Graphite One’s Graphite Creek deposit a generational graphite resource USGS says among largest in the world – Richard Mills

2023.03.11

Modeling by the International Agency shows that global EV adoption must surpass 60% of total cars by 2030 to achieve net zero emissions by 2050.

While accomplishing this goal will be a huge challenge, we’ve already proven that we don’t have enough copper for more than a 30% penetration, Project Syndicate argues that a faster transition is both feasible and affordable:

Copper, the most important metal we’re running short of

Many EV options are already available in major markets, and new ones are steadily being added to manufacturers’ product lines. Growing investment shows that automakers are serious about accelerating the shift to EVs. Prices will keep falling with improvements in battery technology and economies of scale. EVs in China are already cheaper than internal-combustion cars over the life of the vehicle (after accounting for the fuel and maintenance savings that EVs offer). These developments have pushed EV sales past a tipping point in China and 18 other countries, including the United States. Major markets have entered a phase of mass EV adoption in which preferences will shift surprisingly quickly.

Quick transition needed

Note there are risks in going too slowly in making the transition from gas-powered vehicles to electrics, especially for the United States, which is so dependent on minerals imported from China.

At the CERAWeek energy conference in Houston, Biden administration officials warned leaders of the US clean energy transition to decarbonize quickly and keep the supply chain out of China’s control.

Key to the strategy is finding a way to ensure domestic supply without sparking a trade war with China.

“It’s just clear, to say it directly, that China has too much of a chokehold on critical minerals, on critical processing and upstream technologies, and solar,” White House energy adviser John Podesta told the conference, via Reuters. “We let that go. That was a mistake. We need to get it back.”

Energy executives agreed on the value of a diverse and secure supply chain, but some said good relations with China, where products are often cheaper, need to be maintained by Washington.

Tensions with Beijing have been rising over issues ranging from Chinese spy balloons drifting over US territory, a potential war with Taiwan and China’s position on the war in Ukraine.

Richard Adkerson, chief executive of US-based copper miner Freeport-McMoRan, said the risk of a trade war with China is hanging over the industry right now, and is making companies reluctant to invest in long-term projects.

More broadly, looming shortages of key electrification metals like copper and graphite, threaten the global energy transition.

According to Bloomberg New Energy Finance (NEF), getting to net zero will require almost $10 trillion of new metals between now and 2050, with annual demand peaking at around $450 billion in the mid-2030s. An estimated $3.4 trillion worth of copper is thought to be needed.

Graphite importance

Conspicuously absent in the BloombergNEF chart is graphite, a necessary part of lithium-ion batteries, without which there will be no clean energy transition. EV batteries consist of anodes and cathodes; graphite is the material in the anode. There are no known substitutes.

It is also the largest component in batteries by weight, constituting 45% or more of the cell. It may surprise readers to learn that there is nearly four times more graphite feedstock consumed in each lithium-ion cell than lithium, and nine times more than cobalt.

Graphite is included on a list of 23 critical metals the US Geological Survey has deemed critical to the national economy and national security.

According to the USGS, the battery end-use market for graphite has grown by 250% since 2018.

It’s thought that battery demand could gobble up well over 1.6 million tonnes of flake graphite per year (out of 2022 mine supply of 1.3Mt).

Remember, the mining industry still needs to supply other graphite end-users. Currently, the automotive and steel industries are the largest consumers of graphite, with demand across both rising at 5% per annum.

Benchmark Mineral Intelligence has said 97 average-sized graphite mines need to come online by 2035 to meet demand!

China’s dominance

When it comes to graphite, China is by far the biggest producer with nearly 80% of the world’s production. Due to weak environmental standards and low costs, China also controls almost all graphite processing. With no current graphite production of its own, the US is 100% dependent on China for its battery-grade graphite.

Consider: No matter where a battery is made, much of the graphite originates in China, and from there it either gets processed in China, or it moves to South Korea or Japan, for manufacturing by LG or Panasonic, for example.

China’s domination of the graphite space means that developing a North American supply chain from scratch will not be easy.

Graphite One Inc. (GPH, OTCQX:GPHOF)

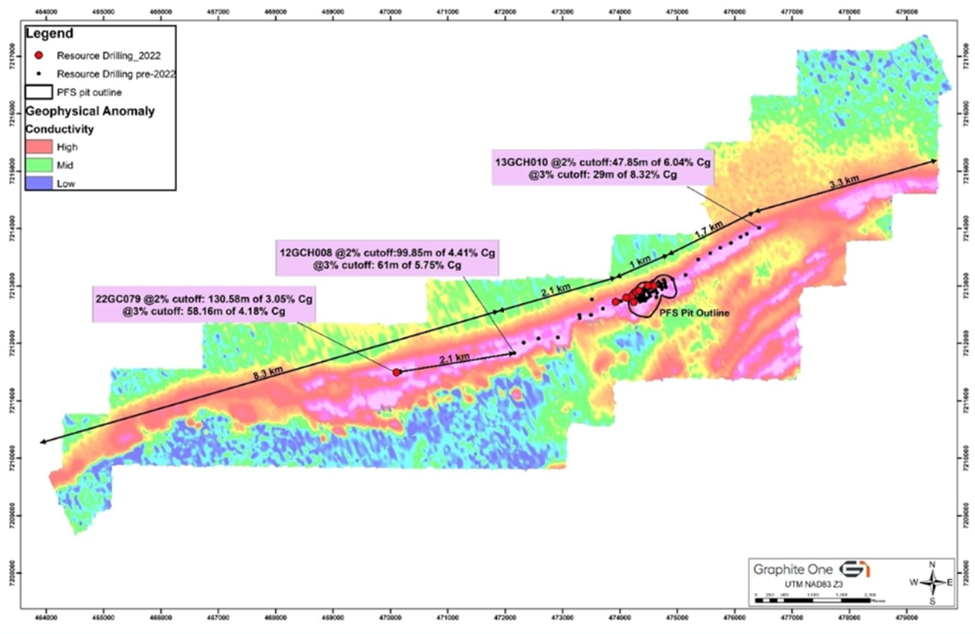

There is one company that almost certainly will have a role to play in this endeavor. Graphite One (GPH, OTCQX:GPHOF)is advancing the Graphite Creek property, situated along the northern flank of the Kigluaik Mountains, Alaska, spanning 18 kilometers.

Located on the Seward Peninsula, Graphite Creek in early 2021 was given High-Priority Infrastructure Project (HPIP) status by the Federal Permitting Improvement Steering Committee (FPISC). The HPIP designation allows Graphite One to list on the US government’s Federal Permitting Dashboard, which ensures that the various federal permitting agencies coordinate their reviews of projects as a means of streamlining the approval process.

In other words, having HPIP means that Graphite Creek will likely be fast-tracked to production.

The US Geological Survey has cited Graphite Creek as the country’s largest known graphite deposit, and recently extended that status to “among the largest in the world.”

Titled ‘Insights into the Metamorphic History and Origin of Flake Graphite Mineralization at the Graphite Creek Graphite Deposit, Seward Peninsula, Alaska, USA,’ the report also confirms what was mentioned earlier, that the United States is 100% net import reliant for graphite, with China supplying one-third of US imports and accounting for 60% of the approximate 1.1 million tonnes of global production.

“Flake graphite,” the report reads, “a highly ordered and crystalline form, is emerging as a particularly important source of spherical graphite used in the anode of lithium-ion batteries that power modern portable electronics, electric vehicles, and renewable energy storage systems…. Demand for battery graphite in 2040 is expected to be 25 times higher than in 2020 (International Energy Agency 2021). Thus, identifying potential flake graphite resources in North America and elsewhere is crucial for meeting future needs.”

“The new USGS report provides some very important insights that strengthen our knowledge base and deepen our understanding of how Graphite Creek and similar types of deposits are formed. It comes at a time when the United States needs to step up its game when it comes to Critical Minerals, and indicates how valuable USGS’s contributions can be,” said Mike Schaffner, Graphite One’s senior vice president of mining, in the March 9 news release. “We’re excited to incorporate this information into our 2023 drilling program as we continue to expand our Graphite Creek resource.”

President and CEO Anthony Huston said, “The USGS report underscores our confidence that Graphite Creek is truly a generational graphite resource. It anchors our supply chain strategy — from our mine to our planned advanced materials manufacturing plant and our recycling facility — to build a 100% U.S.-based graphite supply chain.”

In other words, Graphite One plans to simultaneously develop a battery anode materials manufacturing facility in Washington State and the Graphite Creek Mine in Alaska. Manufacturing would begin with purchased materials until Alaska production is available.

The Vancouver-based company has a memorandum of understanding (MOU) with Sunrise New Energy Material Co., Ltd., a lithium-ion battery anode producer based in Guizhou Province, China. Sunrise and GPH formed an alliance in 2022 to establish a graphite material manufacturing facility in Washington State.

The third link in Graphite One’s US-based graphite supply chain involves battery materials recycler Lab 4 Inc. of Nova Scotia, Canada. Under an earlier MOU, GPH and Lab 4 will work collaboratively to design and build a recycling facility for end-of-life EV and lithium-ion batteries. Lab 4 provides laboratory and engineering support to mining companies with a focus on recycling graphite, manganese and other minerals.

Between the mine, the manufacturing facility and the recycling plant, Graphite One plans to execute a “circular economy” strategy as it goes about building a US-based graphite supply chain.

The part of the USGS report about the Graphite Creek deposit’s size, is consistent with 2022 drill results that indicated the deposit remains open to the west, east and downdip.

Conducted last June to September, the field program included 1,940 meters of drilling for resource definition. The program also increased field camp capacity, completed key environmental baseline studies, and ran 210 meters of geotechnical drilling for the mill site and tailings area.

According to Graphite One, the 2022 drill results will be used to update the measured, indicated and inferred resource estimate published in the Oct. 13, 2022 prefeasibility study. The company expects to release these updated resource figures shortly.

The “prefeas” is based on only one square kilometer (<7% of the 16-km-long geophysical anomaly), meaning GPH could easily crank up production by a factor several times the current (proposed) run rate of 2,860 tonnes per day.

The company says the 2023 drill program will continue to delineate the scope and size of the resource.

Graphite concentrate is already being used to prepare sample battery anode materials for two major EV manufacturers, through Graphite One’s manufacturing partner, Sunrise. Sunrise is also preparing an artificial graphite anode sample for a third EV company.

If these sample batches are successful, it will surely push Graphite One onto the radar of not only major EV and battery manufacturing companies, but major mining companies.

We also have Graphite One signing a Materials Transfer Agreement with PNNL, the Pacific Northwest National Laboratory in Washington State, that will test the company’s anode-active and other materials to verify conformity to EV battery specs.

Then there’s Graphite One’s arrangement with Sandia National Laboratories in Albuquerque, New Mexico. A Graphite One subsidiary has provided Graphite Creek material to Sandia, for testing as a potentially critical mineral-rich carbonaceous feedstock, using its award-winning green extraction technology.

Both labs operate under the auspices of the U.S. Department of Energy.

Conclusion

Graphite One has been publishing a steady stream of good news lately, suggesting this could be G1’s breakout year.

Feasibility study drill work shows the deposit remains open to the east, west and downdip. An updated prefeasibility study with a new resource estimate is expected this quarter or next.

Graphite One plans to investigate increasing the designed production capacity at Graphite Creek, to be used in the feasibility study.

Graphite One also plans to complete 20,000 meters of drilling in 2023-24 with the goal of increased annual concentrate production for the upcoming FS compared to that assumed in the PFS.

Graphite Creek’s current size and potential for expansion — the USGS has named it the largest graphite deposit in the US and among the biggest in the world — indicates it could be ramped up to supply most if not all of the country’s graphite needs.

Another arrow in G1’s quiver: the company and the deposit have the political backing of the highest levels of government in Alaska, including Governor Mike Dunleavy and Senator Murkowski.

The Department of Energy is awarding $2.8 billion in grants to 20 manufacturing and processing companies for projects across 12 states.

The annual Defense Appropriations Bill, passed Dec. 15, 2022, includes funding for graphite as a rechargeable battery material, as well as natural graphite-based foam fire suppressant.

Graphite One’s production from Graphite Creek is expected to qualify for tax credits under the U.S. Inflation Reduction Act, because it plans to produce both anode materials and purified graphite in the United States, as required by the act.

The federal government has finally recognized US critical minerals vulnerability. Graphite is included on a list of 35 critical minerals the US Geological Survey has deemed critical to the national economy and national security.

There have not been very many times in my investing career where I’ve had such a strong conviction regarding a company’s success. Graphite One, aka G1, is such a company. Reread the green paragraphs above, my own confidence level, seeing it all on paper, is only strengthened. I believe G1 is in line for US Federal and State grants and investments from North American EV and battery manufacturers.

As for what the world’s miners think, well that’s anybody’s guess but you’d think they’d be smart enough, and quick enough, to make a move before an EV or battery manufacturer secures off-take agreements and ties up all that graphite.

Monumental shift in way junior mining stocks are valued is coming

If the US is serious about ending its dependency on China, and follows through on plans to build a US-based anode manufacturing supply chain, Graphite One has to be involved.

Graphite One Inc.

TSXV:GPH, OTCQX:GPHOF

Cdn$1.65, 2023.03.10

Shares Outstanding 83.3m

Market cap Cdn$181.2m

GPH website

Richard (Rick) Mills

aheadoftheherd.com

subscribe to my free newsletter

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.

Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.

Any AOTH/Richard Mills document is not, and should not be, construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

AOTH/Richard Mills has based this document on information obtained from sources he believes to be reliable, but which has not been independently verified.

AOTH/Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness.

Expressions of opinion are those of AOTH/Richard Mills only and are subject to change without notice.

AOTH/Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission.

Furthermore, AOTH/Richard Mills assumes no liability for any direct or indirect loss or damage for lost profit, which you may incur as a result of the use and existence of the information provided within this AOTH/Richard Mills Report.

You agree that by reading AOTH/Richard Mills articles, you are acting at your OWN RISK. In no event should AOTH/Richard Mills liable for any direct or indirect trading losses caused by any information contained in AOTH/Richard Mills articles. Information in AOTH/Richard Mills articles is not an offer to sell or a solicitation of an offer to buy any security. AOTH/Richard Mills is not suggesting the transacting of any financial instruments.

Our publications are not a recommendation to buy or sell a security – no information posted on this site is to be considered investment advice or a recommendation to do anything involving finance or money aside from performing your own due diligence and consulting with your personal registered broker/financial advisor.

AOTH/Richard Mills recommends that before investing in any securities, you consult with a professional financial planner or advisor, and that you should conduct a complete and independent investigation before investing in any security after prudent consideration of all pertinent risks. Ahead of the Herd is not a registered broker, dealer, analyst, or advisor. We hold no investment licenses and may not sell, offer to sell, or offer to buy any security.

Richard owns shares of Graphite One Inc. (TSXV:GPH). GPH is a paid advertiser on his site aheadoftheherd.com

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.