Why Canada and the United States need more smelters and refineries – Richard Mills

2026.03.12

A country’s ability to mine minerals and turn them into metals depends on two distinct but connected phases: mining and smelting/ refining.

(To clarify, smelters extract metal from ore or scrap using high heat to create a raw, impure alloy (approx. 80–95% purity). Refineries take this material and use chemical or electrolytic processes to remove remaining impurities, achieving high-purity levels of 99.5% to 99.9% or higher (AI Overview))

We can dig metals out of the ground minerals; what we lack is separating, purifying and refining capabilities.

This sentence was written about rare earths, arguably the most difficult to mine and refine because, A/ they are so hard to find in economic concentrations; and B/ they are so chemically similar. Refining them means separating 15+ different elements that behave almost identically in chemical reactions.

The bottleneck is not in the mining but the refining of rare earths.

Indeed, separating and extracting a single rare earth element takes a great deal of time, effort and expertise. For more read the section on ‘Rare earths 101’ in this 2018 article by AOTH

China is the only country that carries out all three stages — separating, purifying and refining — with Australia and the United States selling some of their semi-processed ores back to China to complete the refining! (Polytechnique Insights)

In fact, China has a monopoly on the entire rare earths value chain. The country has progressively moved from extraction to separation to the manufacture of permanent magnets used in electric vehicles, wind turbines, many other civilian uses, plus key military applications.

China controls 94% of global permanent magnet production and 99% of global heavy rare earth processing capacity. Heavy rare earths are harder to process than light rare earths and are essential for high‑temperature defense applications. (Prinsights)

For example, an American F-35 fighter plane contains more than 400 kg of various materials containing at least one rare earth. Magnets made from Chinese rare earths are also used in the Joint Strike Fighter, the Pentagon’s answer to a one-size-fits-all warplane.

But this article isn’t about rare earths, at least, not exclusively. It’s about the lack of refining capacity in the United States and Canada that is becoming a problem as demand for certain metals increases and countries are looking inwardly at their mining and manufacturing capabilities. Countries are moving away from interdependent mineral supply chains in favor of those that guarantee security of supply.

China has weaponized rare earths, graphite, and other critical minerals to punish countries dependent on its refined metal products.

The United States is heading towards extreme isolationism as it pursues a mercantilist trade policy defined by import tariffs.

In our last article we wrote about how Canadian Prime Minister Mark Carney is diversifying the Canadian economy away from the United States by joining alliances with other “middle powers” like itself.

Canada on the right track with middle power policy — Richard Mills

However, this policy — which I fully support — does not address mineral processing. It’s one thing to allocate government money to new critical mineral mines and projects, but quite another to add the other missing pieces: energy to run the mines; roads or preferably, railways to the mines so that they can ship the concentrate out; and refineries to process the ore, thereby making Canada completely independent from current suppliers, mostly China.

In this article we’re looking at the refining bottleneck, illustrated by six metals: aluminum, copper, nickel, zinc, graphite, and rare earths.

Copper

A new report finds the United States produces more raw copper than it consumes but lacks the processing capacity to turn it into usable metal, leaving manufacturers dependent on foreign refiners.

Benchmark Mineral Intelligence found the US can meet 146% of its domestic copper demand through a combination of mine output and scrap, compared with just 40% for China, the world’s largest consumer. Yet nearly 48% of US mined copper concentrate is exported, largely because of limited domestic smelting and refining capacity.

The US produced 1,714 kilotonnes of copper in 2024, but it still depends heavily on imported refined copper for industrial use. Domestic concentrate and scrap are often shipped overseas, frequently to China, for processing before copper cathode is exported back to US buyers.

Do you see now why I started with rare earths? This is the exact same thing that happens with REEs. Only instead of getting copper cathodes back the US is getting permanent magnets.

The report also states that The key constraint for the US is downstream processing capacity needed to convert concentrate into copper cathode, the refined metal manufacturers use. Benchmark’s analysis suggests expanding domestic refining capacity would strengthen supply security more effectively than acquiring additional raw material assets abroad.

Allow me to rephrase. To achieve security of supply, it would be better for the US to build more copper refineries than it would be to buy more foreign copper mines.

In fact, the United States is more self-sufficient in raw materials via domestic mining and scrap (recycling) than China, says Benchmark’s copper analyst Albert Mackenzie. The problem is the US doesn’t have the processing capacity.

The main difference between the two countries, MINING.COM explains, is that limited US processing capacity means copper from US-owned mines abroad does not return home, while Chinese-owned overseas output more often flows back to Beijing.

China, often viewed as self-sufficient, consumes far more copper than it produces and relies heavily on imported raw materials.

China, though, can process them in huge quantities, unlike the US.

Let’s illustrate this with some numbers.

There are currently two copper smelters in the United States: Freeport-McMoRan’s (NYSE:FCX) Miami smelter in Arizona and Rio Tinto’s (NYSE:RIO) Kennecott smelter in Utah. Both process copper concentrate. There is also the Hayden smelter in Arizona owned by Asarco (Grupo Mexico), but that has been shut since 2019.

The Amarillo refinery in Texas processes anodes and is linked to Asarco’s Arizona’s operations.

According to the US Geological Survey, the vast majority of US copper mining occurs in Arizona, Utah, New Mexico, Nevada and Montana.

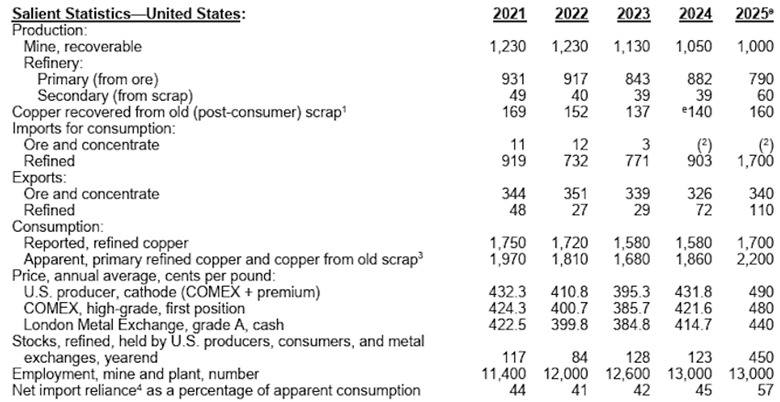

In 2025 the United States refined 790,000 tonnes of copper and exported 110,000 tonnes. Interestingly, total refined copper imports were exactly the same as total refined consumption: 1.7 million tonnes.

Between 2021 and 2024, the most refined copper was imported from Chile (68%), followed by Canada (16%), Peru (7%) and Mexico (6%).

Refined copper accounted for 88% of all unmanufactured copper imports.

The first takeaway is that 100% of the refined copper the US imported went to consumption. Only 100,000 tonnes were exported.

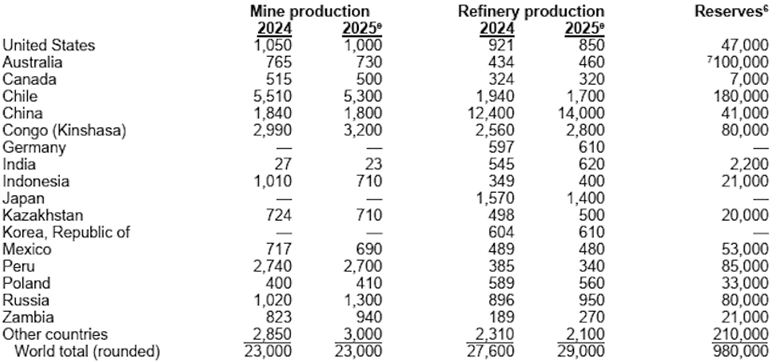

The second takeaway is that China is nowhere to be seen, even though China is by far the world’s largest copper refiner at 14 million tonnes in 2025 versus the United States’ 850,000 tonnes.

In Canada, the only operating copper refinery is Glencore’s (LSE:GLEN) Canadian Copper Refinery (CCR) in Montreal, Quebec. It produces 99.99% pure copper cathodes and operates alongside the Horne smelter in Rouyn-Noranda, Quebec, which produces copper anodes.

Canada mined just 500,000 tonnes of copper last year, and refined only 320,000t, compared to global refined production of 29 million tonnes.

In a previous article we discussed the possibility of building a new copper refinery in the Golden Triangle region of British Columbia.

BC’s Golden Triangle is the West’s solution to its copper supply dilemma

BC is Canada’s leading copper producer, outputting about half of the country’s total, yet nearly all the copper mined from British Columbian operations is shipped to Asia. This needs to change.

Aluminum

Primary aluminum smelters in the United States are concentrated in a small number of locations and are operated mainly by Alcoa and Century Aluminum. Key operating facilities include Massena, New York; Mt. Holly, South Carolina; Sebree, Kentucky; and Warrick, Indiana.

In 2025, two smelters ran at full capacity throughout the year, while two operated at reduced capacity. The remaining two — located in Hawesville, Kentucky and New Madrid, Missouri — have been temporarily shut down since 2022 and 2024, respectively.

Century Aluminum has reportedly sold the Kentucky site to digital infrastructure company TeraWulf.

Reuters reports that, while Trump hiked aluminum tariffs to 50% last year, the benefit has been limited to Century’s restart of 50,000 tonnes of annual capacity at its Mount Holly smelter in South Carolina. The plant, says Reuters, is due to return to near-capacity utilization of 220,000 tons per year by the middle of 2026.

Emirates Global Aluminium is planning a new $4 billion, 500,000-tonne-per-year facility near Inola, OK, which would be the first new aluminum smelter in the US since 1980.

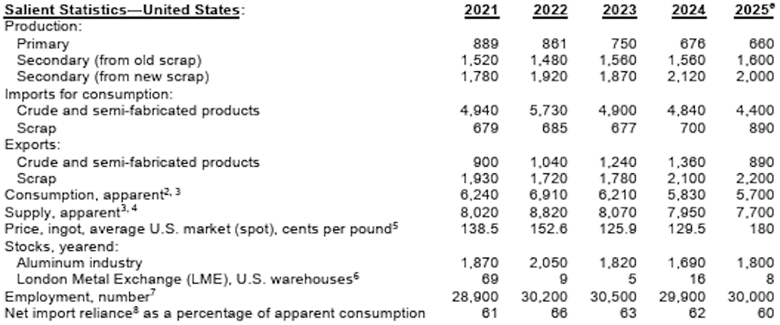

In 2025, the US smelted 660,000 tonnes of primary aluminum, falling far short of the 5.7Mt of consumption. To help fill the gap, the US imported crude and semi-fabricated products totaling 4.4Mt.

The majority of refined aluminum came from Canada (56%) followed by United Arab Emirates @ 8%, Bahrain at 4% and China at 3%.

China leads global smelter production @ 46Mt compared to the United States’ 660,000t and Canada’s 3.3Mt.

Canada has 10 primary aluminum smelters, with nine located in Quebec and one in Kitimat, British Columbia, producing low-carbon aluminum using hydroelectricity. Major operators include Rio Tinto, Alcoa and Aluminerie Alouette.

The largest is the Alouette facility in Sept-Îles, QC with a capacity of about 632,000 tonne a year.

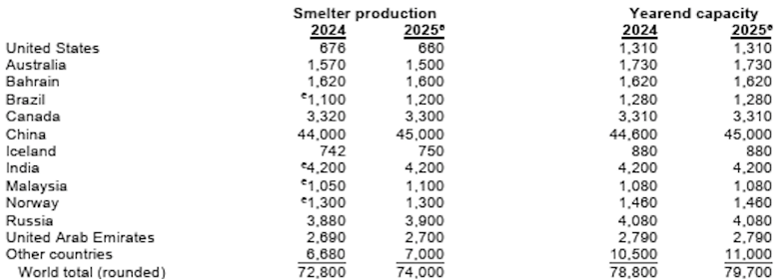

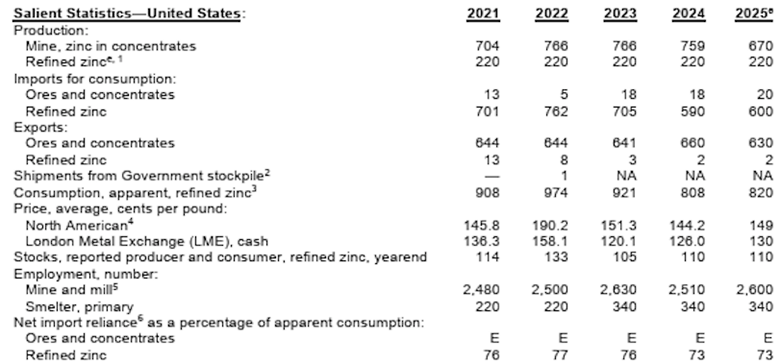

Zinc

The United States has only one primary zinc smelter, operated by Nyrstar in Clarksville, Tennessee.

According to the USGS, zinc is mined in five states at six mining operations by five companies. Two smelter facilities, one primary and one secondary, operated by two companies, account for most of the commercial-grade zinc metal produced in the United States.

In 2025, refined zinc production totaled 220,000 tonnes and refined imports for consumption were 600,000 tons, filling US consumption of refined zinc @ 820,000 tonnes.

Refined metal imports were led by Canada @ 57%, followed by Mexico @ 15%, Peru @ 8% and South Korea @ 7%.

Canada’s primary zinc smelting and refining sector is dominated by Anglo Teck’s Trail operations in British Columbia and Glencore’s CEZinc refinery in Quebec. A third smelter, General Smelting of Canada, also under Glencore, specializes in lead and zinc alloy production.

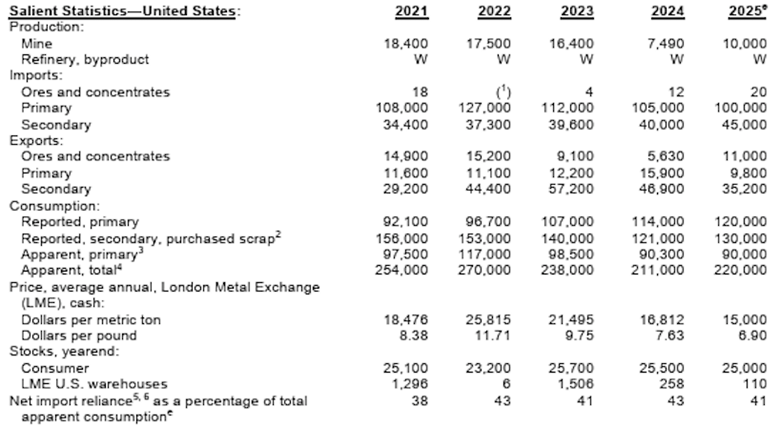

Nickel

The United States has no commercial‑scale nickel refining capacity and relies almost entirely on imports, or on exporting nickel concentrate —primarily to Canada — for processing. The Eagle mine in Michigan is the only active nickel mine.

The USGS says that in 2025, there was no refined nickel production, with imports of primary nickel totaling 100,000 tonnes not quite meeting primary consumption of 120,000 tonnes. Total consumption of primary plus secondary nickel reached 220,000 tonnes.

Primary nickel is nickel refined from sulfide or laterite ores into products like pure metal, ferronickel or nickel matte. Secondary nickel is nickel recycled from scrap.

Canada has three nickel refineries. The first, operated by Glencore, is in Sudbury, Ontario. The second is Sherritt’s (TSX:S) Fort Saskatchewan refinery in Alberta, and the third is Vale’s (NYSE:VALE) Long Harbour processing plant in Newfoundland Labrador.

A fourth project near Timmins, ON, Crawford Nickel, is slated to begin producing low-carbon nickel around 2028.

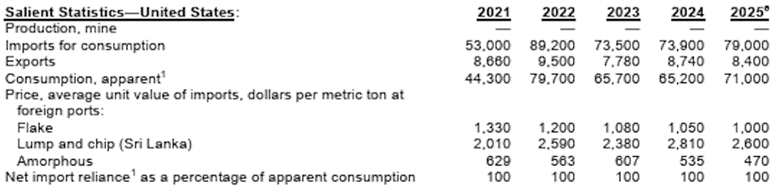

Graphite

In 2025, no natural graphite was produced in the United States. However, Syrah Resources (ASX:SYR) uses feedstock from its Mozambique mine at its processing plant in Vidalia, Louisiana.

Other graphite refining facilities in the works:

- Graphite One (TSXV:GPH) is developing an Advanced Anode Materials (AAM) manufacturing facility in northeastern Ohio. The plant is designed to manufacture synthetic and natural graphite anode active materials using feedstock from their planned Graphite Creek mine in Alaska.

- Westwater Resources (NYSE:WWR) is developing a battery-grade graphite processing plant in Kellyton, Alabama, which will produce purified spherical graphite.

- Volt Resources (ASX:VRC) is planning to industrialize a proprietary hydrofluoric acid-free process for producing battery-grade graphite, with intentions to commission a refinery in Alabama.

- Titan Mining (TSX:TI) in December 2025 announced that ore feeding had commenced at its Kilbourne graphite demonstration facility in Gouverneur, NY. The facility aims for 1,000 to 1,200 tonnes per year initially, with plans to scale up to 40,000 tpy.

According to the USGS, in 2025 79,000t was imported for consumption of 71,000t, with exports of 8,400t. There was no data on refined graphite. The main importing nations from 2021-24 were China @ 46%, Canada @ 13%, followed by Mozambique and Mexico at 13% and 12%, respectively.

China is by far the largest graphite miner globally, producing 1.4Mt in 2025 against Canada’s 8,000 tonnes and the United States’ zero. It also refines more than 90% of the world’s graphite into the material that is used in virtually all EV battery anodes.

An AI Overview says Canada is rapidly developing its graphite refining and processing capacity to support the electric vehicle supply chain, with major projects in Quebec and Ontario. Key developments include Nouveau Monde Graphite’s (NYSE:NMG) Bécancour plant in Quebec, Norwegian company Vianode’s synthetic plant in Ontario, and Northern Graphite’s (TSXV:NGC) planned battery anode material facility.

Northern Graphite’s Lac des Iles mine in Quebec is currently the only operating natural graphite mine in Canada.

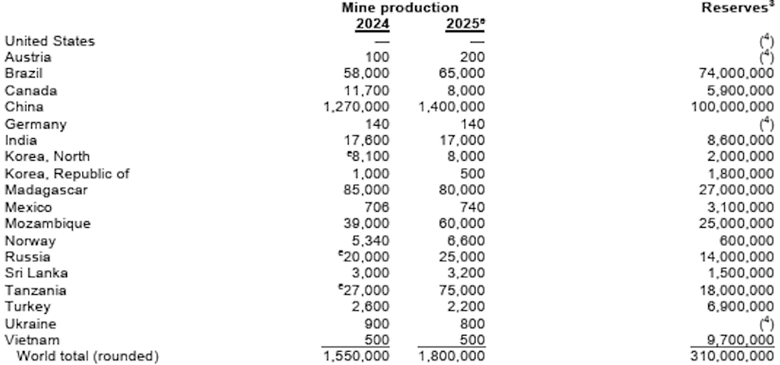

Rare earths

Mountain Pass in California, operated by MP Materials (NYSE:MP) is the only rare earths mine currently in the United States. The mine produces neodymium-praseodymium needed for NdPr magnets.

An AI Overview states that to break dependency on Chinese processing, the US is developing new capabilities. Ucore Rare Metals (TSXV:UCU) is developing RapidSX technology in Louisiana, while REalloys (NASDAQ:ALOY) is developing heavy rare earths refining in Ohio. Other emerging projects include Phoenix Tailings and Lynas USA.

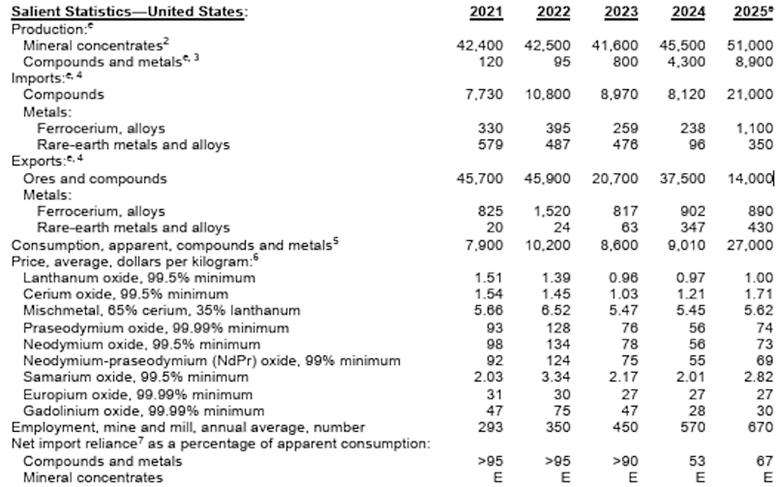

According to the USGS, in 2025 an estimated 51,000 tonnes of rare earth oxides in mineral concentrates were produced in the US.

Another 8,900t of compounds and metals were produced.

The United States imported 21,000t of compounds and 350t of rare earth metals and alloys. Between 2021 and 2024 the main source of rare earth compounds and metals was China, @ 71%. Malaysia, Japan and Estonia followed, at a respective 13%, 5% and 5%. These were derived from mineral concentrates and chemical intermediates produced in Australia, China, and elsewhere, the USGS states.

Canada’s Saskatchewan Resource Council rare earth processing facility in Saskatoon, SK is Canada’s first commercial-scale rare earths refinery. It produces magnet-grade NdPr metal, plus dysprosium and terbium oxides, at a rate of about 400 tonnes per year, enough for 500,000 electric vehicles. An expansion is planned for 2027.

Other Canadian rare earths refineries in the works include Ucore’s demonstration plant to refine rare earths in Kingston, ON using Rapid SX technology; Quebec’s Torngat Metals which has partnered with France’s Carester for REE processing; and Cyclic Materials, developing a recycling plant in Ontario to recover rare earth elements.

Conclusion

The bottom line is that Canada and the United States remain dependent on refined metal imports for all the minerals discussed here: aluminum, copper, nickel, zinc, graphite and rare earths.

While much has been done to develop a mine-to-magnet supply chain in the US, the country still gets 71% of its rare earth compounds and metals from China. For some REEs the concentration is much higher. For example, 93% of US yttrium, used in color TVs and LED displays, comes from China.

China is by far the largest graphite miner globally, producing 1.4Mt in 2025 against Canada’s 8,000 tonnes and the United States’ zero. It also refines more than 90% of the world’s graphite into the material that is used in virtually all EV battery anodes.

But it isn’t only China. The US is dependent on Canada for its aluminum, nickel and zinc, importing a respective 56%, 44% and 57%. It gets 68% of its refined copper (68%) from Chile and 16% from Canada. Other top importers are Peru and Mexico. China isn’t in the mix.

When the US imposed tariffs export controls on rare earth minerals to the US about a year ago, it was suggested that Canada could be an alternative supplier. For example, Rio Tinto produces scandium at its titanium plant in Quebec.

China also restricted exports of antimony, gallium and germanium.

While the US used to rely on China for about 23% of its germanium needs, Canada supplies roughly the same amount to the Americans, according to a Globe and Mail story. It notes that Anglo Teck produces germanium dioxide at its Trail smelter in British Columbia and it is the only Canadian supplier to the US. Anglo Teck’s germanium is produced as a byproduct from the zinc it mines at its Red Dog mine in Alaska.

But remember, these are oxides. Refining them into metal is a lot more complicated, expensive and environmentally unfriendly, with toxic byproducts needing to be disposed of safely.

Canada and the US are making inroads into rare earths refining but it’s early days. For the foreseeable future, China remains the most important supplier of useable metal derived from most rare earths.

It makes little sense to dig up rare earths and other metals, for that matter, and export the concentrate offshore for processing. Security of supply implies a complete supply chain that begins with mining the minerals and ends with refining the metals into finished products.

It’s good to see this message has started trickling up to government. Another Globe story published on March 9 reports that mining experts and executives called in a parliamentary committee for Canada to immediately address its fragility in critical minerals refining capacity to bolster this country’s defence capabilities.

Modern defence systems, including advanced communication networks, aerospace sensors, autonomous systems and electrified military infrastructure all heavily rely on access to critical minerals such as nickel, copper, cobalt and rare earth elements, Nadia Mykytczuk, executive director of the Goodman School of Mines at Laurentian University in Sudbury, said in her testimony to the standing committee on national defence.

“The real strategic vulnerability today is not our geology,” she said. “It is our processing capacity and supply chain dependence. In many cases, Canadian minerals are exported for refining and upgrading abroad before returning its inputs into advanced technologies.”

Reliance on foreign refining for defence minerals exposes Canada to supply disruption, export controls and geopolitical pressure, she added.

Canada is fast-tracking a set of nation-building projects through the Major Projects Office, centered on critical minerals, energy transition, and infrastructure. Railways and smelters/ refineries for British Columbia are sadly not mentioned.

Carney’s plan does facilitate the mining of more ie. copper concentrate. To be shipped to Asia and returned to us as refined metal or manufactured goods.

This problem isn’t news to us at AOTH. We have the minerals. The answer is to build not only more mines, but more transportation and processing related infrastructure. We need such infrastructure to connect to future mines, not to ports to export the concentrate, but to smelters and refineries that can process it domestically.

Only then will be safe from the weaponization of mineral exports countries like China have employed as leverage in trade wars.

Richard (Rick) Mills

aheadoftheherd.com

Subscribe to AOTH’s free newsletter

Richard does own shares of Graphite One (TSXV:GPH). GPH is a paid advertiser on his site aheadoftheherd.com This article is issued on behalf of GPH

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.

{kind=link}

{kind=link}