Quiet quitting and war crashing US bond market – Richard Mills

2026.03.25

US President Trump has reneged on his promise to the American people of making life more affordable by starting a war with Iran that has entered its fourth week.

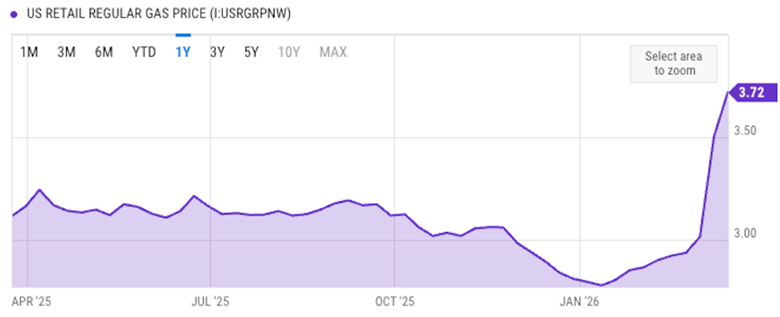

Iran’s closure of the Strait of Hormuz, along with attacks on oil and gas infrastructure in the neighboring Gulf states, have pushed oil prices above $100 a barrel. Gasoline prices have risen about 30% in the US and in Europe they have doubled.

Other commodities that, without naval ships escorting tankers through the narrow waterway, are trapped in the Persian Gulf, include LNG, distillates like diesel and jet fuel, aluminum, fertilizer, and sulfur used in metals (ie. copper, nickel) refining.

Prices of these inputs are rising fast, with shortages a major concern for the industries that rely on them.

According to Fortune, about one-third of global seaborne fertilizer passes through Hormuz. Persian Gulf nations export nearly half of the world’s urea and 30% of its ammonia. The Fertilizer Institute claims fertilizer prices are up roughly 30%, dealing a blow to farmers, and elevating substantially the risk of food inflation.

Qatar Energy, one of the world’s biggest exporters of natural gas and a producer of urea for use in fertilizer, has stopped production following attacks on its facilities.

CNBC reported last week that aluminum prices hit a four-year high, as the war in Iran upends global supply.

Treasury yields rising

A war in the Middle East has always been feared for its impacts on volatile oil and gas prices, but a less obvious, though equally serious outcome of the war, is its effects on the US bond market.

Typically, geopolitical stressors especially wars send investors clambering for safe-haven assets. US Treasuries have traditionally been among the safest. As buyers line up for them, prices of these government bonds rise as their yields fall. This time is different.

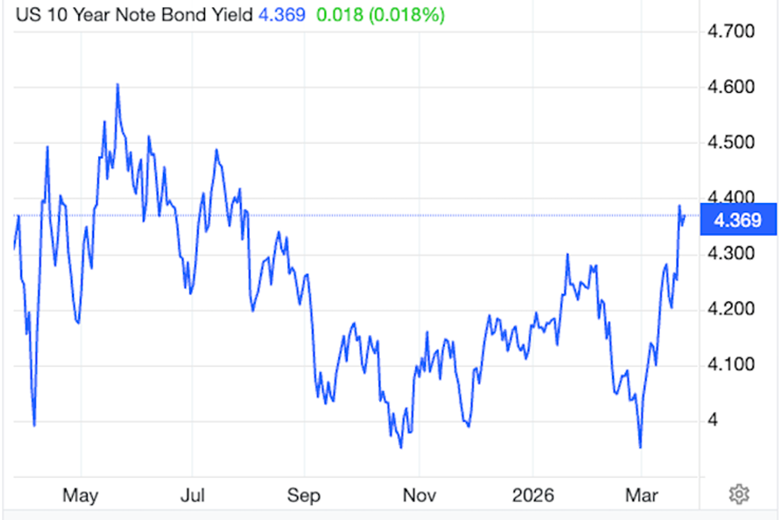

As of Tuesday, March 24, the 10-year yields 4.3% and the 30-year yields 4.9%. Even the 2-year bond jumped more than 9 basis points Tuesday to 3.925% after weak demand in a $69-billion auction. (CNBC)

The 20-year yield returned to the 5% level on Monday, though it has since slipped below that threshold.

In a column, ‘Paydirt’ Editor Doug Hornig writes It’s particularly important to keep an eye on the long bond (30-year Treasury), looking for a 5% yield. Think of that 5% rate as a formidable barrier. It was breached in the fall of 2023, and the spring and summer of 2025, and has been approached on numerous occasions. But as yet it has always drawn back. Why? There is nothing magical about a 5% yield. But it carries a disproportionate weight with the “bond vigilantes.”

A 5% yield suggests investors are demanding higher premia to hold long-term U.S. debt, signaling a fundamental reassessment of sovereign credit risk and a potential return of “bond vigilantes”—investors who sell bonds to force discipline on government fiscal policy. 30-year Treasuries have not consistently yielded more than 5% since 2007, just before the Global Financial Crisis.

Another reason for bond yields rising according to Luke Groman, founder and president of Forest for the Trees, The core issue stems from the heavy reliance on the U.S. dollar by foreign nations that are concurrently dependent on imported energy.

When oil prices spike, these nations sell dollar assets, starting with Treasuries because they’re the most liquid, so they can afford to buy more expensive oil. This puts downward pressure on bond prices and upward pressure on bond yields.

“Iran doesn’t have to beat the U.S. military, if it even could, which I doubt,” Groman told Kitco News. “All it has to beat is the bond market.”

The Guardian notes that consumers worldwide are bracing for a surge in living costs. Central banks, including the US Federal Reserve, Bank of England and European Central Bank, warn the war could have a material impact on inflation and dent global growth.

On Monday morning, Japan’s government bonds fell, pushing yields back towards multi-year highs as concerns mount that the Iran war will stoke inflation (Bloomberg).

Another Bloomberg piece said The specter of stagflation caused by the Iran war has wiped out more than $2.5 trillion from the value of global bonds in March, on track for the biggest monthly loss in more than three years.

Bonds are tumbling as a surge in oil prices quickens inflation, which erodes the value of the fixed payments from debt.

Financial blogger John Rubino notes the war in the Middle East has caused bond yields to spike and that the war’s cost and complexity are causing political turmoil. For example, an embedded CNN article is titled ‘Cracks emerge in GOP over Iran war as administration floats more than $200B request to Congress’.

Many lawmakers including Republicans are skeptical of approving the large sum for a conflict that has no timeline for ending military operations, and for which they were not asked to approve.

Rubino equates the current situation with that of the 1970s, “when interest rates and gold both spiked as confidence in the dollar and those managing it collapsed. Which is another way of saying interest rates spike as bonds traders rebel.”

Stagflation

Stagflation is an economic event in which the inflation rate is high, economic growth rate slows, and unemployment remains steadily high. (Corporate Finance Institute)

The multiplier effects of closing the Hormuz Strait are being felt across the globe.

Rightly so the war between Iran and the United States/ Israel is worrying investors that it could cause the return of 1970s-style stagflation.

“The risk of a 1970s scenario is rising,” said Kaspar Hense, portfolio manager at RBC BlueBay Asset Management. (Reuters)

The epicentre of stagflation fears is the surge in oil prices, and the biggest question for world markets now is how long will those prices remain elevated.

Capital Economics says a useful rule of thumb is that a 5% rise in oil prices adds about 0.1% to developed-market inflation.

High oil prices also dampen economic growth, with the IMF estimating that for every 10% rise in oil prices, global economic output decreases by 0.1 to 0.2%.

Oil price increases contributed to the twin energy crises of the 1970s and the US recessions in 1990 and 2008. Russia’s invasion of Ukraine in 2022 also triggered a major energy shock, particularly in Europe.

The United States was vulnerable to stagflation even before the war started.

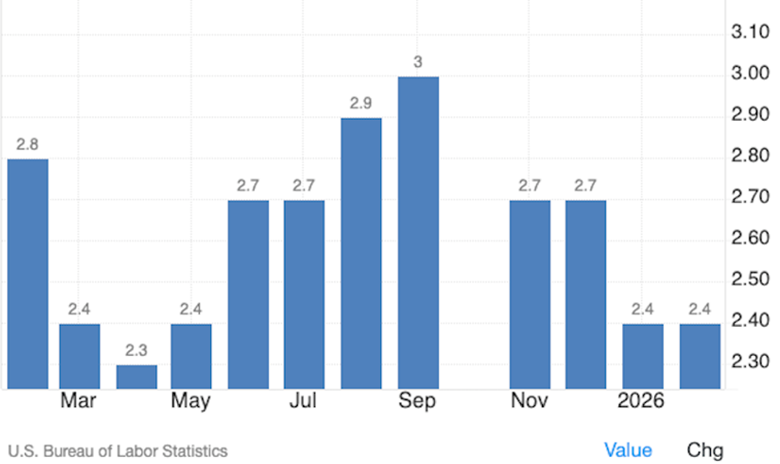

The economy lost 92,000 jobs in February, while the unemployment rate ticked up to 4.4%.

Data released earlier this month showed that CPI inflation in February was sticky, rising 0.3% over January and 2.4% year over year. Of course, the inflation print didn’t capture the effects this month’s oil price surge. Expect March’s number to be considerably higher.

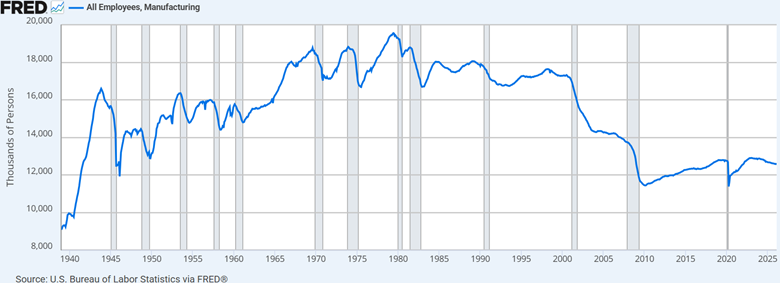

US manufacturing employment continues to shrink, with the sector losing another 12,000 jobs in February, to 12.57 million, the lowest since January 2022.

According to the Kobeissi Letter, manufacturing employment has contracted in 23 of the last 25 months, the longest losing streak since the financial crisis.

The Letter expects the Iran war to make the manufacturing recession even worse, because higher energy costs could force factories to cut even more jobs.

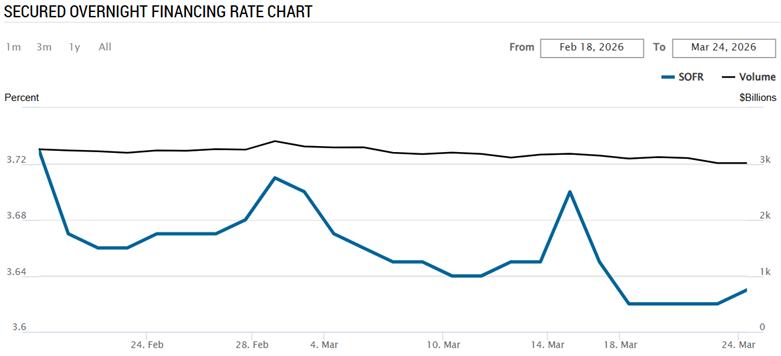

In a note published on March 13, Deutsche Bank strategist Steven Zeng said the biggest factor which has contributed to more than half of the 10-year yield’s climb, is the rise in secured overnight financing rates stemming from higher inflation expectations.

Ultimately, the bulk of the reasoning behind recent moves “is due to an oil price shock leading to inflation worries, forcing the Fed to stay on hold” with interest rates, Zeng said, via MarketWatch.

The third leg of the stagflation “stool” is low economic growth.

The Congressional Budget Office and the Trump administration have differing growth projections, with the CBO forecasting real GDP growth of 2.2% in 2026, trailing to an average 1.8% for the rest of the decade, versus the administration’s far more robust 3-4% range for 2026.

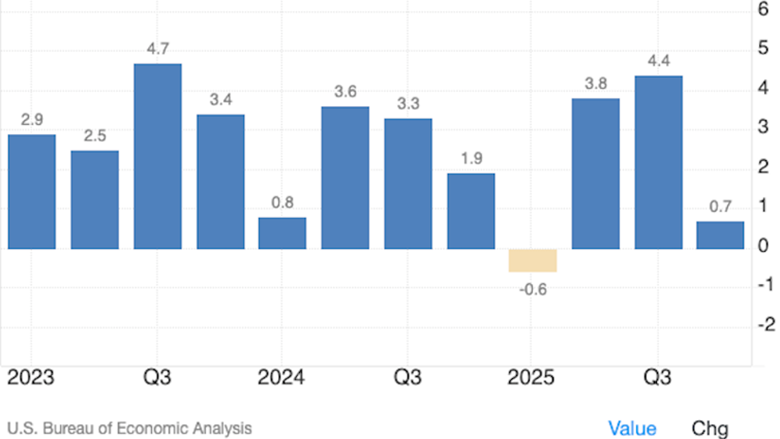

According to Trading Economics, the US economy expanded an annualized 0.7% in the fourth quarter of 2025, the weakest performance since the economy contracted in Q1 of last year, and well below expectation of 1.4% growth.

NBC News said the insipid growth was due to the 43-day government shutdown. Q4 was down sharply from 4.4% growth in Q3 and 3.8% in Q2. For all of 2025, the economy grew at 2.1%. It added the war with Iran has driven up oil and gas prices and clouded the economic outlook.

Financing the debt

The US government must either borrow money or print money to meet its financial obligations. Money-printing is inflationary, so the preferred option is to borrow.

Borrowing at low interest rates is preferable because it means that when bonds mature, and the interest is due, there is less to pay out than if interest rates were higher.

But the deficit and the debt keep climbing, and bond holders are demanding higher interest rates to hold bonds that are becoming increasingly risky given the country’s high indebtedness.

The numbers are alarming.

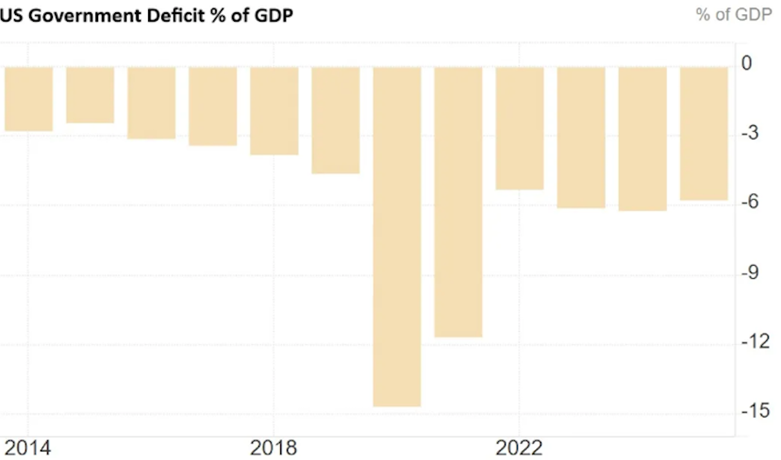

The Congressional Budget Office says the deficit will grow from about 5.8% of GDP in 2025 when Trump took office, to 6.1% over the next decade, reaching 6.7% in fiscal 2036.

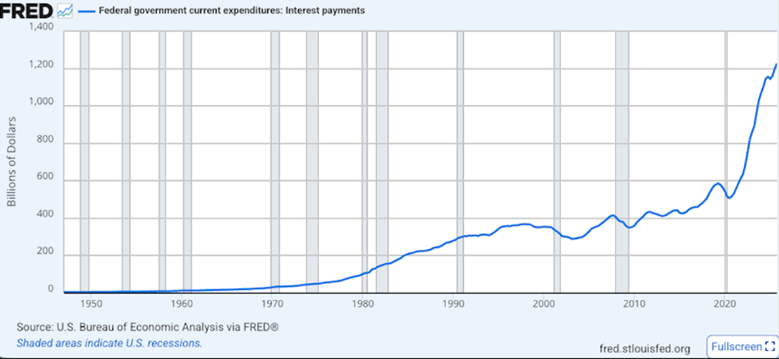

America reportedly borrowed $43.5 billion a week in the first four months of the fiscal year, which starts in October. The interest on that debt works out to over $1 trillion for 2026. Interest in 2024 and 2025 also exceeded $1 trillion.

If borrowing continues at this rate, the deficit will reach $1.8 trillion or higher, says the Committee for a Responsible Federal Budget.

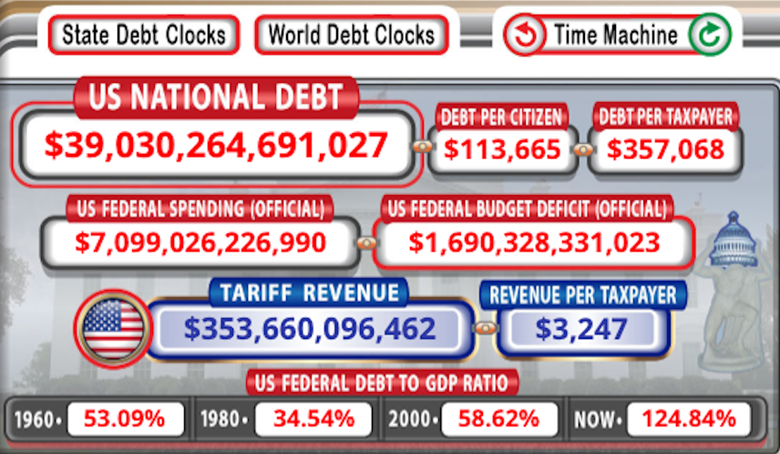

The $39 trillion national debt now exceeds Gross Domestic Product of $31 trillion. The debt is simply the accumulation of prior deficits.

The annual deficit is predicted to grow to $3.1 trillion by 2036, and the US debt is forecast to hit $64 trillion by the same year. In 2030 the debt to GDP ratio will likely reach 120%, beating the previous record of 106% reached right after World War II.

“There’s no sugar-coating it: America’s fiscal health is increasingly dire,” Reuters quoted Jonathan Burks, economic policy director at the centrist Bipartisan Policy Center in Washington. “Our debt is now 100% of GDP, and rather than pumping the brakes, we are accelerating.

“These large deficits are unprecedented for a growing, peacetime economy.”

The U.S.’s debt burden poses an “existential threat to the future of our nation.” Texan Republican Rep. Jodey Arrington, the chairman of the House Budget Committee warned.

Rising yields on government bonds are a red flag on government spending, with investors demanding higher premiums because the perceived risk of the lending has increased.

Trump, Treasury Secretary Scott Bessent and the future Fed Chair, Kevin Warsh, all want low interest rates. But long-term rates will have to rise to attract bondholders. The US can’t afford to lose bond holders, because they finance the US government’s deficit spending.

This, in a short summary, is the Fed’s dilemma: they want to keep interest rates low to goose the economy and when Warsh gets in, to please Trump, and to keep interest payments as low as possible on government debt, but with the prices of oil and other important commodities skyrocketing due to the war in Iran, lower rates will be the wrong policy response to deal with inflation, or worse, stagflation.

Rising interest rates slam the brakes on growth to quell inflation. Before 1965 inflation was at or below 2%, and interest rates were significantly lower. During the late 1960s to early 1970s rates began to rise and by ’73-’74 were as high as 8% due to increased government spending.

The high interest rates (very high compared to the norm) and inflation in 1974 caused a recession. When Paul Volcker became Fed Chairman in August 1979, inflation had accelerated significantly so he enacted a policy of “pre-emptive restraint,” driving the federal funds rate from 11.2% in 1979 to 20% by June 1981 to break the cycle of high inflation.

The US is losing bondholders due to Trump’s “America First” policy (tariffs, isolationism, treating allies like adversaries, etc.) and the only way to attract investors to US Treasuries is for long-term rates to rise. They need to be paid a higher rate to assume the risk of the US defaulting on its debt (more on this below).

The odds seem to be getting getting heavily skewed to rate hikes and stagflation this year, many, me included, think we are currently in a period of stagflation ‘lite.’ Private credit fears are morphing into worries of slowing growth, manufacturing growth slowdown, massive price rises in food and fuel, unrestrained spending and yields climbing could mean full blown stagflation, or worse, recession.

Shunning US debt

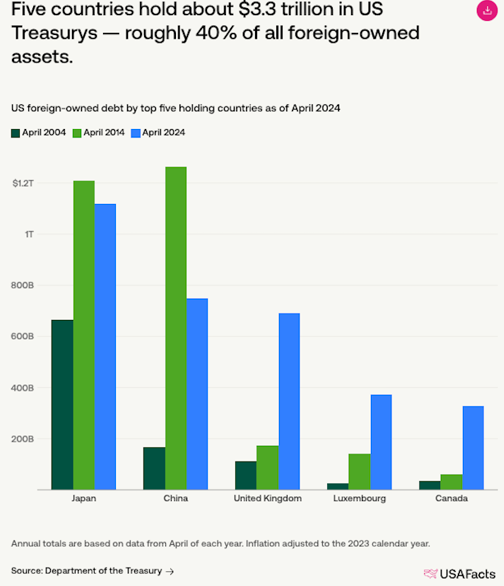

As of April 2024, foreign countries owned approximately $7.9 trillion in Treasuries — or 22.9% of total US debt. The top two debt holders were/are Japan ($1.1 trillion) and China ($749 billion). The next three biggest holders were the UK, Luxembourg and Canada. (USAFacts).

In early February financial regulators in China urged commercial banks to limit purchases of US government bonds and instructed those with high exposure to cut their positions.

The Treasury Department released data in January finding that China’s sovereign holdings of US Treasury debt fell to $682.6 billion, a 1% decrease month on month.

In fact China has been a net seller of Treasuries for nine consecutive months, selling $5.39B in November, according to Barron’s. It adds:

Any ‘quiet quitting’ by Chinese banks would add to growing concern that foreigners are exiting the Treasury market because of worries over the staggering size of U.S. debt. The more the debt supply, the higher the anxiety the U.S. won’t be able to pay back its lenders.

Growing tensions with other countrieson policies proposed by President Donald Trump add to the risk.

Out-of-control spending

Trump’s “One Big Beautiful Bill Act”, which extended the 2017 tax cuts, and slashed outlays on social programs such as Medicaid, will add $4.7 trillion to US deficits over the next 10 years. Tariff revenue will admittedly ease the pain by reducing deficits by about $3 trillion.

Military spending is another large budget item. In early January Trump proposed setting military spending at $1.5 trillion in 2027, citing “troubled and dangerous times.” That’s $500 billion higher than the 2026 military budget.

After adding $500B to the DoD’s 2026 budget, last week, the White House requested another $200 billion for the war in Iran. According to BBC News, the Pentagon told lawmakers the war cost the country $11.3 billion in the first week alone. Tagging this onto the current $1.5 trillion budget means the defense budget next year is $1.7 trillion. Read more on the FY 2026 DoD budget request.

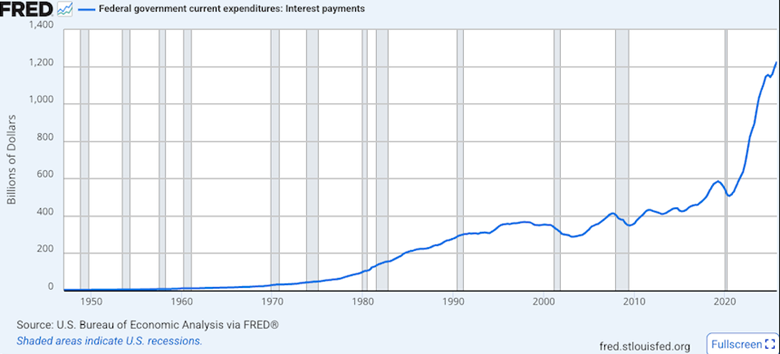

How is all this spending going to affect interest costs? The CBO forecasts the Trump administration’s spending cuts are dwarfed by the growth in net interest costs on the ballooning federal debt, which are set to more than double to $2 trillion by fiscal 2035 from $970 billion in fiscal 2025.

The government is insolvent

In fact the government is effectively insolvent — which is different from bankrupt, but not much better. Wikipedia defines a sovereign default as “the failure or refusal of the government of a sovereign state to pay back its debt in full when due.”

How close is the US to a sovereign default?

In a shattering piece of news that politicians ignored and went unreported in MSM, except for Fortune, the Treasury Department’s consolidated financial statements for fiscal 2025 show $6.06 trillion in total assets against $47.78 trillion in total liabilities as of Sept. 30, 2025 — i.e., liabilities are 8x greater than assets.

Fortune notes the $47 trillion in reported liabilities does not include the unfunded obligations of social insurance programs like Social Security and Medicare, which are disclosed separately.

When these programs are considered, the numbers are even more alarming. Social Security’s 75-year unfunded social insurance obligation — the difference between the present value of projected spending and revenues — reportedly grew by $10.1 trillion in a single year, rising from $78.3 trillion in FY 2024 to $88.4 trillion in FY 2025 — driven primarily by a $6.9 trillion jump in projected Medicare Part B shortfalls and a $2.5 trillion increase for Social Security…

If the $88.4 trillion in 75-year off-balance-sheet obligations were added to the $47.8 trillion in official balance sheet liabilities, total federal obligations would now exceed $136.2 trillion — roughly five times U.S. annual GDP. [or 22.4x the $6 trillion in total assets — Rick]

It gets interesting when Fortune breaks it down to a household level by dividing every number by $100 million or dropping eight zeros.

When that is done, the current US government balance sheet equates to a household that earns $52,446 and spends $73,378, for an annual deficit of $20,932. Total liabilities and unfunded promises amount to $1.361 million, against $60,554 in assets, leaving the household $1.3 million in the hole.

“Uncle Sam, by any accounting standard, is insolvent,” says Fortune.

Another Fortune article published the same day notes it took the United States nearly 200 years to build a debt pile worth $1 trillion. A few decades later, the Treasury is paying that alone just to service the national debt, which recently surpassed $39 trillion.

The CBO calculates the Treasury paid $1.22T in interest on the debt for fiscal 2025, and for FY2026, it has already paid out $520 billion and by 2036 the figure is expected to hit $2.1T.

There are a couple of ways to visualize a trillion dollars. One is that it’s more than the entire FY 2026 Defense Department request of $969.6 billion.

$1 trillion also means that every child in America today carries a $530,000 share of this debt. By keeping the debt and the amount required to service it the same or increasing it, the government is kicking the can down the road for future generations to deal with.

Private credit: risky business

Lastly, we need to talk about private credit and the risk it is posing to the US economy. NPR explains private credit as such:

“Private credit” refers to an opaque but fast-growing corner of the financial world: When private-equity firms and other companies that aren’t banks lend money to businesses, such as software companies and auto lenders. Banks often are more reluctant to lend directly to these businesses, which they see as riskier bets — but they’re still exposed to them, because banks do lend to private credit firms.

The sector, says Morgan Stanley bank, has been growing for years and is now estimated to be a $3 trillion industry. But recent bankruptcies are raising concerns about how carefully private credit firms are vetting the companies they lend to.

“When you see one cockroach, there’s probably more,” JPMorgan Chase CEO Jamie Dimon warned during an October conference call. His bank financed one of the failed companies.

NPR identifies more “cockroaches” that have skittered out of the private-credit woodwork. In February prominent private-credit lender Blue Owl said it would sell off $1.4 billion in assets to give money back to some of its investors. The announcement, says NPR, was intended to reassure Blue Owl’s investors, but instead, it sparked widespread panic about a collapse in private-credit assets…

Now, more investors in several private credit firms are trying to pull their money out of the industry, and the panic is spilling over into the stock market.

Blue Owl’s shares have fallen about 40% since the start of the year. The shares of other big private credit companies, including KKR, Apollo, and Blackstone, are also down by 20% or more.

Part of Wall Street’s concern over private credit is related to AI. Investors are increasingly worried whether their investments in Big Tech, which have powered the stock market for years, will pay off. They’re also worried that AI will render many software companies obsolete. Private credit companies are big lenders to those software companies, explains NPR.

“The great fear is that private credit is going to turn out to have financed a lot of the losers, and then those private credit funds are going to be left with huge losses,” says Harvard law professor Jared Ellias, who co-authored an academic paper about private credit.

In the short term, Wall Street’s private credit selloff is cutting into the retirement accounts of some individual investors, including those who have bought into private credit companies through mutual funds or their 401(k)s.

The even bigger-picture worry for ordinary consumers is that the problems with private credit will ripple throughout the mainstream financial system, sparking some sort of larger meltdown. Investors and financial regulatory experts point to the sector’s lack of transparency as one cause of this concern: Private credit firms are not regulated like banks and do not face the same level of scrutiny or government-mandated disclosures over who or what they lend to.

“We simply don’t know where that money is going (who it is being lent to) and the full extent of the risks being taken,” says Brad Lipton, a former senior adviser at the Consumer Financial Protection Bureau and now the director of corporate power and financial regulation at the Roosevelt Institute, a progressive think tank.

“If investors get spooked about risk and start to pull their money out, we could see a ‘run’ on the companies doing the lending and a crisis,” he adds in an email to NPR.

Lipton and investors also worry about how much the problems with private credit lenders can infect the mainstream banking system. U.S. banks have lent some $300 billion to private credit companies, according to Moody’s.

As more problems with private credit companies have surfaced in recent weeks, bank stocks have sold off.

Conclusion

Households have little room to stomach higher prices, while businesses were already laying-off workers in several countries before the Iran war began.

Barclays estimates in a scenario of oil prices averaging $100 in 2026 – as was the case in 2022 – global growth would be 0.2 percentage points lower, at 2.8% this year, while headline inflation would be 0.7 percentage points higher, at 3.8%, than would otherwise have been the case.

Indeed the war in Iran is really about the ongoing crisis in affordability that started with the covid-19 pandemic in 2020. Due to government-ordered health mandates, supply chains gummed up, causing shortages and higher prices for some items especially food.

This was followed by the inflation surge of 2021-23, when post-pandemic demand for goods outpaced the supply chains that were slowed because of covid, along with the highly inflationary quantitative easing programs launched by central banks to help strapped consumers, many of whom had lost their jobs or had their working hours slashed as businesses struggled to stay afloat.

The 2022 war in Ukraine caused energy prices to spike along with the prices of agricultural commodities exported from the Black Sea region.

US inflation reached a peak of 9.1% in June 2022.

Now we have a fourth inflation event that is piling on top of the three earlier events. Note that the inflation figures are cumulative, thought this is not shown. For example, a 3% increase in a dozen eggs in 2020 is added to a 5% rise from 2021-23, is added to 2022’s inflation of 2%. When the current inflation from the Iran war gets factored into food prices, and it will, you can probably add another 3% to a dozen eggs.

Gasoline prices have increased by 30% in the US and doubled in Europe due to the war.

According to Global News, Canada’s national average for regular gas as of March 19 was sitting just below $1.70, according to CAA, and a month earlier it was closer to $1.28.

People in BC’s Lower Mainland (Vancouver and area) pay the highest gasoline prices in the country, at $2.14 a liter, as of last Monday.

How much inflation can Canadians and Americans stand before they say, “enough is enough”?

Another Global News story that ran on March 23 examined the likely inflationary effects of the war on food.

“The hardest hit items are expected to be meat, dairy, produce and seafood as they have to be transported in refrigerated trucks that require more energy.

“Right now, you may be looking at a double whammy, so on the one side you have energy costs pushing prices higher, but don’t forget with fertilizers with yields being impacted, markets could start to push commodity prices higher mid-year for example,” he said.

Now consider the impacts of higher interest rates on the average homeowner with a mortgage.

In the US, mortgage rates are based on the 10-year Treasury yield which as I mentioned is going up due to the war.

Trump, says the Washington Post, has made housing affordability a centerpiece of his economic agenda, repeatedly emphasizing his desire to see mortgage rates fall.

Instead, US and Canadian mortgage rates are climbing, fast, as the Iran war fans inflation fears and puts pressure on housing markets.

The Washington Post notes mortgage rates briefly topped out at 7% in early 2025, locking many buyers out of the market. Fortunately for them, in late February rates fell below 6% for the first time since September 2022.

On March 19 CBS News reported the 30-year fixed mortgage rate rose to 6.2%, up from 6.1% the previous week.

In Canada, the Financial Post ran a video describing how mortgage rates are already going up due to the war. Although the Bank of Canada has just maintained interest rates at the same level as in October, fixed mortgage rates are rising, including the 5-year, says Shaun Cathcart, director and senior economist, housing data and market analysis at the Canadian Real Estate Association.

Housing, food and fuel prices are all going up. On the micro level, regular wage earners are bearing the brunt of the US government’s ill-conceived attack on Iran.

Those who have some money invested in the stock market are also exposed. The war has caused a correction in global stock markets after months of steady gains. Markets are hyper-sensitive to any sign of the war ending. On Monday Trump extended his deadline for Iran to re-open the Strait of Hormuz. The Dow jumped 1,135 points within minutes while the S&P 500 gained 1.1% for its best day since the war began.

Besides the war and fears about AI being over-hyped, markets are also on edge regarding private credit.

The worry for ordinary consumers is that the problems with private credit will ripple throughout the mainstream financial system, sparking some sort of larger meltdown.

On the macro side, the war has hiked government bond yields, as bond traders price in the effects of higher inflation on long-dated bonds. The specter of stagflation caused by the Iran war has wiped out more than $2.5 trillion from the value of global bonds in March, on track for the biggest monthly loss in more than three years.

The prospect of 1970’s-style stagflation is apparent due to the combination of job losses particularly in manufacturing, stalled growth, and higher inflation emanating from the oil price shock.

The US government is taking in far less money in tax revenue than it spends. Financial statements for fiscal 2025 show $6.06 trillion in total assets against $47.78 trillion in total liabilities as of Sept. 30, 2025 — i.e., liabilities are 8x greater than assets.

The liabilities don’t include unfunded obligations like Social Security and Medicare which amounted to $88.4 trillion in FY 2025.

Meaning the government is basically insolvent.

The CBO calculates the Treasury paid $1.22T in interest on the debt for fiscal 2025, and for FY 2026, it has already paid out $520 billion and by 2036 the figure is expected to hit $2.1T.

The $39 trillion national debt now exceeds Gross Domestic Product of $31 trillion.

“How did you go bankrupt?” “Two ways. Gradually, then suddenly.”

Ernest Hemingway, ‘The Sun Also Rises’

Richard (Rick) Mills

aheadoftheherd.com

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}