Sulfur chokepoint threatens critical minerals supply – Richard Mills

2026.03.28

Iran’s closure of the Strait of Hormuz has had a profound impact on the prices of oil, natural gas, and other key industrial commodities.

Before the war started, 20 million barrels of oil flowed through the strait daily, or about a fifth of global oil consumption. Significant volumes of aluminum, LNG, distillates such as gasoline, fertilizer, and sulfuric acid used in metal refining, also normally transit the narrow waterway, but are trapped in the Persian Gulf due to the conflict.

This article is about sulfur, used to make sulfuric acid, a critical input for copper and cobalt leaching, as well as nickel and lithium refining.

According to Argus Media, Roughly half of global seaborne sulphur trade transits the strait of Hormuz. With Middle Eastern refinery operations disrupted and shipping largely halted, global sulphur availability has tightened sharply.

As the war grinds on, and nothing suggests a quick end to hostilities, there could be long-lasting effects on battery metals production.

Mining Technology notes that Because sulphur is also a by-product of oil and gas refining, disruption across the Middle East can affect both production and trade availability, creating a secondary supply shock for mining and metals processing.

Copper

Sulfuric acid is a core reagent in the heap leaching and solvent extraction–electrowinning (SX/EW) process used to produce copper from oxide ores and certain secondary sulfide ores. This hydrometallurgical method is essential for the economic recovery of low‑grade deposits and is widely employed across major copper‑producing regions worldwide.

Heap-leach operations supply roughly one-fifth of the world’s refined copper, an amount approximating 4 million tonnes per year. According to the USGS, global refined copper production last year was 29 million tonnes, so heap leaching using sulfuric acid represents almost 14% of the total.

Among the top counties using sulfuric acid for copper leaching are the United States, Chile, Peru, Mexico, the Democratic Republic of Congo (DRC), Zambia, China, Kazakhstan and Australia.

Unsurprisingly, Chile is the top copper producer and the largest user of sulfuric acid for copper heap leaching, with a significant portion of its cathode production derived from solvent extraction and electrowinning (SX/EW), a two-stage hydrometallurgical process used to produce high-purity copper from oxide and low-grade ores.

Heap-leached cathodes account for roughly 40% of Chile’s total copper exports.

Ranked second in heap leach operations, the US uses large-scale heap and dump leaching in Arizona, including at the Morenci, Bagdad and Sierrita mines.

Peru, the third-biggest copper miner, uses hydrometallurgical processing, while Mexico operates several major heap leaching projects including Cananea.

China has invested heavily in heap leaching technologies for low-grade deposits and high-mud copper oxides, while Kazakhstan is active in in-situ leaching (ISL) for copper and uranium.

Australia uses bioleaching and heap leaching, for example at the Girilambone and Mount Leyshon mines.

Central African Copperbelt heavily impacted

Sulfur is used to make sulfuric acid used in African countries to heap leach copper. When these countries run out of sulfur/ acid they will no longer be able to extract copper, causing a shortage.

The Central African Copperbelt (CACB) produces around 6 million tonnes per year of sulfuric acid, much of which is used in the DRC — Africa’s largest copper miner — for high-grade oxide leaching.

Africa is particularly exposed to the war in Iran. According to Argus Media, nearly all sulfur imported by southern African buyers last year originated in the Middle East.

The CACB imports roughly 2Mt/yr of sulfur to make ~6Mt/yr of sulfuric acid for oxide copper leaching. An additional 2.5Mt/yr of acid is generated by regional copper smelters processing concentrates.

Argus notes Higher acid prices directly raise copper production costs in one of the world’s fastest-growing supply regions.

Cobalt

The CACB is also the center of global cobalt production, with the DRC accounting for roughly 70% of global mined cobalt supply. Major producers, says Argus, include Glencore, whose Mutanda and Kamoto operations produced around 40,000t of cobalt in 2024, and China Molybdenum (CMOC), whose Tenke Fungurume and Kisanfu mines together produced more than 55,000t of cobalt last year.

Heap leaching is used to extract and refine cobalt, particularly from lower-grade copper-cobalt oxide ores.

Nickel

Along with copper and cobalt refining, sulfuric acid is a key reagent in high pressure acid leach (HPAL) operations used to produce nickel from laterite ores in Indonesia, now the world’s dominant source of battery-grade nickel, producing more than 50% of global supply. According to Argus, several large Indonesian HPAL projects consume millions of tonnes of sulfur annually to generate acid for leaching operations.

The HPAL plants produce mixed hydroxide precipitate for electric vehicle batteries.

Indonesia is particularly exposed to the war because it imports around 75% of its sulfur requirements from the Middle East. Argus notes that If sulphur availability tightens materially, nickel processing costs could rise sharply, weakening the economics of HPAL projects and slowing the pace of supply growth. In turn, this could affect the affordability and availability of nickel units needed for the EV battery market.

Lithium

Sulphuric acid is also widely used in lithium extraction and processing. Hard rock spodumene concentrate is typically converted into lithium chemicals using sulphuric acid roasting, while several emerging direct lithium extraction and brine conversion routes also depend on large volumes of sulphuric acid. A sustained rise in sulphur prices therefore risks feeding directly into global battery metal production costs.

Lithium refining is an energy and reagent-intensive process. Elevated LNG and power costs in Asia, combined with rising sulphur and sulphuric acid prices used in the conversion of spodumene into lithium chemicals, could significantly increase operating costs for converters…

China accounts for roughly 80pc of global lithium chemical refining capacity, meaning that any sustained pressure on Chinese converters would have disproportionate consequences for global lithium supply. (Argus Media)Copper shortage.

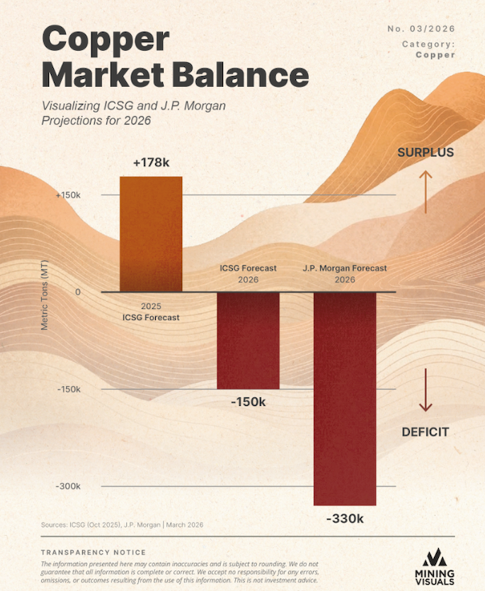

For years, analysts modeling the global copper market were comforted by the expectation of a reliable buffer of surplus supply. But as our latest data visualization reveals, market balance forecasts show a sharp shift from a projected surplus to a deficit in 2026. The International Copper Study Group (ICSG) has officially abandoned its projected surplus for 2025, now forecasting a 150,000-metric-ton deficit for 2026—pointing to the market’s first structural shortage since 2009. Wall Street is bracing for an even harsher reality. J.P. Morgan’s models push the anticipated shortfall to a staggering 330,000 metric tons. Driven by an unprecedented surge in hyperscale AI infrastructure and cascading mine closures, this massive shift in the outlook from green to red has already pushed current prices to historic highs, signaling that the era of abundant copper may be definitively over. (Mining Visuals)

While the copper market was roughly balanced in 2025, meaning that refined production met consumption, mine supply was severely disrupted and will likely create a deficit in 2026, states the International Institute for Strategic Studies (IISS).

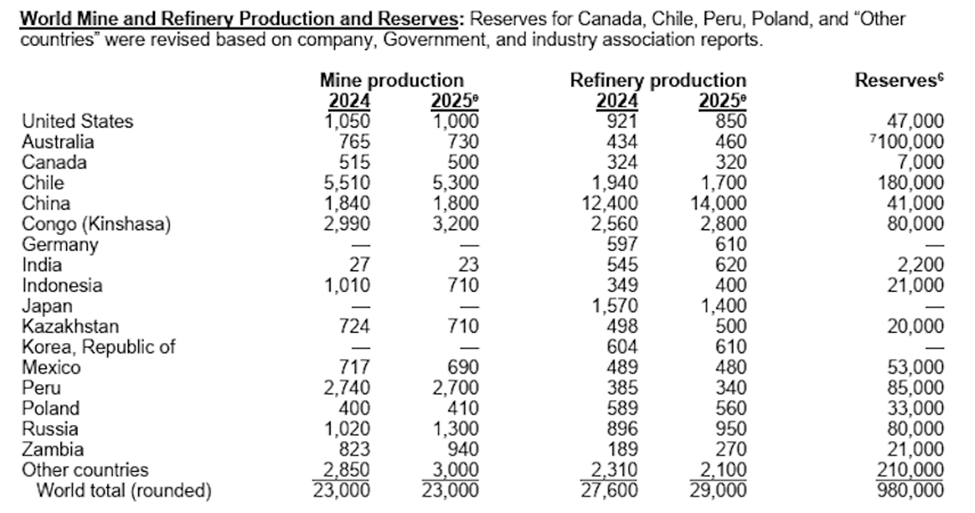

A significant long-term deficit is projected, potentially exceeding 6 million tonnes annually by the early 2030s. Total output from copper mines in 2025 was 23 million tonnes, according to the USGS.

Why we’re running out of copper — Richard Mills

According to the International Energy Agency (IEA), key factors driving the supply crunch include:

- Declining Ore Grades: Global copper ore grades have fallen by 40% since 1991, requiring mining companies to process more ore to produce the same amount of copper, increasing costs and energy usage.

- Operational Disruptions (2025–2026): Major mines, including Grasberg (Indonesia) and Kamoa-Kakula (DRC), experienced significant disruptions (mudslides, flooding, and seismic issues) in 2025.

- Limited New Projects: The pipeline for new mines is weak, with only 5% of all copper deposits discovered in the last 35 years appearing in the last decade.

- Long Lead Times: Developing new copper mines takes between 15 and 30 years from discovery to production, making it difficult to increase supply quickly.

- Smelter Bottlenecks: A rapid expansion in Chinese smelting capacity has caused a shortage of raw concentrate, driving Treatment/Refining Charges (TC/RCs) to negative levels in 2024–2025, forcing potential production cuts by smelters.

We can also add missed production guidance to this list. Anglo American in early February posted a 10% drop in copper production in 2025 and cut its 2026 guidance. The global miner now expects this year’s copper output to be within a range of 700,000 to 760,000 tons, from a previous forecast of 760,000-820,000 tons, partly due to lower production from its co-owned Collahuasi mine in Chile, Reuters said.

Rising demand drivers include:

- Artificial Intelligence (AI) Infrastructure: Data centers are driving huge power demands, requiring significant copper for new infrastructure and power transmission.

- Energy Transition: Electrification and renewable energy systems are expected to triple copper demand by 2045, according to BloombergNEF.

- Defense & Industrial Usage: Growing defense spending and grid upgrades are creating robust demand, with global consumption rising to around 26-28 million tonnes in 2024/2025.

The picture emerging is a world that needs a lot more copper than it currently produces. Supply disruptions at several large copper mines have pushed the market into deficit this year. Copper supply is expected to fall 10Mt short of demand by 2040, putting at risk industries such as artificial intelligence, defense spending and electrification — all of which are driving demand higher. Wood Mackenzie estimates that 8Mtpa of new mining capacity, in addition to 3.5Mt of copper scrap, will be required to balance the market in 2035. The cost to deliver this supply growth is likely to exceed $210 billion, compared to around $76 billion invested in copper mining over the past six years. But copper is getting more expensive to dig out of the ground. Ore grades are declining, and water needed for mining is getting scarce, especially in Chile, which is in a multi-year drought. Energy and labor costs are also pushing expenditures higher. Governments are starting to realize the problems in the copper industry and have made copper a critical metal. The United States and are countries have begun stockpiling copper, signaling a fear of running out of the electrification metal. US stockpiling has further tightened an already tight copper market.Governments are investing in copper mines to gain some control over the copper supply chain, which is vulnerable to disruptions.

Companies are merging to control what copper is left, taking the path of least resistance by shifting reserves from one balance sheet to another rather than taking the time and allocating funds to discovering new copper deposits. It takes decades to develop a new copper mine from discovery to production in regulation-heavy jurisdictions like Canada and the United States. This must change, or the copper supply deficit will only get worse.

I’ve been predicting it for years, but the scramble for copper is finally here. And it’s just getting started.

Copper’s military uses

Since we’re in the middle of a war, copper is considered a critical mineral for national defense and modern warfare. Discovery Alert notes, Copper is considered a traditional and indispensable “military metal” due to its high electrical conductivity, thermal conductivity, corrosion resistance, and malleability, making it vital for modern warfare, defense infrastructure, and munitions production. It is essential for manufacturing weaponry, communication systems, vehicles, and ammunition.

An AI Overview gives the following applications:

- Weapon Systems: Copper is essential for guidance systems, surveillance technology, and electrical systems in modern weapons.

- Missiles and Munitions: It is used extensively in conventional ammunition and missile technology.

- Armor and Vehicles: Emerging technology includes ultra-tough copper alloys that are stronger than steel and can withstand extreme temperatures of 1500°F.

- Naval Vessels: Cupronickel alloys are critical for piping and heat exchangers in marine environments, thanks to their high corrosion resistance.

The Copper Development Association adds:

Copper and copper alloys are ubiquitous in aerospace and defense applications, including high-pressure valves, pumps, shafts, bolting, flanges, couplings, steering mechanisms and turret gears in tanks, aircraft undercarriage components, bearings and bushings for landing gears and cargo doors, ammunition casings and more.

When copper is combined with beryllium, extraordinary alloys are created with unparalleled strength, non-magnetic properties, and a lighter weight than aluminum. Beryllium copper alloys have high strength, up to 1,400 MPa (200,000 psi), surpassing steel, and serving to enhance the speed and performance of fighter jets. Its efficient heat conduction further supports essential defense applications, including surveillance technology. For corrosive marine environments, cupronickel alloys are the material of choice, ensuring the efficiency and longevity of naval vessels. The single-phase microstructure of these alloys enable remarkable properties, and their low corrosion rate in seawater is a critical factor for naval operations.

Conclusion

The threat to refined copper supply due to the very real possibility of running out of sulfuric acid, feeds into the copper deficit narrative that I’ve been warning my readers about.

If sulfur and sulfuric acid fail to make it to the refineries, we are talking about 4 million tonnes/yr stripped from global copper supply, around 14% of a refined copper market of 29 million tonnes. That’s huge.

Mining Technology notes the impact of the Hormuz Strait closure is more significant in refining and processing than in mine production alone:

Although the military confrontation is centred on Iran, Israel, and several Gulf countries, its implications for mining are being transmitted through higher energy prices, shipping disruption, rising insurance costs, and greater uncertainty across commodity supply chains. For the mining industry, the main concern is not only the risk of direct production loss in the region, but also the broader effect on processing costs, raw material flows, and global trade routes…

Any disruption to flows through the Strait affects not only crude oil and petroleum products, but also the movement of industrial inputs and refined metals. As security risks in the corridor rise, mining companies are facing higher fuel bills, longer shipping times, tighter freight availability, and elevated marine insurance premiums. These pressures are feeding into operating costs across both upstream mining and downstream refining activities, particularly in commodity chains that are highly dependent on imported inputs or seaborne logistics.

Codelco, the world’s largest copper company, expects disruptions from the Middle East war to lift its production costs by about 5%. According to a Bloomberg story,

Higher diesel prices, more expensive supplies and the Chilean government’s proposed suspension of a fuel tax credit would together add roughly 10 cents per pound to Codelco’s cash costs, Chief Financial Officer Alejandro Sanhueza told reporters in Santiago on Friday. Currently, the cost stands at about $2 a pound.

“Copper has shown remarkable resilience despite the broader volatility across commodities,” states Tavi Costa, a former partner with Crescat Capital and now founder and CEO of Azuria Capital LLC.

“The metal precisely retested its breakout level, which now appears to be holding as strong support.

In my view, this sets the stage for the next move higher.

Both the technical and fundamental backdrop remain incredibly constructive.”

The global copper market is experiencing a significant, structural tightening of supply, with a projected deficit of 150,000 to 600,000 tonnes in 2026. This anticipated shortfall follows a period of intense disruptions in 2025, which saw mine supply growth slow dramatically, reversing previous projections of a surplus. The long-term outlook is even more strained, with a potential 30% supply deficit by 2035 driven by surging demand for artificial intelligence (AI), grid electrification and renewable energy.

The associated increase in data centers is causing an explosion in electricity demand, requiring substantial copper for new infrastructure and power transmission.

This all boils down to everything driving the world’s economies needs more copper, in the face of persistent constraints on mine supply.

The Iran war is only going to exacerbate the copper supply deficit by reducing smelter output or, depending on how long the war lasts and how much sulfur/ acid is preventing from getting to where it needs to go, could even result in smelters shutting down.

Why Canada and the United States need more smelters and refineries — Richard Mills

It’s also a reminder of the necessity of having localized mineral supply chains rather than relying on imports.

It makes little sense to dig up metals and export the concentrate offshore for processing. Security of supply implies a complete supply chain that begins with mining the minerals and ends with refining the metals into finished products.

Richard (Rick) Mills

aheadoftheherd.com

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.

{kind=link}