Lomiko puts out strong PEA as demand for battery-grade graphite expected to challenge supply

2021.07.31

Lomiko Metals (TSXV:LMR, OTC:LMRMF, Frankfurt:DH8C) is exploring for lithium and graphite in the Canadian province of Quebec.

The mining-friendly jurisdiction placed in the top 10 of the Fraser Institute Annual Survey of Mining Companies 2020, for investment attractiveness. Also last year, the province unveiled the Quebec Plan for the Development of Strategic Minerals 2020-25, signaling its intention to transition to a lower-carbon economy. Quebec has also established a list of 22 minerals considered critical and strategic, among them lithium, graphite, nickel, cobalt and rare earths.

Lomiko’s flagship project is the La Loutre flake graphite property, located 117 km northwest of Montreal, and 53 km east of Imerys Carbon and Graphite’s Lac des Iles mine.

Originally explored for base and precious metals, historical reports showed graphite to be present on the property in quartzite and biotite gneiss, and in shear zones where the graphite content ranges from 1-10% on surface including visible flakes. A recent grab sampling and mapping program confirmed a graphite-bearing structure of approximately 7 km by 1 km, with results up to 22% graphite in multiple parallel zones 30m to 50m wide. Another 2 km x 1 km area consisting of multiple parallel zones, 20m to 50m, includes up to 18% graphite.

The property already has a resource of 18.4 million tonnes carbon flake graphite (Cg) grading 3.19% in the indicated category, and 16.7Mt @ 3.75% inferred. Using a 3% cut-off grade, the resource amounts to 4.1Mt @ 6.5% Cg indicated, and 6.2Mt @ 6.1% inferred.

A preliminary economic assessment released by Lomiko this week shows robust economics for the project.

Completed by Ausenco Engineering and compliant with National Instrument (NI) 43-101 standards, the report uses a measured and indicated resource of 1.04 million tonnes of graphite at a 1.5% Cg cut-off grade as the base case scenario.

The PEA supports an open-pit mine with average annual graphite concentrate production of 108,000 tonnes for the first eight years, and a life of mine average yearly production rate of 97,400t, for 14.7 years.

Cash costs are pegged at US$386 per tonne of graphite concentrate and all-in sustaining costs (AISC) are $406/t.

Up-front costs (capex) are a reasonably low C$236.1 million, which includes mine pre-production, processing and infrastructure (roads, power line construction, co-disposal tailings facility, ancillary buildings and water management).

According to Lomiko, the La Loutre project has the potential to become a major North American graphite producer, with an after-tax net present value (NPV) of $186 million and a 21.5% internal rate of return (IRR).

Small-cap investors reacted favorably to the PEA, bidding up the stock 16.6% on Friday, to close at C$0.14/sh.

One of the most important aspects for investors to recognize about La Loutre, is its exploration upside.

The PEA indicates the property has the geological potential to extend the mine life beyond the initial 14.7 years, as well as the opportunity to expand the scale of production by increasing the mineral resource through ongoing exploration and drilling.

“La Loutre has shown it has the potential to become a highly profitable graphite mine in one of the most prolific producing regions in Canada, said Lomiko’s President and CEO A. Paul Gill, in the July 29 news release. He added:

“With further drill programs, we will continue to add to and upgrade resources as we seek to move the project forward towards production.”

With a strong treasury to support next steps (in May Lomiko closed a C$1.1M financing @ $0.17), the company aims to initiate a Preliminary Feasibility Study (PFS) and environmental impact studies as it continues to explore and reveal the geological potential of La Loutre.

Critical minerals cooperation

The release of the PEA comes as governments have begun showing their support for critical minerals projects that meet environmental, social and governance (ESG) criteria.

For example, the United States and Canada are planning to execute a home-grown strategy to explore for and mine critical minerals, like graphite, in North America.

In January 2020, the two governments announced the Joint Action Plan on Critical Mineral Collaboration. The agreement would increase production and establish supply chains for numerous critical minerals the US is dependent on for imports.

Ottawa recently released a critical minerals list like the list of 35 published by the US in 2017; the 31-metal catalogue includes cobalt, graphite, lithium and rare earths.

According to Gill,

“The development of Canada-USA and Canada-EU critical minerals collaboration agreements gives access for graphite products in these markets. There is a focus on projects with environmental, social and governance (ESG) acceptability which Lomiko has also adopted. The strict criteria for the report should result in competitively-priced graphite for customers in the North America and European markets.

“These recent agreements between Canada and the USA and Canada and Europe have identified graphite as a critical element that will be part of a new supply chain. Lomiko is ready to maximize La Loutre’s value by advancing the studies to further refine and de-risk the project.”

The company says it looks forward to working with its partners in the MRC of Papineau region including the Lac-des-Plages and the Duhamel municipalities, as well as the surrounding First Nations communities. Lomiko will also continue to work closely with the Quebec and federal governments to advance the La Loutre project.

Graphite market update

Lomiko Metals is developing La Loutre during a transformative time in the graphite space.

The demand for “green” metals is pinned on bets that more aggressive climate pledges will accelerate the proliferation of solar panels, wind turbines and electric cars. Beyond electrification and decarbonization, the need is being driven by something more immediate — a worldwide economic recovery from the pandemic.

As countries continue to vaccinate their populations, and infections drop, economies are re-opening, stoking demand for more cars, electronics, and infrastructure, primarily.

On top of surging demand for metals needed to feed so-called “green infrastructure” programs, we have current and emerging structural deficits for several metals, that will keep prices buoyant for the foreseeable future.

Over the past year, tight supply is reflected in the rising prices of copper, nickel, zinc, and lead, for example.

In fact, battery/ energy metals demand is moving at such a break-neck speed, that supply will be extremely challenged to keep up. Without a major push by producers and junior miners to find and develop new mineral deposits, glaring supply deficits are going to beset the industry for some time.

According to a recent report by UBS, a deficit in nickel will come into play this year, for rare earths in 2022, for cobalt in 2023, and in 2024, for lithium and natural graphite.

Moreover, the Swiss investment bank predicts large deficits by 2030 for each of these metals: 170,000 tonnes for cobalt, equal to 42% of the cobalt market; 10.9 million tonnes of copper (about half of current global mined production), representing 31% of the market; 2.1Mt for lithium (50% market share); 3.7Mt for natural graphite and 2.2Mt for nickel (both 37%); and 48,000 tonnes for rare earths, equivalent to 47% of the market.

Graphite is one of the most interesting metal markets to watch, because, like copper, the “EV revolution” doesn’t happen without it.

There are no substitutes for lithium and graphite; these critical metals are expected to remain the foundation of all lithium-ion EV battery chemistries for the foreseeable future.

Lithium is in the battery cathode and graphite, or more precisely, spherical graphite, is in the anode.

A lithium-ion battery should actually be called a “graphite-ion” battery, since it contains about 20 times more graphite than lithium.

Graphite has long been used in the aviation, automotive, sports, steel and plastic industries, as well as in the manufacture of bearings and lubricants. Graphite, an excellent conductor of heat and electricity, is corrosion- and heat-resistant, strong and light.

The steel industry has traditionally taken the majority of the world’s graphite production, but this is beginning to change. Scotland-based commodities consultancy Wood Mackenzie forecasts a rapid acceleration of demand for the energy storage/ battery sector, rising from just 165,000 tonnes in 2018 to almost 1 million tonnes by 2030. Benchmark Mineral Intelligence estimates that the amount of graphite needed for the anode material in lithium-ion batteries will rocket to 1.75 million metric tons by 2028, a nine-fold increase over 2017 levels.

In 2020 the entire mined production of graphite was 1.1 million tonnes, suggesting a coming supply deficit if more graphite deposits aren’t developed into mines. Remember, in addition to supplying the nearly 1 million tonnes of graphite expected to be demanded by lithium-ion batteries within the next decade, the rest of graphite’s uses aren’t going away and will need to be supplied as well.

A recently published research report found that the global lithium-ion battery market is expected to grow at a CAGR of 15% from 2020 to 2026. Roskill, a critical minerals intelligence provider, last year found that demand for graphite in batteries could grow by 19% per year by 2029.

Batteries for electric vehicles represent a large chunk of future energy storage demand. Wood Mackenzie has crunched the numbers, stating that EV sales are expected to top a combined 7 million a year in the three main markets of China, Europe and the US by 2025. As sticker prices fall, the firm predicts sales will double to a combined 15 million a year by 2030.

Projecting further out, Wood Mackenzie says by 2047 battery electric vehicles, plug-in hybrids and fuel cell vehicles will combine to eclipse sales of internal combustion engine (ICE) light duty vehicles. By 2050, Woodmac expects EV sales to reach 62 million units per year, and there to be a global EV stock of 700 million. That compares to an estimated billion-plus passenger cars on global roads today.

The White House reportedly told US automakers it wants them to back a voluntary pledge to make at least 40% of new vehicles electric by 2030.

We can already see the amount of graphite demanded by batteries is growing rapidly. According to MINING.com’s EV Metal Index, In April 2021, just over 14,000 tonnes of synthetic and natural graphite were deployed globally in batteries of all newly-sold passenger EVs combined, a 233% jump over the same month last year.

Will there be enough mined graphite to meet the demand? We can answer this question in a couple of ways. If we take Woodmac’s prediction of 15 million EVs by 2030, the amount of graphite demanded is found by simply multiplying 15 million EVs X an average 70 kg/ 154 lb of graphite per EV (85 kg/ 187 lb is the amount of graphite in a Tesla Model S battery). Already this is approaching the world’s current mined graphite production of 1.1Mt and we haven’t included the graphite tonnage needed for consumer/ military electronics, two-wheeled electric vehicles, buses, trucks, electric planes and trains. Wood Mackenzie predicts that annual commercial EV sales are expected to hit 3 million by 2025 and triple to 9 million by 2030. Batteries for electric vans, trucks, planes, trains and buses are obviously far larger than passenger vehicles and require more graphite.

The 1.150 million tonnes of graphite demanded for 15 million EVs also leaves out all the graphite that will be needed for graphite for vanadium redox batteries used for large-scale energy storage. These batteries, which are the size of a house, will require “copious quantities of graphite felt,” states a 2016 article by The Northern Miner.

Graphite supply is going to be a major obstacle to the kind of EV market penetration Wood Mackenzie and other are predicting.

Tesla produced just shy of 510,000 vehicles in 2020, a 39.5 percent increase on the company’s stellar 2019, which had been driven to a large extent by Model 3 production and sales figures. This is only one company. What about all the other EV manufacturers needing to install batteries containing graphite?

By 2025 global installed battery production capacity is expected to increase by over 300%.

In the United States, there are a number of battery plants in the works to join Tesla, whose first gigafactory in Nevada started production of battery cells in 2017. The company has a plant in Buffalo, New York, and plans to open a third (US plant) in Texas by the end of this year. Tesla also has a “pilot line” at its facility in Fremont, California, for R&D technologies.

In 2020 General Motors announced plans to install its first battery cell factory in Ohio, a project called Ultium Cells launched with its Korean partner LG Chem. The latter opened a plant in Holland, Michigan in 2013.

Another South Korean company, SK Innovation, is planning on opening the first of two battery plants in Georgia this year; the company is a supplier to Volkswagen and Ford.

The latter along with American auto icon GM have big plans to electrify their fleets. Ford announced plans to boost spending on electrification by more than a third, and aims to have 40% of its global volume electric by 2030, which translates to more than 1.5 million EVs based on last year’s sales.

GM reportedly aspires to halt all sales of gas-powered vehicles by 2035, with plans to invest $27 billion in electric and autonomous vehicles over the next five years.

There are currently 11 EV start-ups racing to catch up with market leader Tesla, fueled by money from Wall Street. They include Rivian out of Irvine, California, Lucid Motors based in Newark, CA, Lordstown Motors from Ohio, Nikola Corp (Phoenix), Fisker (Los Angeles), Faraday & Future (Los Angeles), Canoo (Torrance), NIO, Li Auto and XPing from China, and Arrival, based in London.

Where is all of this extra graphite going to come from?

As important and valuable as graphite is, the US currently has no domestic production of the mineral, which means all the graphite it uses to build EV batteries come via imports, and that amount is growing year by year – about 40,000 tonnes of graphite material were imported in 2020.

Meanwhile, its biggest rival China is by far the world’s biggest producer, with 650,000 tonnes of mined graphite recorded in 2020, representing nearly 60% of the world’s total. After China, the next leading graphite producers are Mozambique, Brazil, Madagascar and India.

Only 12,000 tonnes a year is being mined from two existing facilities in Canada, leaving plenty of opportunity for newcomers.

Conclusion

The need for lithium batteries not only for EVs, but energy storage, handheld tools like drills, vacuums, cell phones and laptops, is almost certain to outstrip supply. The lithium-ion battery manufacturing capacity currently under construction would require flake graphite production to double by 2025.

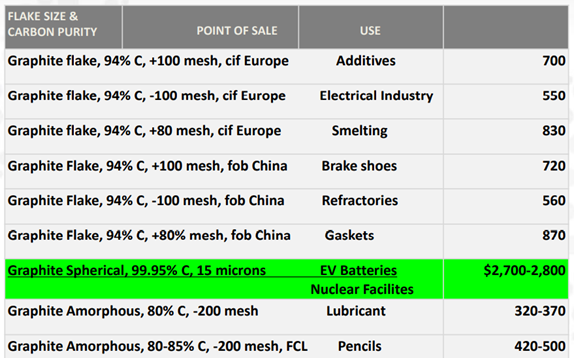

Only flake graphite, upgradeable to 95.95% purity, can be used as anode material in a lithium-ion battery.

According to MINING.com’s EV Metal Index, graphite prices have held steady above $700 a tonne in 2021, after hitting a low of $644/t last September.

The bullish market forces that are swirling in preparation for what many are calling the next commodities super-cycle, are excellent news for companies on the hunt for minerals that support the electrification of the transportation system, the decarbonization of energy sources, and new spending on infrastructure, both green and traditional/ blacktop.

Lomiko Metals just released a PEA on its La Loutre graphite project in Quebec, a major milestone in the path to production. The market rewarded Lomiko with a 16% bump in the share price and I expect continued momentum as Lomiko drills off more resources, extends the mine life and makes the economics even more attractive.

Lomiko Metals Inc.

TSXV:LMR, OTC:LMRMF, Frankfurt:DH8C

Cdn$0.14, 2021.07.30

Shares Outstanding 76.5m

Market cap Cdn$30.1m

LMR website

Richard (Rick) Mills

aheadoftheherd.com

subscribe to my free newsletter

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.

Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.

Any AOTH/Richard Mills document is not, and should not be, construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

AOTH/Richard Mills has based this document on information obtained from sources he believes to be reliable, but which has not been independently verified.

AOTH/Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness.

Expressions of opinion are those of AOTH/Richard Mills only and are subject to change without notice.

AOTH/Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission.

Furthermore, AOTH/Richard Mills assumes no liability for any direct or indirect loss or damage for lost profit, which you may incur as a result of the use and existence of the information provided within this AOTH/Richard Mills Report.

You agree that by reading AOTH/Richard Mills articles, you are acting at your OWN RISK. In no event should AOTH/Richard Mills liable for any direct or indirect trading losses caused by any information contained in AOTH/Richard Mills articles. Information in AOTH/Richard Mills articles is not an offer to sell or a solicitation of an offer to buy any security. AOTH/Richard Mills is not suggesting the transacting of any financial instruments.

Our publications are not a recommendation to buy or sell a security – no information posted on this site is to be considered investment advice or a recommendation to do anything involving finance or money aside from performing your own due diligence and consulting with your personal registered broker/financial advisor.

AOTH/Richard Mills recommends that before investing in any securities, you consult with a professional financial planner or advisor, and that you should conduct a complete and independent investigation before investing in any security after prudent consideration of all pertinent risks. Ahead of the Herd is not a registered broker, dealer, analyst, or advisor. We hold no investment licenses and may not sell, offer to sell, or offer to buy any security.

Richard does not own shares of Lomiko Metals (TSX.V:LMR). LMR is a paid advertiser on his site aheadoftheherd.com

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.