Are climbing bond yields a signal to the Fed to raise interest rates? – Richard Mills

2026.05.21

Global bond yields are reaching frightening levels due to the continued war in Iran and the effective closure of the Strait of Hormuz. Continued high oil prices and the threat of reverberating inflation are causing investors to demand higher yields on government bonds.

Here we dissect the trend, but first, a primer on bond yields.

The global bond market is significantly larger than the global stock market, with a total value exceeding $140 trillion. The US bond market alone is valued at over $51 trillion, making it the largest in the world.

This is why investors, large and small, watch US Treasury yields closely to see what they are signaling for the economy going forward.

High long-term yields are a sign of rising inflation expectations. Investors require higher interest rates to tie up for their money for up to 30 years, as the risk of inflation is greater.

Lower yields generally indicate reduced interest rates for government debt and can signal weakening economic growth expectations or lower inflation expectations. During periods of quantitative easing, when the Fed lowers rates and buys up bonds and other securities to shore up a weakening financial system, Treasury yields fall and bond prices rise.

When yields fall, it means investors are willing to accept lower returns on their investments in Treasuries, often because they are seeking safe-haven assets (bonds) during periods of economic uncertainty.

Bond prices and yields have an inverse relationship. When yields go up prices drop, signaling a lower demand for Treasuries. If the Fed increases interest rates, yields generally rise.

US long bond highest since 2007

On Tuesday, May 19, the yield on the 30-year US Treasury bond rose to the highest level since 2007, at 5.19% — part of a global selloff of government bonds as investors grow increasingly worried about accelerating inflation. Bond markets across Europe and Asia also fell.

Yields on government bonds have surged globally in recent weeks as a jump in energy prices caused by the Iran war adds to inflation fears, pushing investors to bet central banks, including the Federal Reserve, will raise interest rates. Mounting government deficits also are prompting investors to demand greater compensation to own longer-maturity debt.

Traders now anticipate the Fed’s next move will be an interest rate increase. When the war began in late February they were predicting up to three cuts in 2026.

In preparation, US officials have already shifted debt issuance towards shorter-dated maturities.

“The market has swung to a clear hiking bias,” said Benjamin Schroeder, a senior rates strategist at ING Groep NV. That’s because investors are “worried about energy price pressures morphing into something more than just a short-lived inflationary episode.”

Bloomberg noted the 5% level for 30-year US yields has always been considered a “line in the sand” that would spark dip-buying. But there are few buyers for the long bond.

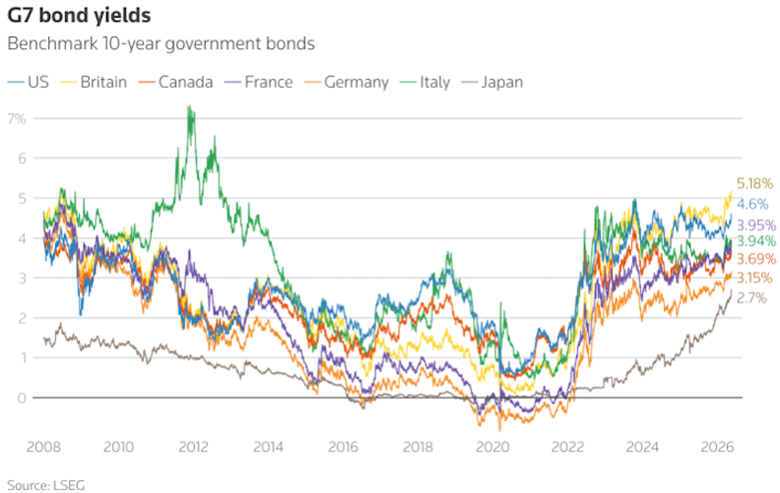

A similar dynamic is playing out globally, with yields on 30-year UK gilts approaching 6% and Germany’s long-term borrowing rate trading at a 2011 high.

In another demonstration of climbing bond yields, yields on 30-year Treasury Inflation Protected Securities (TIPS) on Monday hit their highest level since April 2025, rising about 40 basis points since the Iran war started, and contributing to most of the jump in the 30-year nominal yield.

CNBC titled an article, ‘Ominous bond trades point to much higher rates’:

More than three times the past month’s average daily volume traded in the long-term Treasury fund, the iShares 20+ Year Treasury Bond ETF (TLT) on Friday, with a heavy bias towards put contracts positioning for lower prices and higher yields. Of the 1.4 million contracts traded, almost 380,000 were puts exchanged at the ask or above, indicating they were likely purchased. By comparison, under 240,000 calls were bought.

The put trades would be a bet on a yield spike since bond prices (value of the TLT fund) move inversely to rates. Some of the biggest trades of the day Friday were betting on a big rate spike and subsequent move lower in the fund.

A US interest-rate strategist at TD Securities said that for interest rates to come off the highs and return to previous levels, a catalyst that drives oil prices lower is needed.

A March 17 Bloomberg story said pressure on bonds is likely to persist as long as Hormuz remains closed.

“This price action is concerning for two reasons,” said Priya Misra, a portfolio manager at JPMorgan Asset Management. “Long-end rates are rising globally which tend to feed on each other, and the prospect of Fed hikes is coming into the market narrative.”

In a nutshell, she said, “the rate range has moved higher unless the Strait is opened.”

The primary worry is hotter inflation, which is spoiling bets that incoming Fed Chair Kevin Warch will cut interest rates. Investors are also seeking higher rates on longer-dated Treasuries because of worries over swelling US deficits, and whether the economy is resilient enough to withstand the war’s negative effects.

“There is a sense that the bond market is requiring more of a concession to own new Treasuries in this environment,” said Kevin Flanagan, head of investment strategy at WisdomTree. “The inflation narrative is dominating the market.”

There’s a good chance, he said, that the next consumer-price report will show 4% annual inflation, which would be the highest since 2023. It was 3.8% in April.

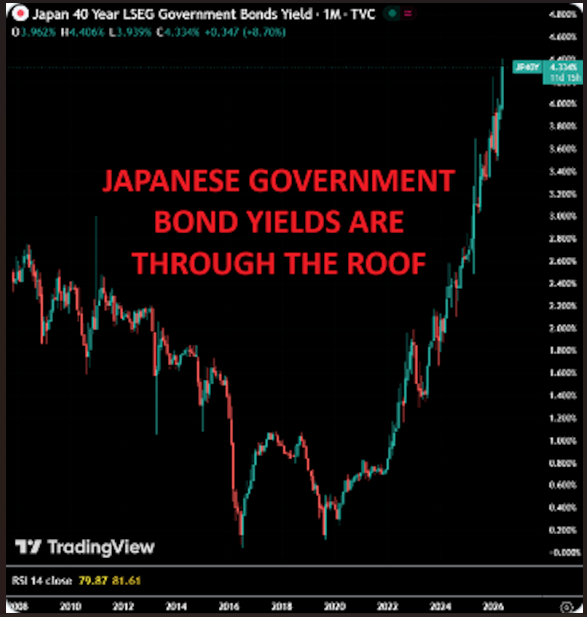

Japanese yields go parabolic

As mentioned, it isn’t only US long-term bonds that are being dumped by investors out of an abundance of caution.

According to a Reuters video, Japan’s government will likely issue fresh debt as part of funding for a planned extra budget to cushion the economic blow from the war.

On Monday, the 40-year Japanese government bond rose to 4.33%, the highest level since the bond was introduced in 2007. The 30-year bond breached 4.40% for the first time in history.

According to a tweet by Global Markets Investor,

The surge in government bond yields is global, driven by surging oil prices raising inflation and rate hike expectations.

Furthermore, growing fiscal concerns in Japan over increased bond issuance and energy relief measures are adding further pressure.

Political instability in the UK is adding another layer of uncertainty.

Global government borrowing is getting increasingly expensive and bond markets are the most important markets to watch right now.

Bloomberg said Japan’s 5-year government bond auction on Monday saw lower demand than the 12-month average, with the yield topping 2% for the first time this century.

Meanwhile, the yen is weakening toward 160 per dollar despite multiple rounds of intervention by Japanese authorities. That’s adding to inflation risks and weighing on sovereign debt as pressure mounts for the Bank of Japan to raise rates after holding policy steady last month.

Overnight index swaps suggest traders are pricing an about 80% chance of a rate hike next month…

Reuters said the European Central Bank is seen hiking as early as next month, and the Bank of England about twice this year. In Europe, Germany’s bund futures and French OAT futures fell about 0.4% and 0.45%, respectively. UK gilt yields surged last week, hitting their highest in decades.

Pressures mounted on Prime Minister Keir Starmer to resign over his party’s hefty losses in local elections.

Inflation threat

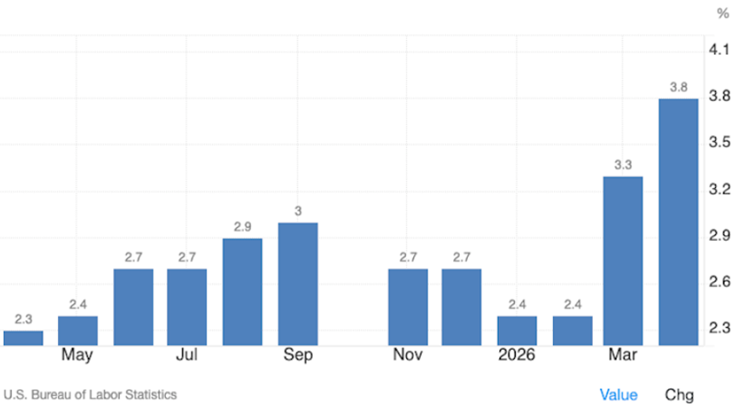

US inflation in April rose 3.8%, the highest since May 2023. According to Trading Economics, energy costs jumped 17.9%, the steepest annual increase since September 2022, compared to 12.5% in March, mostly due to gasoline (28.4% vs 18.9%) and fuel oil (54.3%). Inflation also accelerated for shelter (3.3% vs 3%) and food (2.3% vs 2.7%).

One source says 4% US consumer inflation, the CPI, “is rapidly coming into view.”

The last thing the Fed would do in an inflationary environment is cut interest rates, since this results in consumers and businesses spending more, which drives prices even higher.

According to the Gains, Pains & Capital blog, the fact that the Federal Reserve has rates at 3.5%, but the yield on the US 2-year Treasury, which the Fed typically follows, is over 4%, “suggests that the Fed WON’T be cutting rates again in 2026 and that in fact, we can expect some rate hikes in the next 24 months.”

The below 2-year charts for US, British and Japanese bonds, by financial blogger Graham Summers, mean higher inflation is coming.

Economist Peter Schiff flags the Producer Price Index (PPI) as a leading warning for the Consumer Price Index (CPI). In a May 15 podcast, Schiff said:

But the real bad news is not the CPI that we got yesterday; it’s the PPI that we got today because this means that the CPI that we get next month is going to be much worse because the producers are gonna now pass on these price hikes to their customers. … Well, last month producer prices were up point five; the expectation for April was an increase of point seven; the actual increase was twice that amount: one point four percent was the increase in one month. That’s more than half of the Fed’s two percent target in just one month.

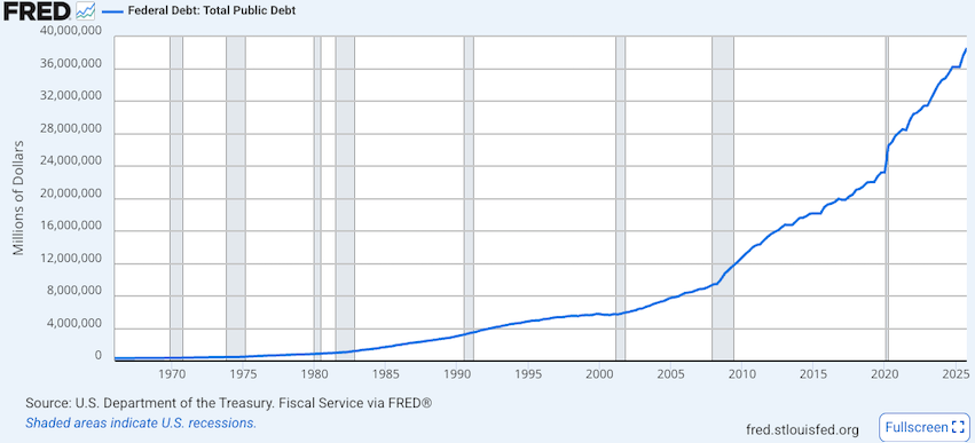

Schiff used a historical comparison to show how painful high rates would be today given the much higher federal debt, which is approaching $39.3. trillion:

Think about this though: rates are the highest they’ve been in about 19 years, but the chart and the trend are what’s important. What happens if rates get back to where they were in 1991? Now you’re looking at a 30-year yield at 8 percent; 8 percent in 1991 the national debt just hit 3 trillion; we have a debt that’s 10 times as high as it was in 1991.

Risk to equities

At the top of the article, I said that the global bond market is significantly larger than the global stock market. But many investors eschew bonds and are instead invested in stocks or mutual funds.

That’s what is scary about the bond market selloff. While the S&P 500 is up over 7% this year, there is a heightened risk that the bond rout could bleed into equities.

According to Bloomberg’s May 19 story,

“The ability of US equities to withstand the current bearish move in Treasuries is the true litmus test of the bond selloff,” said Ian Lyngen, head of US interest-rate strategy at BMO Capital Markets in New York. “We suspect that if and when 30-year rates manage to reach 5.25% in the next few weeks, there will be a more durable pullback in equity valuations.”

Reuters wrote that US stock markets have not yet priced in the risk of rocketing inflation and are vulnerable to a sharp spike in bond yields.

Equities are trading higher due to robust first-quarter earnings and expectations of boosts from artificial intelligence that are overshadowing the risks of high energy prices and the ongoing war with Iran.

Reuters notes that rising benchmark yields tend to put pressure on equity valuations, as companies and consumers will face higher borrowing costs. This can also weigh on economic growth and corporate profits, while possibly making bond returns more competitive with stocks…

“I do think there is a real fear that inflation is kind of embedded in the economy going forward,” said Peter Tuz, president, Chase Investment Counsel, in Charlottesville, Virginia. “You don’t see any signs of it going down right now, and that is a real fear, and it will drive the market down if it continues.”

Bond vigilantes

There is a group of powerful investors that not only watch US Treasury yields closely but they also take an active part in influencing the bond market, especially if they don’t like the economic policies of the administration.

Bond vigilantes are investors who sell government bonds in response to fiscal policies they view as inflationary or irresponsible, driving up borrowing costs for the government. — Investopedia definition

The term was coined by economist Ed Yardeni in the 1980s.

Historical examples of bond vigilantism occurred in the early 1980s, during the Clinton administration of the ‘90s, in the early Obama years, and most recently, following Donald Trump’s election victory in 2024, when US Treasury yields jumped from 4.29% to 4.42% in a single day — the big move attributed to concerns about spending and tax cuts under the new administration. (Investopedia)

According to Fortune, Bond vigilantes are protesting mounting US fiscal deficits and inflation risks by dumping government bonds, causing 30-year Treasury yields to surge near 5.2% — their highest levels since the Great Recession. They are warning that if the Federal Reserve doesn’t tighten credit, they will force borrowing costs higher.

China selling Treasuries

As mentioned the demand for government bonds is low. The way the US Treasury manages its spending is by issuing government debt to countries who hold it as part of their foreign exchange reserves.

The three largest US Treasury holders are Japan, the UK and China, at $1.19 trillion, $927 billion and $652 billion respectively. If governments abroad significantly slow or stop their Treasury purchases, the US government would be in serious trouble. It would have to print money to buy the Treasuries themselves, a policy move known as quantitative easing, or QE. QE is highly inflationary.

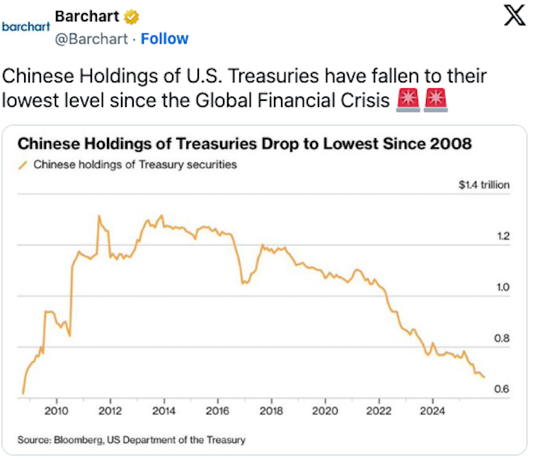

According to the South China Morning Post, Mainland Chinese investors shed their holdings of US Treasury bills in March, joining many overseas institutions and central banks amid uncertainties over the US-Israel war on Iran.

Data released by the US Treasury Department found the world’s second-largest economy cut its holdings to $652.3B from $693.3B a month earlier.

A Barchart tweet below shows Chinese holdings of US Treasuries have fallen to their lowest level since the financial crisis.

Five reasons why investors are selling government bonds:

- Higher oil prices because of the Iran war. Oil matters for inflation because it feeds into almost everything people buy and use. Companies often pass those higher costs on to consumers, pushing up prices across the economy, and cause investors to sell bonds over concerns central banks may keep interest rates higher for longer to combat higher prices.

- Strained government budgets. Already high budget deficits and promises from authorities from Tokyo to Washington to spend even more are also denting demand for bonds.

- AI and demand for chips. Prices of semiconductors and other components behind the AI investment boom are soaring and stoking inflation worries.

- Central banks and interest rates. Investors are worried that central banks are falling behind on fighting inflation. When investors think rates will stay higher, bonds become less attractive and they sell debt.

- Global growth is holding up. Economic data has shown that the US economy is still resilient. Why would you buy bonds when they typically act as your insurance against an economic downturn?

Global spending crunch

As bond yields surge, investors are growing wary of a global spending crunch. High bond yields threaten a severe hit to the spending power of governments, businesses and households, Bloomberg states in a May 18 piece.

The average rate at which governments in the Group of Seven richest nations pay to borrow for 10 years is approaching 4%, up from around 3.2% before the war started in late February. The yield on the 10-year U.S. Treasury note is around 4.6%, its highest level in more than a year and a source of concern among investors given its role as the key borrowing rate in the world’s largest economy.

The risk of longer-lasting inflation has ignited concern that central banks will need to quickly raise interest rates, potentially amplifying economic fallout — and putting G7 governments in a tight spot in terms of policy.

“Yields are going to go higher until something breaks. The wild part is Iran knows this,” said Jack McIntyre, portfolio manager at Brandywine Global Investment Management in Philadelphia. “I would say we’re in that range right now where the equity market is paying attention to bonds. The closer we get to 5%, the more that pressure builds.”…

Kenneth Broux, head of corporate research, FX and rates at Societe Generale, said to stop what he called a “slow-motion crash” in the bond market would require a retreat in oil prices, recession fears growing enough to spark a safe-haven rush to bonds, or prices falling low enough to attract buyers.

MSN recently reported that ‘The US is in a league of its own when it comes to its debt burden, as rating agencies bemoan ‘long-running deterioration’ in fiscal governance’.

The country “beats out the competition when it comes to the size of its debt burden, as the nation’s public liabilities have exceeded the size of its economy for the first time since World War II.”

Moreover, the Committee for a Responsible Federal Budget (CRFB) announced that US debt held by the public, estimated to be $31.27 trillion, officially surpassed the country’s annual GDP of $31.22 trillion in March.

Rising debt comes with a long list of economic risks, including the threat that the cost of servicing that debt might crowd out other essential government spending. Another consequence would be a deterioration of the country’s once-top tier credit rating, a scenario that could lead to higher borrowing costs and even more constrained government spending.

The Warsh factor

One last thing we need to talk about: Faster inflation will make it harder for the central bank to lower interest rates and add pressure on incoming Fed Chair Kevin Warsh.

Reuters reported this week that Warsh’s arrival leaves long bonds without a safety net. What does that mean?

Start with the assumption that Warsh is a long-time opponent of Fed bond-buying, aka quantitative easing (QE). He advocates the opposite, i.e., running down the central bank’s $6.7 trillion balance sheet of mostly Treasury securities.

(The Fed typically steps in and buys bonds when the usual buyers aren’t snapping them up at auction — like currently. If the Fed doesn’t buy the bonds, who else will? And what would happen to US government spending which relies on Treasury buying to finance it?)

What seems clear to most Fed watchers is that it couldn’t happen immediately, especially not in the current market environment.

The argument for running down the balance sheet centers on first shortening the maturity of its holdings to Treasury bills of 12 months or less and then being able to more easily run them off as those bills mature.

Whatever the route or timetable, there seems little chance that Warsh would support any further buying of long-term debt – 10-year tenors or longer – even in a fresh shock or crisis.

That leaves the very long end of the market without the effective safety net it’s enjoyed for 18 years since the Fed first launched quantitative easing (QE) after the 2008 banking crash…

In the end, the mere uncertainty about how markets would react to the next shock – without the certainty of Fed intervention – may be enough to demand a higher risk premium anyway.

In layman’s terms, that means higher interest rates are coming.

Conclusion

Government bond yields around the world, including in the US, are hitting multi-decade highs as investors price in higher-for-longer inflation due to the Iran war.

Interest rates, or yields, that governments pay on their debt can drive the global economy — when rates are low, countries are able to spend more freely and drive economic growth. (Axios)

When rates are high, their ability to spend is restricted by higher borrowing costs. Governments, businesses and households end up borrowing less, and spending less, driving down economic growth.

The market before the war was pricing in two to three interest rate cuts in 2026. Market participants now think the Fed’s next move will be a rate raise, mostly due to war-related inflation that is reverberating through the global economy.

US inflation in April rose 3.8%, the highest since May 2023. Energy costs jumped 17.9%, the steepest annual increase since September 2022.

The bigger worry is the Producer Price Index, which increased in April by 1.4%, double the expectation. Producers are almost certain to pass these higher costs onto their customers, which will likely mean consumer inflation soon tops 4%.

The appropriate policy response to higher inflation is higher interest rates. Higher rates not only restrict the borrowing capacity of governments, but they also put pressure on spending.

As MSN recently reported, Rising debt comes with a long list of economic risks, including the threat that the cost of servicing that debt might crowd out other essential government spending. Another consequence would be a deterioration of the country’s once-top tier credit rating, a scenario that could lead to higher borrowing costs and even more constrained government spending.

The “line in the sand” for the 30-year “long bond” is 5%. That’s supposed to spark dip-buying, but there are few buyers even at 5.1%. Could the yield go even higher to attract investors into tying up their money for three decades? It appears quite likely.

The 2-year yields on US, UK and Japanese bonds all suggest higher inflation in on the way. The US 10-year yield @ 4.59% is close to a 10-year high. The 2-year is only about a percentage point away.

The next domino to fall could be US stock markets, which despite the uncertainty of war, are soaring.

Reuters notes that rising benchmark yields tend to put pressure on equity valuations, as companies and consumers will face higher borrowing costs. This can also weigh on economic growth and corporate profits, while possibly making bond returns more competitive with stocks…

Indeed, stock markets, unlike bond markets, have not yet priced in inflation. When they do, look for a correction.

What needs to happen to end the bond rout, lower inflation risks and reverse all the negative consequences that come with higher interest rates? Clearly the answer is an end to the Iran war and the re-opening of the Strait of Hormuz.

Unfortunately, the daily news reports on the prognosis for peace in the Middle East do not bold well for a swift resolution to the crisis.

Richard (Rick) Mills

aheadoftheherd.com

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.

{kind=link}

{kind=link}

{kind=link}