Palladium is an unsung green superhero

2019.10.12

Smog from vehicle emissions is estimated to cause a third of the air pollution in the United States. The fact that cars and trucks have tailpipes at street level makes the exhaust fumes even more harmful than industrial smokestacks, because people breathe them directly into their lungs.

Despite greater environmental awareness and transit use, vehicles continue to emit a toxic cloud of four air pollutants, caused by the burning of gasoline in the internal combustion engine. They are:

- Carbon monoxide, expelled when the carbon in fuel doesn’t burn completely. Breathing CO is particularly harmful because it impairs the ability to move oxygen through the body;

- Hydrocarbons, a compound of hydrogen and carbon;

- Nitrous oxides, a product of burnt fuel, created when nitrogen reacts with oxygen;

- Particulate matter, which consists of tiny soot particles that contribute to hazy skies and, when inhaled on a regular basis, can cause lung damage.

Other health problems known to result from air pollution include asthma, heart disease, birth defects and eye irritation.

A study earlier this year found over 30,000 Americans had died from diseases connected to air pollution in 2015, the latest year data was available.

According to Environmental Defense Fund, the transportation sector is responsible for 27% of the country’s greenhouse gas emissions. Passenger vehicles produce four times more greenhouse gases than all of domestic aviation.

In 2018 there were 276 million vehicles registered in the US, 40% of which were cars. In 1990 just under 200 million were registered. The sheer number of people that continue to drive and buy cars has offset pollution-control measures adopted by the auto industry, along with the growing popularity of hybrid-electric vehicles, electric vehicles and renewable fuels – ethanol and biodiesel.

Despite dips during recessions, light vehicle sales per year in the United States have grown from about 15 million in 1978 to 17.2 million in 2018.

The US used to be the world’s biggest contributor of carbon dioxide and other greenhouse gases, but in 2008 China took the ignoble top spot.

Cars being a status symbol, the Middle Kingdom has about 300 million vehicles registered. The Chinese government has taken steps to clamp down on air pollution and diversify into cleaner sectors. The country is a market leader in solar power, electric vehicles and the provision of new nuclear power. Gradually, coal-powered fired power plants are being phased out. While China and India still rely on the cheap fossil fuel, less coal plants are being planned. China permitted just 5 gigawatts (GW) of coal power in 2018 versus 184GW in 2015. India allowed under 3GW of coal in 2018 compared to 39GW in 2010, and has added more solar and wind power capacity than coal over the last two years, states the Guardian.

Yet air pollution in China and India is horrific. A 2018 story in the South China Morning Post reported toxic air hacks around US$38 billion off the Chinese economy each year, due to early deaths and lost food production. Smog-inducing ozone and fine particles are destroying about 20 million tonnes of rice, wheat, maize and soybeans.

Secret weapon

That sounds grim, but there is a secret weapon for fighting tailpipe emissions – catalytic converters, which in 1975 became mandatory for automakers to put into all new cars and trucks. Also known as autocatalysts, these devices reduce noxious emissions, and have been an important reason for internal combustion engines (ICE) polluting up to 90% less than they did in the 1970s, along with the tightening of nation-wide tailpipe emission regulations, led by California.

Enter palladium

Catalytic converters are supplied for both diesel-fueled ICEs and gasoline engines. Both contain a mix of PGEs and other metals including platinum and palladium. A higher percentage of platinum is used in diesel autocatalysts, whereas gasoline-powered autocatalysts employ more palladium.

Palladium (Pd) is one of six platinum group elements (PGE) found in the Periodic Table of the Elements. The others are iridium (Ir), osmium (Os), platinum (Pt), rhodium (Rh) and ruthenium (Ru).

According to the International Platinum Group Metals Association (IPA), one-quarter of all manufactured goods either contain a PGE, or a PGE played a key role in its production. That makes PGEs indispensable for industrial applications.

Autocatalyst demand accounts for three-quarters of the need for palladium. In 2018, out of a total market of 10.1 million ounces, catalytic converters used 8.6Moz, the balance going towards other industrial applications and jewelry.

Diesel phase-out

It used to be that diesel vehicles were sought after because diesel is cheaper than gasoline. Many considered diesels no worse than gas engines for air pollution. In 2016 the diesel car industry was shaken after Volkswagen admitted it had cheated on its emission tests. The “diesel-gate” scandal was made worse amid new reports of the dangers of air pollution.

A 2017 study in the journal ‘Nature’ found that emissions from diesel vehicles which exceeded certification limits were associated with 38,000 premature deaths. The following year, a German court ruled that smog-belching vehicles were to be banned from the centers of Stuttgart and Dusseldorf.

Concerns over air pollution led the EU to set a target of cutting emissions by at least 40% by 2030, from 1990 levels. According to Euractiv, the mayors of 10 European capitals are urging a switch to zero-emissions vehicles within the next 20 years – something the British Columbia government has pledged to happen by 2040 according to a new climate plan.

As of last month, all passenger vehicles sold in Europe must meet “Euro 6d-TEMP” standards, showing they comply with NOx and particulate matter emissions. China will implement its next round of carbon emission rules between 2020 and 2023, involving higher palladium and rhodium loadings, according to Johnson Matthey, a UK-based chemicals company.

Platinum’s loss is palladium’s gain

Diesel engines are therefore being phased out in favor of gas-powered cars that meet stricter emission regs. Testing is reportedly underway in parts of China and the European Union and will be mandatory in those two regions by 2020.

The move away from diesel has hurt not only diesel-car manufacturers but platinum. Less demand for diesel autocatalysts has weighed on platinum prices, which tumbled from about $1,400 an ounce in January 2014, to the current $876/oz. The metal’s market value since 2011 has halved.

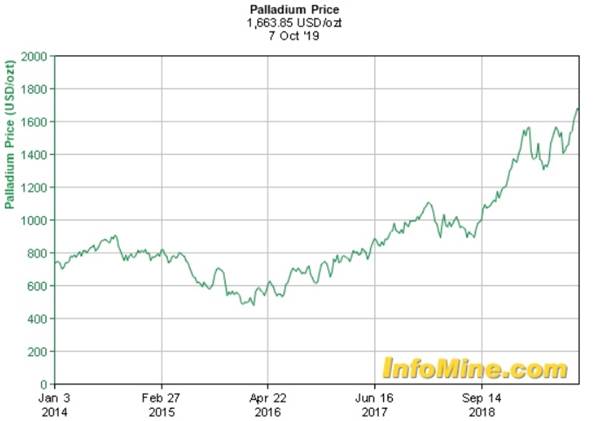

In contrast, palladium has more than doubled over the last three years (+124%) and ran up 18% in 2018. Spot palladium raced past US$1,700 an ounce in September, and traded at $1,663/oz on October 7, far outpacing spot gold, which finished Monday at $1,492/oz.

Despite a global downturn in auto sales in 2018, and the first eight months of this year, palladium prices have stayed buoyant.

Among the factors in its favor are a 3.6% forecasted rise in autocatalyst demand, driven by tighter emissions standards, and increased market-share for gasoline vehicles in Europe.

In the near future, palladium is also likely to see a major surge in demand due to a widespread recall by Fiat Chrysler (FCA). In March FCA issued a voluntary recall of nearly 900,000 gasoline-fueled vehicles, due to defective catalytic converters. The recall is expected to create a need for another 77,000 ounces of palladium, thereby putting upward pressure on prices.

Supply squeeze

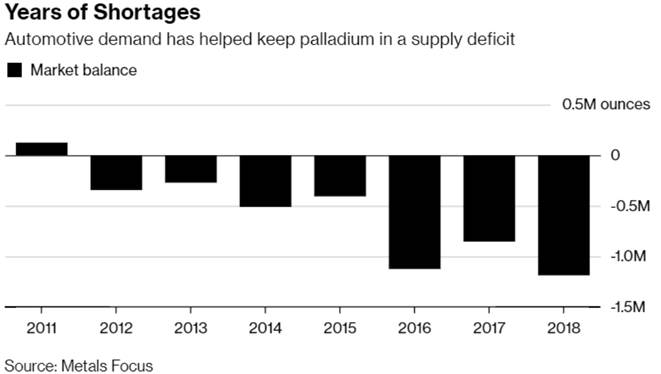

Moreover, currently and for the foreseeable future, palladium is facing constricted supply. The palladium market has been in deficit for years.

An analyst quoted by Reuters said the deficit in 2019 is expected to widen to 1.8Moz, and 1.9Moz in 2020.

The reason has mostly to do with structural problems in South Africa.

About 90% of palladium is mined as a by-product of nickel and copper mining in Russia and platinum mining in South Africa. These two countries dominate the Pd market, with Russia producing 2.84 million ounces in 2018, and South Africa mining 2.59Moz.

South Africa’s platinum mining companies are under constant pressure to contain costs, because their mines are some of the deepest, hottest and most labor-intensive in the world. They also face frequent strikes. In 2014 workers at the country’s three major producers – Lonmin (now Sibanye), Anglo American Platinum and Implats – downed tools for five months demanding that wages be doubled.

In fact, earlier this week Implats took a big step to diversify it’s risk away from those South African mines by allocating capital to North America and acquiring Canada’s North American Palladium Inc. (NAP) for $753 million. NAP is one of two primary palladium producers globally. The other was bought by another South African company 2 years ago, Sibanye. Sibanye bought Stillwater Mining and its palladium mine in the USA.

There are significant infrastructure constraints that the South African’s are dealing with. South Africa has limited processing capacity and water is a constant concern

No substitutes

Some have suggested that platinum could be substituted for palladium if palladium prices continue to trade significantly higher than platinum prices. The problem however is supply. Both metals are looking at long-term structural supply deficits even though investment interest in platinum has piqued recently due to the negative interest rate environment globally (in the first half of 2019, an unprecedented 855,000 ounces of investment demand was driven by 720,000 ounces of Pt that flowed into ETFs).

It has also been said that palladium-heavy catalytic converters perform better than platinum under extreme-conditions emission tests, and that switching to a platinum-based autocatalyst would be too expensive.

Hybrid demand

The palladium supply deficit is due to supply problems set against robust demand not only for palladium in gas-powered vehicles, but hybrids, which despite being cleaner than straight gas models, also require heightening emissions controls.

A small but growing number of consumers are choosing hybrids, which are seen as bridging the gap between ICEs and all-electrics. A 2018 report by JP Morgan Chase & Co. predicts hybrids are expected to grow from 3% of global marketshare to 23% by 2025.

It’s also important to note research showing that hybrid-electric vehicles require more palladium and lithium than traditional gas-powered cars and trucks.

Consolidation

Palladium’s run seems unstoppable, which is putting a renewed focus on mergers and acquisitions in the sector.

In July 2018 Silver Wheaton, a heavy hitter in the precious metals streaming business, acquired the gold and palladium stream from Sibanye Gold’s Stillwater mine in Montana. CEO Randy Smallwood is bullish on Pd due to the expected rise in autocatalyst demand.

Brokerages are also paying attention to the star platinum-group metal and companies that mine it. RBC Dominion Securities has reportedly initiated coverage of North American Palladium, which was just acquired by Implats for + CAD$753 billion. The boards of both companies approved the deal, but it still needs regulatory approval.

In a note, analyst Mark Mihaljevic based an “outperform” rating and $26/sh price on the company’s “positive financial outlook, demonstrated capital returns through regular and special dividends, and unique exposure to palladium,” adding he expects the palladium deficit to continue into 2021.

The Toronto-based company’s Lac des Iles mine northwest of Thunder Bay, Ontario has been in production for over 30 years. It is one of two the only primary palladium mines in the world, the other being Stillwater.

This past August, North American Palladium acquired 51% of the Sunday Lake PGM Project, about 95 kilometers from Lac des Iles. The acquisition was the result of exceeding the mandated two-year expenditure requirement, and completing the requisite cash payments, to option partners Implats and Transition Metals Corp.

Meanwhile Platinum Group Metals, a junior working in South Africa, has put forward a definitive feasibility study (DFS) on its Waterberg PGM Project. The DFS outlines a 45-year decline-accessible polymetallic mine, producing an annual 420,000 ounces of palladium, platinum, gold and rhodium, along with copper and nickel by-products.

The numbers:

- After-tax Net Present Value (“NPV”) of US$ 982 million, at an 8% real discount rate, using spot metal prices as at September 4, 2019 (Incl. US$ 1,546 Pd/oz) (“Spot Prices”).

- After-tax NPV of US$ 333 million, at an 8% real discount rate, using three-year trailing average metal prices up until September 4, 2019 (Incl. US$ 1,055 Pd/oz) (“Three Year Trailing Prices”).

- After-tax Internal Rate of Return (“IRR”) of 20.7% at Spot Prices and 13.3% at Three Year Trailing Prices.

- Estimated project capital of approximately US$ 874 million, including US$ 87 million in contingencies. Peak project funding estimated at US$ 617 million.

Waterberg is a joint venture between Platinum Group Metals, Implats, Japan Oil, Gas and Metals National Corporation (JOGMEC), plus a Japanese trading company and a Black Empowerment partner.

Palladium One (TSX-V:PDM, FRA:7N11, OTC:NKORF)

The key point here, is with M&A shrinking the already-small palladium sector – remember 90% of palladium is produced as a by-product, and pure palladium deposits are very rare – there are limited investment opportunities for getting into a PGE play with a heavy exposure to palladium.

Palladium One’s Lantinen Koillismaa (LK) Project in Finland has the rocks that few copper-nickel-platinum group elements (Cu-Ni-PGE) deposits can boast.

About 2.4 billion years ago, a continental rifting event created the Koillismaa Complex which hosts the LK Project and several other mafic-ultramafic intrusions containing palladium-rich Cu-Ni-PGE sulfide minerals, chromium and iron-titanium-vanadium.

Continental rifting has produced some of the largest Cu-Ni-PGE (copper, nickel, platinum group elements) deposits in the world including the Duluth Complex in Minnesota, Norilsk in Russia, and China’s Jinchuan deposit.

Several of these mafic-ultramafic intrusions occur in Scandinavia, in an area known as the Fennoscandia shield. This is “elephant-deposit country.”

The Fennoscandia shield includes a number of large Cu-Ni-PGE deposits including Pechanga on Russia’s Kola peninsula, Kevitsa, Sakatti, and the Portimo Complex located 90 km northwest of LK.

This summer PDM came out with a maiden resource estimate at Kaukua, the most explored (1 km strike length) mineralized zone on the 25 km basal intrusive contact (2,500-hectare) property.

The first (maiden) NI 43-101-compliant resource on Kaukua places Palladium One in the starting blocks of what should prove to be a very interesting run at developing an open-pit Cu-Ni-PGE mine in a premier mining jurisdiction, Finland.

The main difference between the new and, historic,, 2013 resource is that PDM has defined the resource using reasonable constraint assumptions for economic extraction inside used an conceptual open-pit mine plan, with a cutoff grade of 0.3 grams per tonne palladium, versus the earlier unconstrained 0.1 g/t cutoff grade resource. This “pit-constrained” resource is estimated at:

- 11 million indicated tonnes grading 1.8 grams of palladium-equivalent per tonne (0.81 grams palladium, 0.27 platinum, 0.09 gold, 0.09% nickel and 0.15% copper) for 635,000 oz Pd_Eq.

- 11 million tonnes of inferred grading 1.5 grams per tonne Pd_Eq (0.64 palladium, 0.20 platinum, 0.08 gold, 0.08% nickel and 0.13% copper) for 525,800 oz Pd_Eq.

This leaves Palladium One with a total indicated/ inferred resource of 1.16 million ounces palladium-equivalent, at its LK Project.

About 97% of the earlier indicated resource has been incorporated into the new pit-constrained resource estimate, and 85% of the inferred. Importantly, tThe total pit-constrained resource is currently split evenly between indicated and inferred categories.

Future drilling at Kaukua will target higher-grade PGE zones plus nickel and copper, and upgradeing inferred resources to indicated.

Half a kilometer south of the resource estimate, the Kaukua South zone has outlined a target from only 6 drill holes of between 0.23 and 3 million tonnes grading between 0.7 and one gram palladium-equivalent.

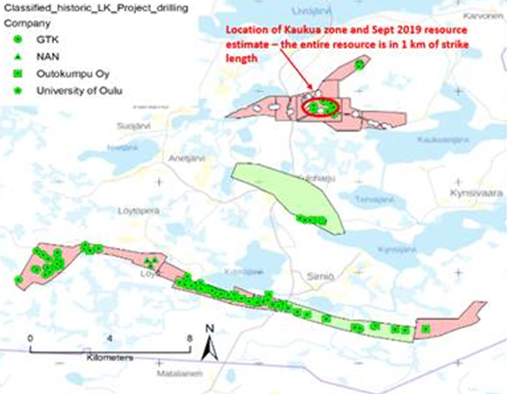

There are nine exploration permit renewal/applications at LK feature three mineralized zones: Kaukua, Murtolampi and Haukiaho, plus 2 reservation applications for an additional 13 km of basal contact.. Historical exploration goes back to the 1960s and was undertaken primarily by Outokumpu, who were exploring for shallow nickel and copper mineralization.

GTK, the Geological Survey of Finland, and Outokumpu punched in a series of widely spaced, shallow (typically ~ 40 meters depth) drill holes that demonstrated anomalous Cu-Ni-PGE mineralization all along the entire 25 km of basal contact. Therein lies the exploration opportunity, the upside.

Only about four kilometers of the 25-km basal contact has been systematically drill-tested, whereas the entire 25 km contact has received widely spaced reconnaissance drilling that demonstrates mineralization. What’s needed is shallow high resolution IP geophysics to vector into the higher sulphide zones, which host higher grades, and start drilling to add tonnes.

At Haukiaho, where historic exploration did not use IP, the 2013 historic resource estimate identified 23.2 million inferred tonnes grading 0.21% copper, 0.14% nickel, 0.13 g/t platinum, 0.31 g/t palladium and 0.10 g/t gold (Au) (0.53 g/t PGE), using a 0.1 g/t Pd cutoff. Current management do not believe adequate work was undertaken at Haukiaho and therefore they did not attempt to prepare a resource estimate for Haukiaho but rather believe IP and more drilling is required prior to preparing a new resource estimate.

The largely unexplored area has about a 10-km strike length. While historical drilling by GTK found multiple anomalous holes mineralized intersections along the entire strike, the higher-grade shoots/ pods were not targeted and no modern induced polarization (IP) survey has been done.

At Murtolampi, a recent surface sample returned 3.106 g/t PGE, 0.78% copper and 0.13% nickel, opening up the possibility of significantly higher-grade the Kaukua mineralization extending north of Kaukua, or even east along strike where no drilling has been conducted. As mentioned the LK Project is in good company, located within Finland’s Fennoscandia shield containing a number of large Cu-Ni-PGE deposits. But it’s also fascinating to compare how PDM ranks among its peers, concerning other open-pit palladium deposits.

The map below shows the extent of historic reconnaissance drilling proven mineralization along about the 38 (25+13) kilometers of basal contact, drilled through shallow, widely-spaced holes. Thus we know the area is mineralized, we just need to conduct IP and poke more drill holes at narrower intervals to better ascertain define where the higher-grade stuff is, that would merit an open pit, or more likely, a series of open pits governed by pit-constrained resources.

We already have a robust resource at Kaukua, with a decent very respectable 3:1 strip waste:ore ratio that in future, would afford a low-cost, open-pit mine.

Now take a look at the table below. Palladium One has shored up 638,000 ounces of indicated Pd_Eq ounces, and 519,000 inferred, at its Kaukua target, for a total of 1.16Moz. The important metric here is the first numbered column, palladium-equivalent tonnes. PDM has the lowest tonnage among its peers in the table – 10,985t measured and indicated – but remember, the company has had to do very little drilling at Kaukua, just 30,000 meters to get to a 1.16 Moz I&I resource and there’s 25km of mineralized trend to find more!

Consider that the Kaukua zone encompasses a very small part (red circle) of the 25 km of basal contact which we know, from historic drilling, is mineralized (ie. anomalous Cu-Ni-PGE mineralization along the entire 25 km of basal contact).

If over a million I&I ounces were generated from just the one target, Kaukua, its fun to entertain/ imagine how many prospective ounces might be sitting there, among the other identified zones at LK, waiting to be outlined and incorporated into new resources.

“This now is a drilling exercise to drill it out and build it up.” CEO Derrick Weyrauch told us at Ahead of the Herd, upon release of the maiden resource at Kaukua.

We agree wholeheartedly.

Conclusion

At AOTH we don’t think it’s a stretch to foresee a lot more PdEq rolled into a total resource at LK, perhaps incorporating three or four zones in open pits. We’re not going to get ahead of ourselves, though. It’s still early days. Geochemical and geophysical studies need to be done on these properties, to pinpoint the mineralization accurately, before they are drilled off.

Success at the drill bit is bound to interest a major, perhaps operating within the Fennoscandia shield, leading to a property purchase or company takeover. Big copper-nickel-PGE deposits are not common, and this looks to be one of them.

PDM investors can look forward to upcoming geochemical/ geophysical studies and a 6,000 to 7,000m drill program. The company plans to drill three major zones not included in the historical resource estimate: Kaukua South, Murtolampi and Haukiaho’s West Torkoaho Zone.

We are confident PDM can execute its exploration plans. The company has a lot going for it, including a robust maiden resource estimate, production of a saleable concentrate, and most importantly in our eyes, massive potential for expanding the resource through further exploration. A previously announced share consolidation cut the number of outstanding shares in half, and an oversubscribed private placement raised $1.352 million.

Palladium One has an excellent management team and board including CEO Weyrauch, VP-Exploration Neil Pettigrew, Lawrence Roulston, former publisher of the acclaimed ‘Resource Opportunities’ newsletter, and Dr. Peter Lightfoot, who literally wrote the book on nickel-copper-precious metal ore deposits.

We know that all metals at LK – palladium, platinum, gold, copper and nickel – are in demand for the foreseeable future, nickel for its use in batteries and stainless steel, copper for its myriad industrial applications, and palladium as a key ingredient of catalytic converters found in gas-powered/ hybrid vehicles and gold for investment and capital preservation purposes.

Finally, we see that PDM’s 2.4 million market cap is grossly undervalued, considering the resource it has just delineated and the huge exploration upside to the project. Based solely of the Kauka resource and excluding any premium for exploration upside or the team, PDM estimates it currently trades at an average 60% discount to its peers, some of which have huge market caps therefore limited potential for stock appreciation. PDM is, in my opinion, the best palladium junior right now for investors wanting to get exposure to the red-hot palladium sector.

Palladium One Mining Inc

TSX-V:PDM, FRA:7N11, OTC:NKORF

Cdn$0.055 2019.10.08

Shares Outstanding 43,702,350m

Market cap Cdn$2.40m

PDM website

*****

Richard (Rick) Mills

subscribe to my free newsletter

Ahead of the Herd Twitter

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.

Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether or not you actually read this Disclaimer, you are deemed to have accepted it.

Any AOTH/Richard Mills document is not, and should not be, construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

AOTH/Richard Mills has based this document on information obtained from sources he believes to be reliable but which has not been independently verified. AOTH/Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of AOTH/Richard Mills only and are subject to change without notice. AOTH/Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission. Furthermore, AOTH/Richard Mills assumes no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information provided within this AOTH/Richard Mills Report.

AOTH/Richard Mills is not a registered broker/financial advisor and does not hold any licenses. These are solely personal thoughts and opinions about finance and/or investments – no information posted on this site is to be considered investment advice or a recommendation to do anything involving finance or money aside from performing your own due diligence and consulting with your personal registered broker/financial advisor. You agree that by reading AOTH/Richard Mills articles, you are acting at your OWN RISK. In no event should AOTH/Richard Mills liable for any direct or indirect trading losses caused by any information contained in AOTH/Richard Mills articles. Information in AOTH/Richard Mills articles is not an offer to sell or a solicitation of an offer to buy any security. AOTH/Richard Mills is not suggesting the transacting of any financial instruments but does suggest consulting your own registered broker/financial advisor with regards to any such transactions

Richard owns shares of Palladium One Mining Inc and PDM is an advertiser on Richards site aheadoftheherd.com

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.