Graphite One raising CAD$35M for Active Anode Materials plant – Richard Mills

2026.03.01

Graphite One (TSXV:GPH, OTCQX:GPHOF) plans to build a graphite anode manufacturing plant in Trumbull County, Ohio, and is raising funds to put towards the project.

On Feb. 18 the Vancouver-based company announced that it closed a public offering involving the sale of 20,002,000 units for aggregate gross proceeds of CAD$35 million.

Each unit consists of one GPH common share plus a warrant priced at $1.75. Each warrant entitles the holder to acquire one common share at a price of C$2.25 per share for 36 months.

The company intends to use the net proceeds of the offering for the Active Anode Materials (AAM) plant-related expenditures including design and engineering, permitting and equipment purchases.

Subsequently, Graphite One said it has applied to list the warrants on the TSX Venture Exchange. It anticipates that 20,002,000 warrants will commence trading on the TSXV on or about March 3, 2026, under the symbol GPH.WT.A.

G1 has selected Ohio’s Voltage Valley as the site, entering into a 50-year land-lease agreement on 85 acres. The deal also contains an option to purchase the property once known as the Warren Depot, part of the National Defense Stockpile infrastructure.

According to Graphite One, the Voltage Valley site is in the heart of the automobile industry (the “Rust Belt” is being transformed into the “Battery Belt”). The site is accessible by road and rail, with nearby barging facilities. Existing power lines are sufficient for Graphite One’s Phase 1 production target of 25,000 tonnes per year of battery-ready anode material. Land is available for follow-on phases to ramp up to 100,000 tonnes per year of production.

Graphite One plans to become the first vertically integrated producer to serve the US EV battery market. Its supply chain strategy involves mining, manufacturing and recycling, all done domestically.

The Ohio facility represents the second link in Graphite One’s graphite materials supply chain; the first link is Graphite One’s Graphite Creek mine in Alaska, which completed a bankable feasibility study in Q2 2025, mostly funded by a $37.5 million grant from the Department of Defense.

G1’s Voltage Valley AAM manufacturing facility will initially produce synthetic Active Anode Materials from purchased materials and in the future add natural graphite AAM as graphite becomes available from the company’s Graphite Creek mine, located near Nome, Alaska, according to the March 20, 2024 news release.

The company can make other graphite products. Two possibilities are silicon-blend graphite, where silicon is embedded within a graphite matrix in the anode; and hard carbon, which improves ionic flow and provides higher power densities in batteries.

The plan also includes a recycling facility to reclaim graphite and other battery materials, to be co-located at the Ohio site, which is the third link in Graphite One’s circular economy strategy.

Active Anode Materials manufacturing

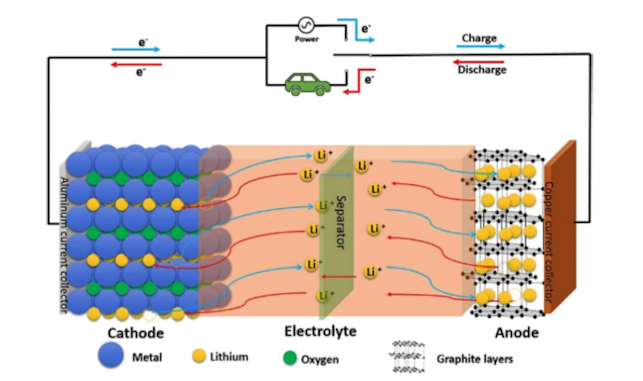

Active Anode Materials in a battery’s anode store and release lithium ions during charge and discharge. By manufacturing AAM from both natural graphite (derived from the Graphite Creek mine) and artificial graphite, Graphite One intends to complete America’s graphite materials supply chain.

Graphite is available in two forms: natural graphite (NG) and artificial graphite (AG). Both must be further processed to convert each into AAM to effectively function in lithium-ion batteries. AAM is designed and manufactured to meet each customer’s specifications. The AAM design necessary to each specification requires selection from a range of primary component combinations of NG AAM and artificial graphite AAM, either separately or in blends, and sometimes with other materials such as silicon and silicon monoxide (SiO). The specifications can be categorized to attain fast charging, high energy density, or longer life cycles.

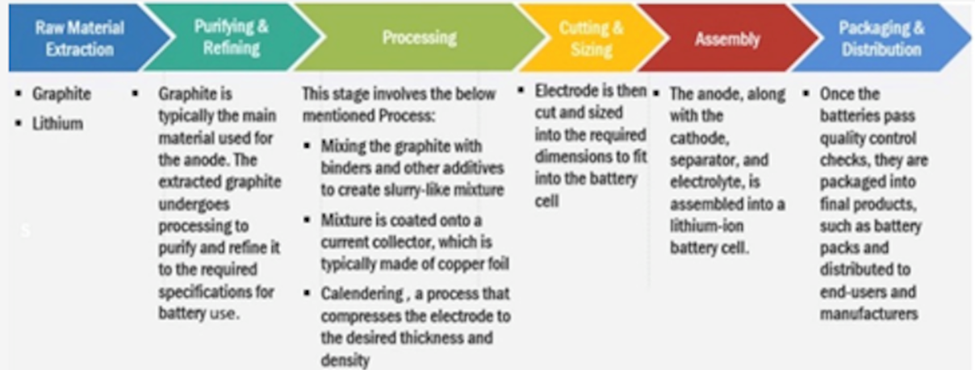

Graphite One plans to make both AG AAM and NG AAM for the electric vehicle and energy storage systems markets. The process for making each can be separated into three phases: preparation of the precursor materials; graphitization or purification of the precursor materials; and finishing/blending of the graphitized or purified material to produce the final AAM product. The precursor materials for AG AAM include petroleum cokes and pitches. For NG AAM, they are natural graphite concentrate and pitches.

AAM market

Active Anode Materials refers to materials that are being developed for use in various energy storage and convergence technologies; the primary focus is on improving battery performance.

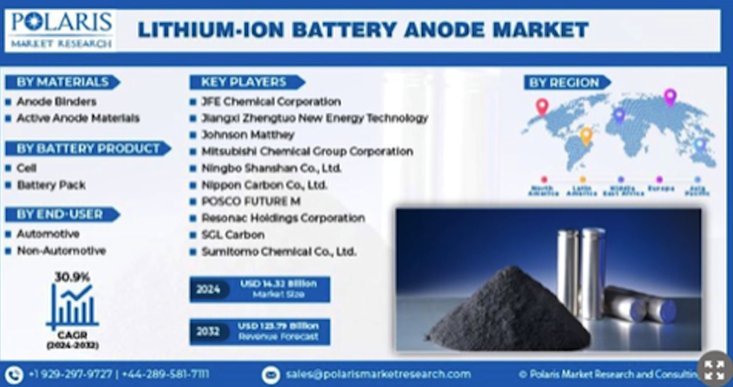

A report by Polaris Research valued the global anode market at $11.5 billion in 2023. By 2032, revenues should reach $123.7B, with the industry growing at a CAGR of 30.9%.

The main reasons for such a high growth rate is increasing global EV adoption and the global battery storage market.

“The lithium-ion battery anode market is experiencing notable growth due to electric vehicle acquisition. The growing approval of plug-in hybrids and EVs instantly translates into growing demand for lithium-ion batteries,” states Polaris Market Research via PR Newswire.

Another report by Markets&Markets projects anodes will grow from a $19.06 billion industry in 2025 to $81.24B by 2030, a CAGR of 33.6%.

The report concurs with Polaris Research’s observation that electric vehicles are the key demand driver but adds that industrial applications are increasingly adopting lithium-ion batteries for their efficiency and clean-energy benefits.

According to Barchart, the automotive segment is projected to record the highest CAGR during the forecast period. In terms of material, natural graphite is likely to register the highest CAGR due to its cost-effectiveness, wide availability, and excellent electrochemical properties suitable for large-scale battery production. As demand for electric vehicles and energy storage systems accelerates globally, manufacturers are increasingly turning to natural graphite.

The anode, also known as the negative electrode, is typically made up of graphite powder baked onto copper foil.

To be suitable for lithium-ion battery manufacturing, anode materials should meet the following requirements:

- Excellent porosity and conductivity

- Good durability and light weight

- Low cost

- Voltage match with preferred cathode

Technological advancements are resulting in the development of novel anode materials with higher energy densities, faster charging rates, and longer lives. This is propelling the use of next-generation anode materials in a variety of applications, including consumer electronics, energy storage, and electric vehicles.

According to an AI Overview, Active Anode Materials are currently undergoing a significant transition from traditional, cost-effective graphite to high-performance silicon-graphite composites, driven by the demand for higher energy density in electric vehicles and improved efficiency in energy storage systems. As of early 2026, the market is characterized by the dominance of synthetic graphite, the rapid adoption of silicon additives (5-10%), and the scaling of, or investment in, advanced materials to overcome performance bottlenecks.

Between 2026 and 2030, graphite is expected to remain the industry standard for AAM due to its stability, high conductivity, and lower cost. Synthetic graphite provides better consistency and cycle life for high-performance applications, whereas natural graphite is more cost-effective.

Silicon-graphite blends are emerging as the dominant next-gen solution, with 5-10% silicon commonly added to graphite to increase capacity by 20-40%.

Silicon oxide (SiOx) is often used in combination with graphite for high-end applications to improve lifespan and manage swelling.

Major manufacturers are actively integrating silicon-rich anodes to achieve 80% charging in under 15 minutes.

China currently dominates the AAM supply chain, but new US and European tariffs (e.g., 205% on some Chinese imports by February 2026) are accelerating the development of domestic production in North America and Europe.

The global battery storage market is experiencing rapid “explosive” growth, projected to expand from USD 44.12 billion in 2025 to over USD 183 billion by 2035. Driven by renewable energy integration, falling lithium-ion costs (potentially reaching $80/kWh by 2026), and grid-scale deployment, this sector is shifting from a niche to a primary infrastructure component.

Lithium-ion (specifically LFP) is the dominant technology, with 4-hour systems becoming more common. There is also a notable shift towards energy arbitrage as market dynamics evolve BloombergNEF report.

The surge is driven by the need for firm power, falling capital costs (CAPEX), and increasing deployment of wind and solar Reuters reports. Despite high growth, the market faces challenges like supply chain constraints BloombergNEF notes.

Synthetic graphite market and supply chain

Synthetic, or artificial graphite, and natural graphite are both used in battery anode applications, but synthetic dominates the market.

China controls 80% of synthetic graphite production.

Despite its higher cost compared to natural graphite from graphite mines, “its well-defined structure facilitates smoother lithium-ion movement, enabling faster charging and higher reliability,” states Markets&Markets. An additional advantage of synthetic graphite is its longer lifespan compared to natural.

Given Chinese export restrictions, and the vast potential of the synthetic graphite market, Graphite One is forging ahead with its plans to build America’s first synthetic graphite production plant.

The important thing here is security of supply. There is currently no commercial US production of synthetic graphite; to get it, a company would have to buy it from overseas companies such as China’s BTR and Shanshan. Other possibilities are Epsilon Advanced Materials (India), and Talga Group (Australia).

Graphite One intends to produce synthetic graphite from scratch, then make bespoke anode materials for their customers. G1 is the first link of a homegrown synthetic and natural graphite supply chain for EV batteries.

Conclusion

Graphite has the largest component in batteries by weight, constituting 45% or more of the cell. Nearly four times more graphite feedstock is consumed in each battery cell than lithium and nine times more than cobalt.

Graphite is therefore indispensable to the EV supply chain.

Automakers and defense companies have been raising alarm bells over the fact that the United States hasn’t mined any graphite since the 1950s, and even if it had, it would need to be shipped to China for processing. G1 intends to play a large part in correcting this.

But mine production, despite being fast-tracked, is a few years away. Graphite One’s plan to build an AAM plant in Ohio is an important interim step before mining begins.

Phase 1 production targets 25,000 tonnes per year of battery-ready anode material. Land is available for follow-on phases to ramp up to 100,000 tpy of production.

Graphite One could become the first synthetic graphite producer in the United States, ending decades of import dependence. Graphite One would produce its own synthetic graphite, not buy it from overseas companies, before manufacturing it into Active Anode Materials for its customers.

The opportunity here is huge.

The global lithium-ion battery anode market is projected to grow from roughly USD$19 billion in 2025 to over $81 billion by 2030, driven by a 33.6% CAGR as demand for high-performance materials increases.

China, meanwhile, has imposed restrictions on graphite exports. Exporters must apply for permits to ship synthetic and natural flake graphite.

The United States responded with countervailing duties. According to PV Magazine,

In its preliminary determinations in 2025, the DOC [Department of Commerce] imposed countervailing and anti-dumping duties of 11.58% and 93.5%, respectively. In the final determination issued on February 11, 2026, the DOC increased the countervailing duty rate to between 66.82% and 66.86%, while maintaining the anti-dumping duty rate at 93.5% for specified companies. A China-wide anti-dumping duty rate of 102.72% was imposed on all other exporters.

Imports of Chinese active anode materials are now subject to multiple layers of trade measures, resulting in a total effective duty of approximately 220%…

The duties apply broadly to anode graphite materials, as defined by Commerce, including synthetic and natural graphite products, whether coated or uncoated, as well as blended materials used in lithium-ion battery applications.

Increased usage of natural graphite is expected from non-Chinese sources, who are seeking to establish ex-China supply chains.

Graphite One is a ‘first mover’ at the forefront of this trend. The company has significant financial backing from the Department of Defense, and political support from the highest levels of government, including the White House, Alaska senators, Alaska’s governor, and investments from three Alaska Native corporations totaling $13.3 million from – Bering Straits Native Corporation, Doyon, LLC and Aleut Corporation.

Graphite, whether synthetic or natural, plays a vital, irreplaceable part in the move away from fossil fuels to the electrification of the US and global economies.

Graphite One Inc.

TSXV:GPH, OTCQX:GPHOF

2026.02.27 Share Price: Cdn$1.34

Shares Outstanding: 182.5m

Market Cap: Cdn$241.4M

GPH website

Richard (Rick) Mills

aheadoftheherd.com

Subscribe to AOTH’s free newsletter

Richard does own shares of Graphite One (TSXV:GPH). GPH is a paid advertiser on his site aheadoftheherd.com This article is issued on behalf of GPH

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.

{kind=link}

{kind=link}