast becoming a food crisis, with stranded cargoes and fertilizer shortages threatening global supply chains.

Food Navigator reports the Hormuz Strait disruption is impacting over 2,000 ships carrying food and energy inputs, with grains, oil, sugar, cocoa and coffee delays threatening food and beverage manufacturers.

It’s a little-known fact that grains such as wheat, maize and barley account for a large portion of bulk cargoes moving through the Strait of Hormuz. Edible oils such as sunflower oil and rapeseed oil are also important cargoes and prone to spoilage as they sit idle at sea.

Trapped agricultural imports like fertilizer put future harvests at risk.

Downstream oil products like packaging and petrochemical-based materials are also impacted. Shortages are poised to hit categories like beverage bottling, temperature-sensitive products, protein, and processed foods.

Food Navigator notes the largest misconception is that if your primary supplier is not in the Middle East, the strait’s closure won’t impact you.

“You are only as strong as your weakest link in your supply chain, and so your suppliers’ suppliers and your suppliers’ suppliers’ suppliers could be dependent on ingredients impacted,” warns Lisa Anderson, president of supply chain specialists LMA Consulting Group.

In practice, that means companies far removed from the region on paper may still be exposed through hidden dependencies deep in the supply chain. From fertilizers used to grow crops, to petrochemical resins that underpin food packaging, to specialist inputs sourced by lower-tier suppliers, disruption at a single chokepoint can cascade across an interconnected global system. The result is that even manufacturers with no direct ties to the Middle East may face higher costs, shortages or delays as those upstream vulnerabilities surface.

Global food prices are indeed creeping up.

According to the Food and Agriculture Organization, the FAO Food Price Index climbed to 128.5 points last month, indicating a 28.5% increase in food prices compared to the 2014-16 base period. While that’s far below the peak of 160.2 in March 2022, shortly after Russia’s invasion of Ukraine, it’s up 8% from March 2024 and roughly 35% from the 2019, i.e. pre-pandemic average. (Statista)

FAO Chief Economist Máximo Torero said so far, price rises have been modest due to ample cereal supplies, but if the conflict stretches beyond 40 days — which it did on April 10 — farmers will have to choose: farm the same with fewer inputs, plant less, or switch to less intensive fertilizer crops. Those choices will hit future yields and shape our food supply and commodity prices for the rest of this year and all of the next.”

Tomatoes are one of the hardest-hit grocery items. According to the US Bureau of Labor Statistics, tomato prices rose 15% in March, hitting an eight-year high. The main price driver is tariffs on Mexican tomatoes, but higher energy prices due to the Iran war and bad weather are also contributors, states CNBC.

Cascading inflation

A shortage of sulfur/ sulfuric acid and the knock-on effects on copper refining, silver, fertilizer and food shows how integrated inflation is into economies. Commodity shortages cause prices to rise, which filters down to users of those commodities. Manufacturers who buy input metals at higher costs typically pass those costs onto their customers.

Inflation is the reason the prices of many foods can ultimately be traced back to the war in Iran, and before that Russia’s invasion of Ukraine. Farmers pay more for fertilizer, forcing them to charge more for their produce. Grocery stores either absorb that higher cost or pass it onto their customers to maintain profit margins.

In the US, the Trump tariffs are pushing the prices of imported foods like tomatoes even higher. Bad weather, a frequent food inflation culprit, is also to blame in some cases. The skyrocketing price of chocolate, for example, is due to a severe shortage of cocoa caused by poor harvests in West Africa — the world’s #1 chocolate supplier — driven by droughts and heavy rain.

Beef is expensive primarily due to a severe supply shortage, with North American cattle herds at their lowest levels in decades. Again weather pays a huge part, drought stalks much of the mid and western US, pastures are no longer usable and hayfields, if not irrigated with water for other uses already in short supply, do not produce required volumes of winter hay.

The war is exposing supply chain vulnerabilities in some odd places. This week, it was reported that the City of Baltimore’s public water system cut fluoride levels in its drinking water nearly in half, in response to strains in the supply chain caused by the conflict.

The city’s fluoride supplier alerted public works officials that deliveries would be reduced from three per month to two. In response, the water system which serves 1.8 million customers, is lowering fluoride levels from 0.7 milligrams per liter, the recommended limit, to 0.4 mg/l.

Other US water systems are facing a similar problem due to a shortage of hydrofluorosilicic acid, the chemical used to fluoridate drinking water to prevent cavities and tooth decay.

When we start thinking about the geopolitical situation, supply chains and resource nationalism — the tendency for governments to seek control over their own natural resources and to prevent foreign companies from exploiting them — readers should open their minds up to what else is going to get expensive.

Take electricity, for example. The Iran war has driven up global energy costs particularly in Europe, where natural gas prices have surged over 70%. Here again there are knock-on effects. Power prices in Sweden are heavily influenced by prices in Germany due to the integrated European energy market and interconnecting cables. Projections indicate a potential 10% increase in electricity generation costs in some areas.

US wholesale prices experienced a 4% surge in March 2026, driven by an 8.5% rise in energy prices from February, marking the largest increase in over three years.

Rising natural gas prices are expected to increase heating and cooking costs, with higher energy costs expected to flow through to electricity bills. (AI Overview)

British drivers are also feeling the effects. The price of gasoline, or petrol in local parlance, averaged 158.2 pence per liter on April 13, an increase of more than 25p since the start of the war.

It’s even worse for diesel prices. UK diesel is now 191.5p/l, up nearly 49p since the beginning of March. According to BBC News, It means that the average cost filling a 55-litre family car with petrol has increased by £14 since the start of the Iran conflict, with diesel up by £27.

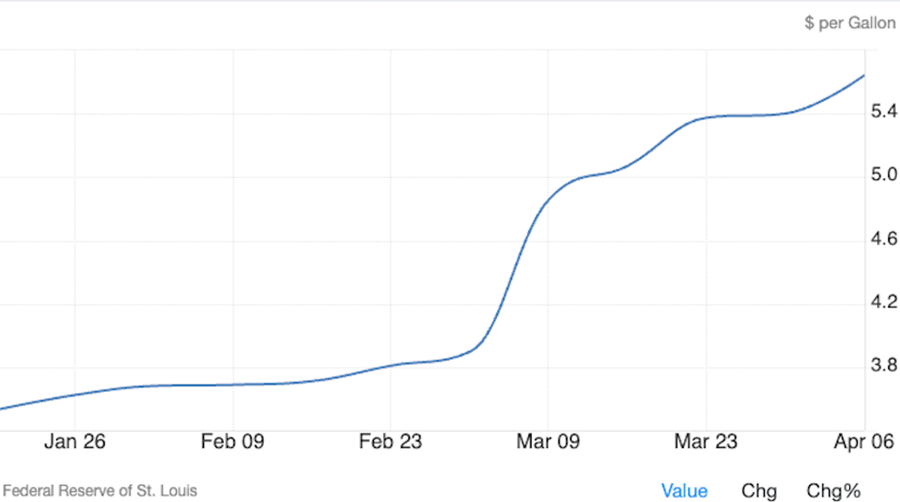

In the US, diesel is currently $5.64 a gallon, compared to $3.53/g in January — not far from the record-high $5.81 reached in June 2022.

Then you look at mortgages. Before the war, there was hope that interest rate cuts would lower the cost of mortgages. Sadly, for homeowners, this is unlikely to happen due to rising inflation.

In the UK, the average two-year fixed rate has jumped from 4.83% at the start of March to 5.89%.

In the US, Reuters reported on April 1 that the interest rate on the most popular 30-year fixed-rate mortgage rose 14 basis points to 6.57%.

Mortgage rates have climbed by 48 basis points since the United States and Israel launched war on Iran on February 28, threatening to make home purchases less affordable…

Mortgage rates are based on the 10-year US Treasury yield which, despite falling back recently due to hopes that the Strait of Hormuz would open and help ease inflation concerns, is still at 4.25%, as of this writing. Since Sept. 1, 2025, the rate has stayed below 4.25%, only poking above that level twice, on Jan. 20, and Feb. 2-4.

Less government wiggle room

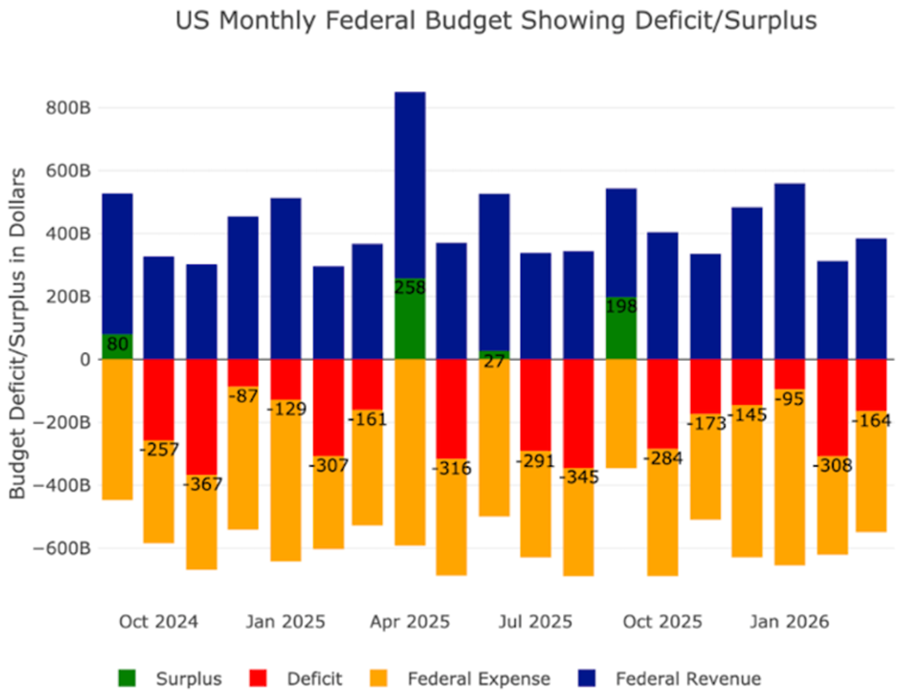

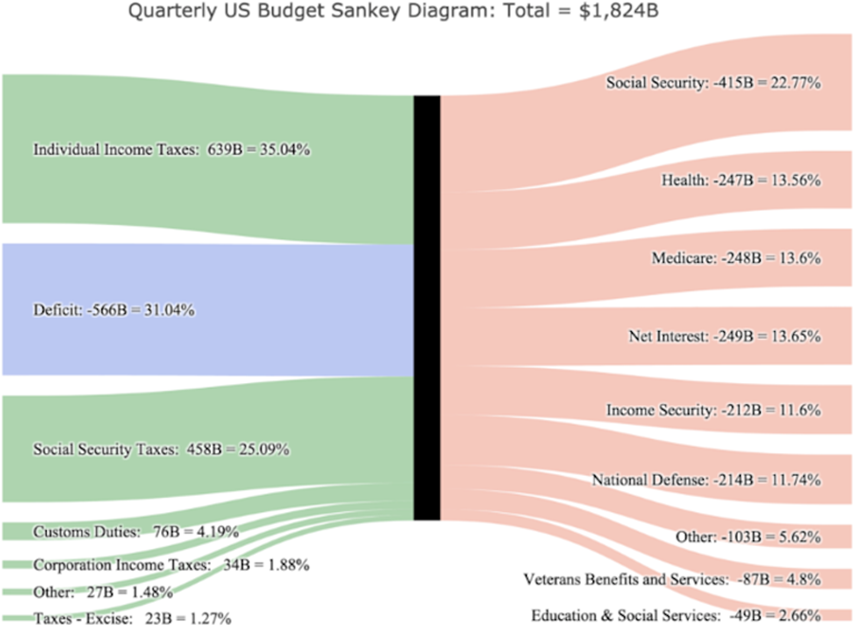

At AOTH, we have written extensively on the US national debt, which now exceeds $39 trillion. The most alarming thing about this figure is the amount required to service the debt, i.e., interest payments.

The debt is comprised of previous and current deficits.

The chart below courtesy of SchiffGold shows that the last three months all saw deficits, with five of the last six months showing a deficit of more than $100 billion.

The big concern with the chart below is how much Interest expense has moved up, making up 13.6% of all spending in Q1. This is now the second largest line item behind only Social Security. This is how debt spirals work. The deficit now makes up 31% of all spending, which means that the US borrows 1 in every 3 dollars it spends.

(This isn’t only a US issue. The accumulation of public debt has become a global problem. Fortune Magazine reported the IMF forecasts global public debt will hit 99% of world GDP by 2028, breaching the 100% threshold sooner than previously forecast. Under stress scenarios representing the 95th percentile of plausible outcomes, that figure could spike to 121% within three years.)

The US government is already paying over a trillion dollars per year on interest payment just to service the national debt..

But the American people can no longer depend on the national government to fund their most basic needs. Trump recently said it’s “not possible” for the US to pay for Medicaid, Medicare and day care because “we’re fighting wars.”

He said it should be up to the states to take care of these programs while the federal government focuses on military spending.

As reported by BBC News,

In his 2027 fiscal year budget request released in April 2026, President Donald Trump proposed a massive increase in military spending to $1.5 trillion. This proposal aims to boost defense funding by over 40% from the 2026 level of $901 billion, marking one of the largest military spending increases in U.S. history.

At the same time the Trump White House is cutting taxes, further reducing the government’s room for maneuver around the massive deficits and debt it’s racking up.

The IMF this week, per Bloomberg, warned Wednesday that the escalating scale of US debt issuance is undermining the premium Treasuries have commanded from investors, with implications for government securities across the globe.

In January, before the war, it was reported that foreign countries are retreating from US debt markets, with Denmark’s Treasury holdings at record lows, and China’s holdings falling to $682.6 billion in November, the lowest level since 2008. India has also been selling Treasuries, with holdings dropping to $190 billion as of the end of October. Yahoo Finance reports:

Taken together, these actions point to a fundamental reassessment of US credit risk among major foreign holders.

The scale and persistence of these reductions suggest more than routine portfolio rebalancing. Instead, they reflect growing concern over America’s fiscal sustainability and the risk of policy-driven deterioration in credit quality.

And then there’s this, seen on Bloomberg Television:

Former Treasury Secretary Henry Paulson suggested US authorities prepare a back-up plan in order to avert a potential future collapse in demand for Treasuries resulting from long-running concerns over the federal debt load — an event that he warned would have “vicious” effects.

Debt slaves

A recent New York Times article found that consumer spending is under strain. That spells trouble for the US economy because consumer spending comprises 70% of the economy.

First, the Times points out that “The enduring strength of consumer spending…has been the main reason that the United States has evaded a recession through successive drubbings over five years: roaring inflation, a rapid run-up in interest rates and a barrage of tariffs.”

The dirty little secret as to why consumer spending has been so resilient over the past few years has nothing to do with saving money or making smart investments. When Americans couldn’t afford something, they just put it on credit. As reported by Money Metals:

By the end of 2020, revolving debt, primarily reflecting credit card balances, had dropped below $1 trillion to $979 billion. Today, outstanding revolving debt stands at $1.33 trillion…

Meanwhile, the personal savings rate is at the lowest level since 2008.

Americans have run up a significant amount of debt in just a few years. They currently owe $5.12 trillion.

The Federal Reserve consumer debt figures include credit card debt, student loans, and auto loans, but do not factor in mortgage debt. When you include mortgages, U.S. households are buried under a record $18.8 trillion in debt.

US security umbrella gone

Let’s be honest. The US is wearing out its welcome in the Middle East, Europe and Canada. Trump’s threat to annex Greenland is surely a good reason why Denmark sold 30%, or $4 billion, of its Treasuries.

According to an AI Overview,

Danish pension fund AkademikerPension is selling all its U.S. Treasuries—approximately million—by February 2026, driven by concerns over weak U.S. public finances, rising debt, and low predictability of U.S. policy. The decision, prompted by rising credit risk, was accelerated by geopolitical tensions regarding Greenland, though it was not the sole factor.

Other countries follow suit. Next in line could be Gulf Cooperation Council nations, all six of which — Saudi Arabia, Qatar, the UAE, Kuwait, Bahrain and Oman — are US allies.

A March 26 brief from the Globe and Mail notes how badly these countries, which host US military personnel and infrastructure, that also makes them targets, have been pummeled during the Iran war:

Whatever the outcome of the Iran war, one question is already unavoidable for the Gulf’s energy-rich economies: Is the U.S. security umbrella still worth the cost? A Reuters dispatch to The Globe reports that since the United States and Israel began strikes on Iran on Feb. 28, Gulf neighbours have suffered the most from missiles and drones that have damaged energy infrastructure and exposed the limits of the U.S. security umbrella. At stake is a possible re-evaluation of the financial, trade and military relationships at the core of their dollar-based economies — and of the hundreds of billions in dollar reserves supporting them.

For decades, Washington and the Gulf states had an implicit agreement: U.S. protection in exchange for access to Gulf energy, oil priced in dollars, and the investment of petrodollars in U.S. arms and assets. The arrangement underpins the dollar’s status as the world’s reserve currency and has been central to U.S.-Saudi relations ever since. UK Commercial Secretary to the Treasury Jim O’Neill says, “If this war has shown anything so far, it is that allying yourself with the U.S. no longer guarantees security.”

Adding to the demise of the US petrodollar is the rise of so-called “commodity currencies”. A recent Reuters piece describes how The war in the Middle East is the latest reminder of how commodities are reshaping the geopolitical landscape, leaving currencies from Norway, Canada, Australia, and New Zealand well placed to outperform larger rivals.

These commodity currencies – so called due to their close correlation to the fortunes of their countries’ main export commodities – include two of the best performers among 10 developed market economies: the Norwegian crown and Australian, or Aussie, dollar.

The story goes on to say that both are up over 7% versus the US dollar this year, and that some investors see the potential for even bigger gains as an increasingly fragmented global order accelerated by the United States’ go-it-alone shift and the rise of China drives nations to prioritise energy security and secure commodities essential to the AI-buildout and green transition.

Conclusion

The war in Iran has exposed the fragility of the world’s supply chains. The closure of the Strait of Hormuz has effects on so many commodities beyond oil and gas; as this article has shown, practically everything is getting more expensive.

Take metals. In the West we don’t produce enough critical minerals like manganese, graphite, antimony, aluminum and copper. We don’t make enough steel, either, and we’ve hit peak silver and peak gold.

With supply chains shifting from Just-in-Time to Just-in-Case, the only option available to suppliers, to ensure a steady flow of products, is to stockpile raw-material inputs. We’re seeing this already with the US stockpiling copper, China stockpiling silver and oil, and placing export restrictions on critical minerals it controls the refining of.

Remember, mining input costs such as diesel are also going up, increasing costs per tonne or ounce, compressing margins and leading to production challenges.

It’s all coming to a head; we live in a very inflationary environment. And let’s remember: Just because a war stops or a Strait opens, just because ‘one man with a missile’ disappears for a short while, doesn’t mean that people aren’t going to start, or won’t continue hoarding key raw materials needed for manufacturing, defense, pharmaceuticals, the food supply, transportation, energy production, AI and the like.

In an unstable world, we are heading back to the era of warehousing and stockpiling to keep the shelves full. Especially given that one combatant shouldering an RPG can sink a ship in one of the world’s dozen choke points, throwing the JIT supply chains that rely on perpetually open shipping lanes into massive chaos.

Companies are starting to realize that there is no security of supply in a two-three-day inventory buffer. As the Tarangya blog puts it, “The old playbook has been shredded.”

Making the shift from Just-in-Time to Just-in-Case will be costly, too. Regional container shipping hubs would need to be set up or expanded, more ships built, more trains, more trucks, etc. Possibly new railways, roads and ports too, to serve much more localized supply chains.

Not to mention the people needed to crew the ships, operate the trains and drive the trucks. The Trump administration’s crackdown on undocumented migrants has made sure that the workforce that picked the fruits, vegetables, nuts and berries is either detained or too scared to show up on farms. Ditto for construction sites and warehouses.

We also need to acknowledge that we’ve given a lot away to foreign countries — the most obvious example being mining and mineral processing. A movement to mine and process locally is beginning in the United States and Canada but it will arguably take years to make a difference.

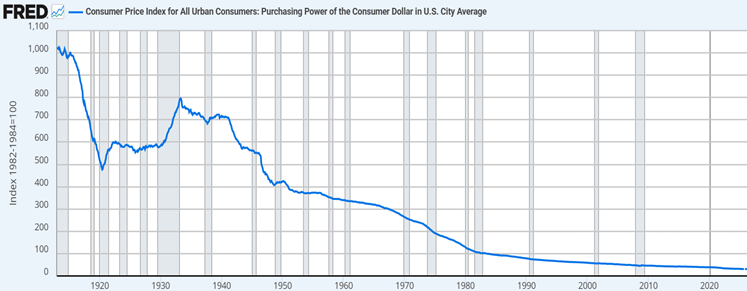

Casey Research founder Doug Casey believes we often put the cart before the horse when thinking about inflation. The renowned investor, author, and speaker states,

“Inflation” occurs when the creation of currency outruns the creation of real wealth it can bid for… It isn’t caused by price increases; rather, it causes price increases.

Inflation is not caused by the butcher, the baker, or the auto maker, although they usually get blamed. Inflation is the work of government alone since government alone controls the creation of currency.”

February 1970

Milk: $1.32 per gallon

Eggs: 60¢ per dozen

Bread: 70¢

Bacon: 85¢ – 95¢ per pound

Gasoline: 36¢ a gallon

February 2021

Milk: $3.36 per gallon

Eggs: $1.59 per dozen

Bread: $1.32

Bacon: $5.77 per pound

Gasoline: $2.55 a gallon

March 2026

Milk: $4.06 per gallon

Eggs: $2.35 per dozen

Bread: $1.85

Bacon: $6.90 per pound

Gasoline: $3.00 a gallon

We can all agree there has been a large increase in the prices of our breakfast groceries, over the past 5 plus decades. This is inflation.

In 1970 the United States was still on the gold standard. An American with an ounce of gold, say an American Eagle coin, could redeem his gold for US$35. How much could he buy and how many people could he feed? At 1970 prices, that $35 could make a lot of pancakes and French toast, with plenty of bacon rashers for everyone and still a few eggs left to cook and milk for coffee and tea.

Now take that same $35 and try to make an identical breakfast feast in 2021. The groceries do not stretch nearly as far, we estimate $35 worth of milk, eggs, bread, and bacon would feed about 40% less people than in 1970. Everything is just so much more expensive.

Of course, what has gone up even more, is gold. Selling an ounce of gold in 2021 would have given you about $1,750 — a 50X increase over the $35/oz gold in 1970. Obviously $1,750 buys a hell of a lot more breakfast groceries than $35 — you could probably feed an entire football team, including coaches and trainers, with everybody coming up for seconds.

The point is a grocery shopper using gold as a currency rather than dollars in 2021 would have seen a 50-fold increase in their purchasing power.

The shopper using dollars by contrast lost about 40% of their purchasing power because the prices of their grocery items have at least doubled or in the case of bacon quintupled. The 35 dollars can feed 40% less people than in 1970. If they had kept that same ounce of gold and cashed it in 51 years later, they could feed 50 times as many people.

You can do the math between 1970 and 2026, but it does not take a whole lot of figuring to know which has been the better store of value, dollars, or gold? Obviously, it is gold – the only true safe haven that protects the holder against rampant inflation caused by excessive money-printing.

Richard (Rick) Mills

aheadoftheherd.com

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.