Silver joining copper in upcoming supply crunch – Richard Mills

2022.11.09

Copper is one of the most important metals with more than 20 million tonnes consumed each year across a variety of industries, including building construction (wiring & piping,) power generation/ transmission, and electronic product manufacturing.

In recent years, the global transition towards clean energy has stretched the need for the tawny-colored metal even further. More copper will be required to feed our renewable energy infrastructure, such as photovoltaic cells used for solar power, and wind turbines.

The metal is also a key component in transportation, and with increasing emphasis on electrification, demand is only going to increase.

Silver, like gold, is a precious metal that offers investors protection during times of economic and political uncertainty.

However, much of silver’s value is derived from its industrial demand. It’s estimated around 60% of silver is utilized in industrial applications, like solar and electronics, leaving only 40% for investing.

As the metal with the highest electrical and thermal conductivity, silver is ideally suited to solar panels. About 100 million ounces of silver are consumed per year for this purpose alone.

Battery electric vehicles contain up to twice as much silver as ICE-powered vehicles. A recent Silver Institute report says the auto sector’s demand for silver will rise to 88Moz in five years as the transition from traditional cars and trucks to EVs accelerates. Others estimate that by 2040, electric vehicles could demand nearly half of annual silver supply.

Despite being widely used in many industrial applications, copper and silver are often skipped over in discussions of metals needed for the green economy, with battery metals like lithium, cobalt and nickel hogging the limelight.

Ahead of the Herd explains why the red and the white metal deserve more credit as decarbonization/ electrification metal mainstays, and why they are, imo, among the top tier of investable commodities.

Silver stocks depletion

The stocks of silver held by the London Bullion Market Association and the Comex, in New York, are thinning out. Silver inventories in London (the LMBA) have fallen for 10 straight months and are now sitting at a new record low of just over 27,100 tonnes, or 871.3 million ounces.

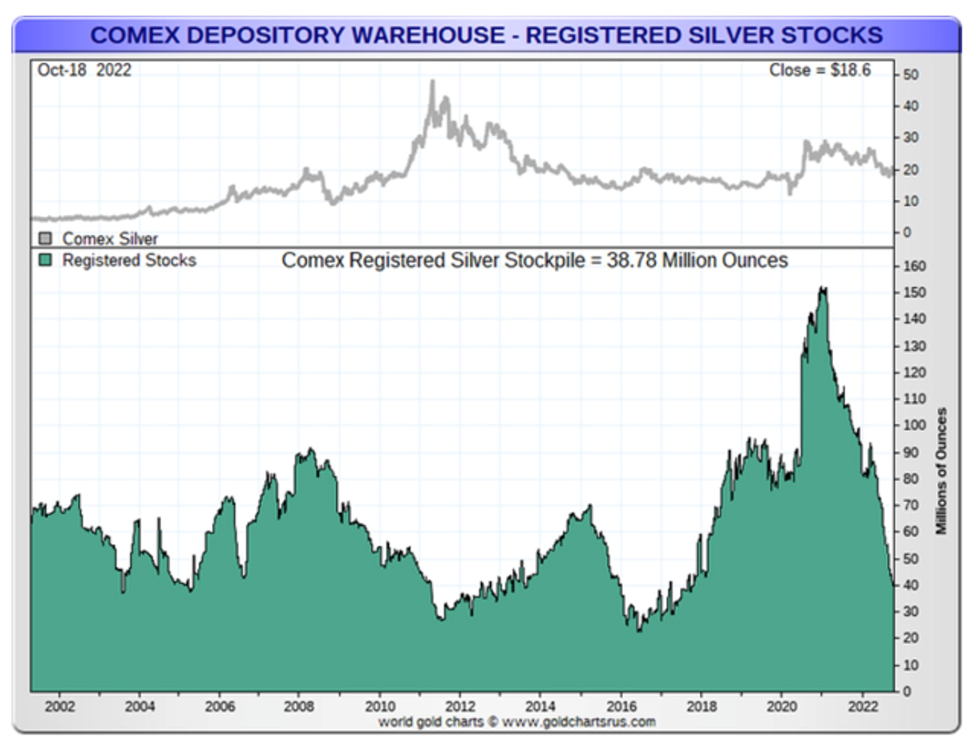

On the Comex, registered silver totals just 1,186 tonnes, or 38.13Moz, a five-year low. In September the LBMA vaults lost 45.166Moz, more than the Comex’s entire registered category.

Analysts are keeping a close eye on declining silver stocks worldwide, including Sprott Money, which wrote an article on the subject. The article references a column by Bullion Star’s Ronan Manly, in which he states that “There is an unprecedented situation emerging in London, where the relentless hemorrhaging of one of the world’s largest stockpiles of silver is now well and truly under way.”

In July, the “LBMA vaults” comprising the precious metals storage facilities in and around London run by the bullion banks JP Morgan, HSBC and ICBC Standard Bank, as well as the London vaults of three security operators, namely Brinks, Malca-Amit and Loomis, saw their silver inventories fall to a near 6-year low, below 1 billion ounces (997.4 million ounces or 31,022 tonnes).

During July and August, the bleeding continued, with the LBMA vaults losing another 2,517 tonnes of silver.

Source: LBMA, Gold Charts R Us

Manly explains that, from November 31, 2021 to August 31, 2022, the LBMA silver vaults were 27% lower, falling 7,915 tonnes, from 36,421t to 28,506t. That equates to just over a year’s supply of mined silver (the Silver Institute estimates that world annual silver mining production in 2022 will be 26,262t, or 843.2 million ounces).

Moreover, the total amount of silver in the LBMA vaults that is not pledged to the various silver ETFs, is only about 300,000 ounces or 10,000 tonnes. This is not even a third of annual mine supply and if withdrawals continue at July’s pace, total deliverable supply could be depleted by mid-2023, Manly calculates.

As for the Comex, the amount of silver in its vaults is also falling rapidly and is back to its lowest level since June of 2016.

Total registered silver stocks on the Comex have dropped nearly 70% over the past 18 months, to 35,527,659 oz.

According to Sprott Money:

What’s important is that almost half of the total COMEX silver vault is very likely a supply of silver that is not now, nor at any time in the future, readily available for physical delivery. And if that’s the case, the total COMEX vault is just about back to where it was in 2016—with just 150,000,000 ounces, of which just 35,000,000 is marked as registered and available for immediate delivery.

The upshot is that between the LBMA vaults and the Comex,

[s]ilver supply is not yet at a crisis stage. Metal can be mined, refined, and shipped in large enough quantities to forestall any immediate crisis. But what about the months and years to come? There’s currently a globally-recognized shortage of many other industrial metals, so this drain of global stockpiles could certainly continue into 2023.

By industrial metals shortage, Sprott Money is referring to copper, although zinc and lead should be factored in too (see below), since the majority of silver is mined as a by-product of those two metals.

Copper and the climate

According to S&P Global’s recent report, via Reuters, Efforts to reach carbon neutrality by 2050 are likely to remain out of reach as copper supply fails to match demand amid the growing use of solar panels, electric vehicles, and other renewable technologies.

Who better to confirm this than the CEO of one of the world’s largest copper companies, US-based Freeport McMoRan. Richard Adkerson said surging global demand for copper for electric vehicles, renewable energy and power lines would cause a shortfall, telling the Financial Times, “There is going to be a very significant shortage in copper. It’s going to be very difficult to meet the aspirations that have been set.”

Those aspirations include a recent report from Wood Mackenzie, a consultancy, that said 9.7mn tonnes of annual supply needs to come from projects yet to be sanctioned over the next decade. The market size is at present 25mn tonnes a year. “To date, a shortfall of this magnitude has never been overcome,” the authors wrote, predicting that $23bn of annual investment in new projects was needed, two-thirds more than the average over the past 30 years.

Another CEO of a major copper company, Codelco’s Maximo Pacheco, was quoted saying he expects a 6-7Mt deficit over the next decade. Pacheco also noted that Codelco won’t be able to match last year’s production levels for up to four years, citing the issue of reserves replacement.

Chile’s declining ore grades present a key downside risk to production forecasts. The chart below shows Chile’s average copper grades more than cut in half between 1999 and 2016.

Mining executives including Adkerson said the supply challenge is compounded by the downturn in the global economy, which has dragged down the copper price.

“This current economic turmoil is only making the problem worse,” he told the FT. “Companies are reluctant to invest in today’s world.”

Like silver, copper warehouse inventories are becoming depleted.

On Oct. 19, Reuters reported the available copper in London Metal Exchange warehouses halved within eight days. Indeed copper stocks at metal exchanges are falling to record lows. Trafigura, one of the world’s largest copper traders, has warned the market currently runs on inventories equivalent to just five days of global consumption, with the margin expected to drop to 2.7 days by the end of the year.

Copper: the most important metals we’re running short of

Russian copper shunned

Western sanctions on Russian companies due to the war in Ukraine are factoring into low copper inventories. The LME is talking about suspending deliveries of Russian metal (aluminum, copper and nickel), which at the end of September comprised over 60% of the exchange’s copper stocks.

Although there are no official sanctions around the importing and trade of Russian copper, some companies are “publicly self-sanctioning,” Fast Markets wrote in August.

“None of our customers are willing to take Russian material,” a copper trader told the commodity price reporting agency.

According to traders quoted by Fast Markets, more than half the copper warrants in warehouses could be of Russian origin, implying an even tighter market than shown on paper if these units cannot be financed or accepted by consumers.

Zinc and lead inventories low too

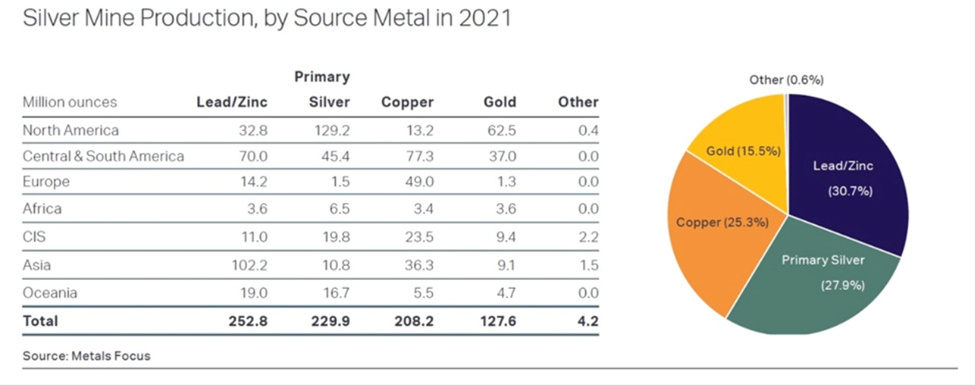

As we mentioned while analyzing the silver market, less than 30% of silver supply comes from primary silver mines. Over two-thirds is sourced from polymetallic ore deposits, including gold, lead/zinc operations and copper mines.

This makes the supply-demand outlook for the lead and zinc markets rather important. According to the International Lead and Zinc Study Group (ILZSG) smelter disruptions owing to high energy prices will cause global refined lead output to slide this year. Among the other supply pressures facing lead, are the flooding of Germany’s Stolberg plant, the loss of Russian imports due to sanctions, and the shuttering of secondary capacity in Italy. ILZSG also noted falling production in North America, Turkey, South Korea and Australia, including two months of scheduled maintenance at Nyrstar’s Port Prie, Australia smelter during the fourth quarter.

The group forecasts a global supply deficit of 83,000 tonnes this year and 42,000t in 2023. Reuters notes LME lead stocks are super low at 27,625 tonnes, equivalent to less than a day’s worth of global consumption, with physical premiums at record highs.

The base metal enjoyed a bump in its price last Friday, with lead futures gaining almost 10%, on news that lead will be included in the Bloomberg Commodity Index (BCOM).

Andy Home, Reuters’ metals columnist, made an interesting point about lead demand. He quoted the director for zinc and lead at Wood Mackenzie saying that, of the 80 million passenger cars produced last year, “just about every single one had a lead-acid battery in them.” That includes the 8 million EVs that rolled off assembly lines; a little-know fact: EVs have a back-up lead battery installed for safety systems and to power entertainment systems.

The market for zinc is less bullish than lead.

Since hitting a two-month high in August, attributed to Nrystar putting its Dutch zinc smelting operation on care and maintenance, zinc prices have softened.

Reuters describes zinc as “caught between weakening demand and sliding supply,” with prices dependent on which will fall hardest this year. Weighing on demand is the slowdown in the Chinese property market, lessening the need for zinc-coated galvanized steel.

Zinc prices are falling despite low exchange inventories. LME warehouse levels have shrunk to just over 40,000 tonnes, down by about 190,000t at the start of the year. In September Home observed both the Shanghai and the London zinc markets to be in backwardation, which is when the spot price is higher than zinc futures. “Both regions remain gripped by acute tightness,” he wrote, with European buyers paying record premiums of over $500 per tonne on top of the LME price — five times more than they were paying at the start of 2021.

Indian silver buying

Back to silver, despite this year’s price weakness alongside gold, there are multiple reasons to believe that longer term, silver will rebound.

The potential forces behind silver’s next rally include: monetary demand, industrial demand, above-ground stocks, gold-silver ratio, silver-copper correlation, net short positions reduced, physical market tightness, and low inventory.

Moribund silver may soon have liftoff

According to The Silver Institute, physical silver investment demand, consisting of silver bar and bullion coin purchases, is projected to jump 13% in 2022, achieving a seven-year high.

The Indian market is particularly strong for silver. Silver consumption there is forecast to surge by around 80% this year, Bloomberg said, as warehouse inventories are drawn down after two years of covid.

A recent article says that, while Indians bought low amounts of silver in 2020 and 2021, due to hits to supply chains and demand, this year silver sales are back on track:

Local purchases may surpass 8,000 tons in 2022 from about 4,500 tons last year, said Chirag Sheth, principal consultant at Metals Focus Ltd. That’s up from an April estimate of 5,900 tons.

“We are seeing a jump in purchases among retail customers, similar to what we saw in gold last year, because of pent-up demand,” Sheth said.

Imports during the January to August period were 6,370 tons compared to just 153.4 tons during the year-before period, according to the latest data from the nation’s trade ministry. For 2021, the country shipped in only 2,803.4 tons.

Most of the buying is from LBMA-accredited warehouses, which is contributing to the silver inventory drawdowns described above.

Silver to India is usually shipped by sea, but because of the high demand for it, the transportation mode has switched to air. Sheth added that wait times have also increased, with suppliers taking about 20 days to dispatch an order.

Bar and coin supplies pressured

According to one market analyst quoted by Kitco News, right now there is a significant disconnect in the silver market between investment demand in “paper” silver (ETFs, futures) and physical silver (bullion).

Physical investors are paying record premiums for bullion because there isn’t enough supply.

“Demand for physical gold and silver is off the charts. I’ve never seen anything like it in 20 years of doing this,” says Steve Rand, senior precious metals advisor with Scottsdale Bullion & Coin.

A recent article by SB&C notes gold and silver prices are strongly influenced by the buying and selling of futures contracts. Unlike “paper” gold and silver, there is a limited quantity of physical metal:

As a result, it’s typical for the spot price of gold and silver to take a while to catch up with the realities of physical demand. It’s only a matter of time before that gap is reconciled…

The entire precious metals industry is struggling to keep up with the skyrocketing demand for physical gold and silver. This extraordinary rush towards physical metals has resulted in market wide supply shortages and delivery delays of some gold and silver coins, gold bars, and silver bars. The combination of fewer people looking to sell gold and silver and a growing number of buyers is squeezing the availability of physical precious metals…

Physical gold and silver are getting scooped up quicker than suppliers and coin dealers can meet the demand. It’s only a matter of time before the spot prices jump to reflect the modern-day gold rush as retail investors, banks, and governments all flock to the safe haven of precious metals. Now is the perfect opportunity to take advantage of these temporary dips.

Conclusion

Obviously Scottsdale Bullion & Coin are talking their book, but I agree with the overall message: now is a good time to be stocking up on relatively cheap gold and silver, although for me, the better investment is in junior resource companies, who are exploring for and developing the world’s future mines.

But not just any mines. I’m particularly bullish on silver and copper, which despite their low profile among investors, are arguably the two most important metals for electrification and decarbonization.

There is no shift from fossil-fueled powered vehicles and energy sources without copper, which has no substitutes for its uses in EVs (electric motors, wiring, batteries, charging stations) wind and solar energy.

According to S&P Global, the world’s appetite for copper will reach 53 million tonnes by mid-century. This is more than double current global mine production of 21Mt, according to the US Geological Survey.

We already know that we don’t have enough copper for more than a 30% market penetration by electric vehicles.

How are we going to find the copper?

A recent Silver Institute report says battery electric vehicles contain up to twice as much silver as ICE-powered vehicles. Charging points and charging stations are also expected to demand a lot more silver.

It estimates the auto sector’s demand for silver will rise to 88Moz in five years as the transition from traditional cars and trucks to EVs accelerates. Others estimate that by 2040, electric vehicles could demand nearly half of annual silver supply.

This year silver followed copper down. Could the reverse happen, when copper runs higher, due to the structural supply deficit we’ve been forecasting for years? It seems quite likely. The two metals’ movements are closely correlated.

Silver seen tracking copper prices higher

Goldman Sachs is forecasting the LME copper price to more than double from its current level, to $15,000 a ton in 2025. Let’s step back here and remember the incentive price to make mining copper attractive is US$9,000 a ton — copper is trading currently at ~$7,000/t.

Copper will have to rise from its current price of US$3.63 to a minimum $4.50/lb to incentivize miners to build mines.

I’ll leave you with this. According to Adamas Intelligence’s State of Charge report, EV registrations rose by 42% in the first half of 2022, compared to the same period last year. This amounts to 6.23 million units, up from 4.4 million in H1, 2021. For round numbers, let’s just say that electrification is growing at 2 million units a year. How much copper and silver will be needed for that level of demand? And remember, the mining industry still needs to mine enough silver and copper for all the other industrial, and in silver’s case, monetary uses.

The soaring demand for both, matched against each’s coming supply crunch, all but guarantees that prices are moving higher.

Richard (Rick) Mills

aheadoftheherd.com

subscribe to my free newsletter

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.

Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.

Any AOTH/Richard Mills document is not, and should not be, construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

AOTH/Richard Mills has based this document on information obtained from sources he believes to be reliable, but which has not been independently verified.

AOTH/Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness.

Expressions of opinion are those of AOTH/Richard Mills only and are subject to change without notice.

AOTH/Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission.

Furthermore, AOTH/Richard Mills assumes no liability for any direct or indirect loss or damage for lost profit, which you may incur as a result of the use and existence of the information provided within this AOTH/Richard Mills Report.

You agree that by reading AOTH/Richard Mills articles, you are acting at your OWN RISK. In no event should AOTH/Richard Mills liable for any direct or indirect trading losses caused by any information contained in AOTH/Richard Mills articles. Information in AOTH/Richard Mills articles is not an offer to sell or a solicitation of an offer to buy any security. AOTH/Richard Mills is not suggesting the transacting of any financial instruments.

Our publications are not a recommendation to buy or sell a security – no information posted on this site is to be considered investment advice or a recommendation to do anything involving finance or money aside from performing your own due diligence and consulting with your personal registered broker/financial advisor.

AOTH/Richard Mills recommends that before investing in any securities, you consult with a professional financial planner or advisor, and that you should conduct a complete and independent investigation before investing in any security after prudent consideration of all pertinent risks. Ahead of the Herd is not a registered broker, dealer, analyst, or advisor. We hold no investment licenses and may not sell, offer to sell, or offer to buy any security.

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.