Gold Stocks Not Overvalued

By Adam Hamilton, CPA

Gold miners’ stocks have skyrocketed this year, hitting extraordinarily-overbought levels a few weeks ago. With gold in a similar exceedingly-stretched technical situation, that necessitated big-and-fast drawdowns in both which are now underway. Yet despite those gross excesses, gold stocks still never neared extreme valuations. Not being really-overvalued argues this powerful gold-stock bull will resume after this selloff.

Gold stocks are 2025’s Cinderella story, shining as the belle of the market ball after being forgotten and neglected for years. The leading GDX gold-stock ETF reclaimed some long-lost popularity as this year marched on. At its latest interim high in mid-October, GDX had soared a stupendous 149.0% year-to-date! That amplified gold’s parallel 65.8% soaring over this same span by 2.3x, in GDX’s usual 2x-to-3x range.

Gold stocks’ massive gains this year accrued in a sustainable trajectory until late July, when their Q2 earnings season was spinning up to full-swing. The major gold miners dominating GDX were reporting epic record results, their best fundamentals ever by far. That started attracting professional investors even though gold was then mired in a months-old high consolidation. Their capital inflows goosed this sector.

Gold stocks are ultimately leveraged plays on their metal because of their inherent profits leverage to it. Consider the example of those Q2 results. In the comparable Q2’24, GDX’s top-25 gold miners averaged all-in sustaining costs of $1,289 per ounce. The average gold price that quarter ran $2,337. Subtract the former from the latter, and these major gold miners as a sector were earning about $1,048 per ounce.

Fast-forward a year to Q2’25, and those GDX-top-25 average AISCs surged 10.5% year-over-year to $1,424. Yet that was much slower than gold prices, with their quarterly average soaring 40.6% YoY to a dazzling record $3,285! So implied unit profits ballooned to a record $1,861, skyrocketing fully 77.6% YoY! Thus the 44.8% jump in quarterly-average GDX prices between Q2’24 and Q2’25 was more than justified.

Such fundamental analysis is really important, but challenging to do. Reading many dozens of quarterly reports and collating their important data requires much expertise, experience, and time. I’m hard at work digging through new Q3 results as they are released, and hope to write my 38th GDX-top-25 quarterly-results essay in a row next week. This latest Q3’25 will almost certainly prove another best quarter ever!

The spreadsheet resulting from that nearly-decade-long research thread is massive and complex. But all that data accumulated over many years proved gold stocks were nowhere near overvalued as Q2 ended. Q3 is tracking the same way at this point. This new Q3 read is particularly important because over the subsequent couple-plus weeks after quarter-end GDX would soar to near-record overboughtness in mid-October.

Overvalued means stocks are priced too high relative to their underlying corporate fundamentals. That is very different from overbought, a technical term meaning stock prices have soared too far too fast to be sustainable. Extreme overvaluation slays secular bulls, while extreme overboughtness just necessitates healthy rebalancing selloffs within them. While GDX wasn’t extremely-overvalued, it was crazy-overbought.

In mid-October GDX soared an astounding 62.9% above its baseline 200-day moving average! I had warned about that mounting extreme overboughtness and its resulting risks in a late-September essay GDX Super-Overbought. Because of that we then ratcheted up the trailing stop losses on our extensive gold-stock trades, to protect more of their massive unrealized gains when that inevitable selloff eventually hit.

GDX at 1.629x its 200dma happened to be its third-most-overbought close in the entire 19.4-year history of this original gold-stock ETF! That ranked as top-0.3% levels of overboughtness, and gold itself was stretched way up to its own top-0.3% overboughtness since 1971! So some reckoning was coming to rebalance extraordinarily-extreme technicals and excessively-greedy sentiment, and soon hit like a sledgehammer.

GDX plummeted 6.8% the next day, then another 9.4% two days later! The latter proved GDX’s 14th-biggest down day ever! If you want more analysis on those huge GDX and gold selloffs, I wrote a whole essay right after they happened Gold Stocks Slammed.

Those averaged fantastic +182.7% annualized realized gains across thirteen gold-stock trades in our weekly newsletter and a similar +181.8% across six in our monthly! But just because gold stocks had hit dangerous extremely-overbought levels didn’t mean they were also extremely-overvalued. Despite the colossal gold-stock gains in 2025, this sector had been deeply-undervalued for years before this soaring.

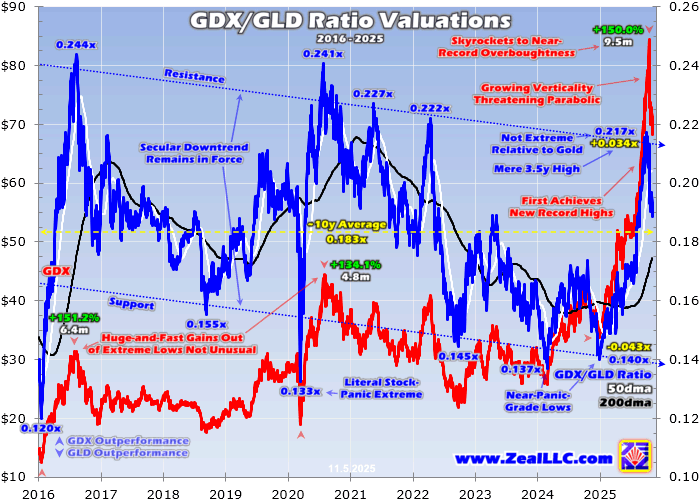

Starting from such battered levels, this sector still hadn’t climbed high enough to reach potentially-bull-slaying valuations. While gold miners’ quarterly fundamental data definitively proves that, Q3’25’s earnings season hasn’t concluded yet. In the meantime, a great easy proxy for how gold stocks are valued relative to the metal that overwhelmingly drives their profits is a simple construct called the GDX/GLD Ratio.

It merely divides GDX’s daily closes by GLD’s, the leading and dominant gold ETF. When charted over time, swings in this ratio reveal whether gold stocks are cheap or dear compared to the metal they mine. This chart looks at the last decade or so of GGR action, roughly the same span that I’ve been doing my deep quarterly research on GDX-top-25 results. In mid-October gold stocks never hit extreme overvaluations!

The raw GDX in red utterly skyrocketed this year, again up an epic 149.0% YTD at gold stocks’ latest peak. A 150.0% soaring is noted in this chart because gold stocks carved a major interim bottom on 2024’s second-to-last trading day. Just looking at that red line over this long secular span shows gold stocks have shot parabolic. That implies a blowoff popular-speculative-mania topping like bull-killing ones.

But relative to gold which drives its miners’ earnings, gold-stock price levels didn’t get extreme at all. The GGR merely hit 0.217x leading into mid-October’s peak! That was still well under all previous peaks in this past decade. Those include 0.244x in mid-August 2016, 0.241x in late July 2020, 0.227x in mid-May 2021, and 0.222x in mid-April 2022. And none of those prior GDX/Gold Ratio highs proved extreme either.

The GGR’s about-decade-long average from January 2016 to midweek runs 1.183x. But realize that gold stocks languished out of favor for most of this past decade. They enjoyed three powerful bull runs, but roughly seven other years of largely drifting sideways. During GDX’s previous decade or so ending in 2015, this same GGR averaged a far-higher 0.367x! Gold stocks fared considerably better in that earlier span.

Reflecting their general lack of popularity over this latest decade, the GGR has been drifting lower in a secular downtrend. Despite GDX’s massive skyrocketing in 2025 and resulting extraordinarily-extreme overboughtness, the GGR merely poked its head a little above its secular resistance line. Gold stocks soaring to extreme overvaluations would require a way-higher GGR peak, smashing past-decade highs.

Back to that latest-ten-year average of 0.183x, in late December 2024 at gold stocks’ last major low the GGR plunged to lower support hitting 0.140x. That was 0.043x under that secular mean. Yet the recent 0.217x peak witnessed in early October was only 0.034x above that long-term average. In other words, gold stocks haven’t even rallied proportionally to gold from their deep undervaluation heading into 2025.

Extreme overvaluations require big overshoots, far above averages. That certainly didn’t happen last month. Sliced another way, in 2023, 2024, and YTD 2025 the GGR averaged 0.166x which is on the low side historically. But in the prior three years of 2020, 2021, and 2022, the GGR averaged a much-higher 0.195x despite gold stocks getting obliterated in the COVID-19-lockdown stock panic early in that span.

Despite skyrocketing 150.0% in 9.5 months into mid-October, gold stocks still never neared high valuations relative to their metal. Even that mighty surge was comparatively-modest. Note above that back in mid-2020 GDX skyrocketed a similar 134.1% in about half the time at 4.8 months! Earlier GDX enjoyed another colossal bull run in early 2016 with huge 151.2% gains in just 6.4 months. 2025’s rally isn’t a wild outlier.

Amazingly gold stocks still continue to lag gold. Its current mighty cyclical bull was born way back in early October 2023. Over the next 24.5 months into mid-October 2025, gold soared 139.1% making for its largest cyclical bull ever! Normally the major gold miners of GDX amplify material gold moves by 2x to 3x, implying 278%-to-417% GDX gains over these last couple years. Yet gold stocks fell way short of that.

Over that same span, GDX only powered 226% higher for terrible 1.6x upside leverage to gold! Even more damningly for gold stocks’ bull run, much of their outperformance only accrued recently since late July 2025. At that point GDX was only up 99.3% gold-bull-to-date compared to the yellow metal’s 80.9% gains, amplifying them a dreadful 1.2x. If gold stocks don’t well-outperform gold, they’re not worth owning.

In addition to gold price trends driven by its own global supply and demand, miners heap on big additional operational, geological, and geopolitical risks. Gold can fare well, but if a miner experiences significant troubles on any of these fronts its stock price can still fall way lower. Compensating traders for those extra-gold risks is one reason GDX has tended to leverage material gold moves by 2x to 3x historically.

Gold stocks’ underperformance relative to gold since late 2023 resulted from their years of languishing deeply out of favor. They were so forgotten and neglected for so long that their popularity has really lagged gold’s. That’s why they haven’t yet soared to extremely-overvalued levels capable of slaying their secular bull. Despite being big absolutely, recent gold-stock gains have been quite weak compared to precedent.

Gold stocks haven’t even challenged seriously-overvalued levels in traditional terms. As part of my quarterly gold-miners-fundamentals research, I always look at their conventional trailing-twelve-month price-to-earnings ratios. Those aren’t as useful as the average implied unit profits for measuring gold miners’ fundamentals because of some major distortions. But P/Es still show gold miners aren’t really overvalued.

The biggest problem with averaging GDX-top-25 P/Es is some small and varying subset of gold miners are always flushing big non-cash writedowns through their income statements. The most-common ones are impairment charges for gold deposits or mines no longer worth as much as the capital invested due to operational, geological, or geopolitical challenges. These unusual items force their miners’ P/Es well higher.

Another key distortion is GDX’s upper ranks include a handful of royalty and streaming companies which are almost always wildly-overvalued. Some institutional investors love these types of gold stocks since their earnings and cashflows are way more predictable than miners’, bidding their stocks to very-high prices compared to their profits. Excluding these, the GDX-top-25 averaged 22.1x P/Es right after Q2 results.

I’ll collate the latest numbers over this next week working on GDX-top-25 Q3 results. But in the ones I’ve checked so far because they’ve already reported, P/Es are still mostly running in the teens! For reference after that last powerful gold-stock bull with GDX skyrocketing 134% into early August 2020, the Q2’20 GDX-top-25 average P/Es excluding royalties and streamers was running about twice as high at 43.6x.

Because gold stocks didn’t hit extremely-overvalued levels in mid-October, their secular bull run almost certainly isn’t over yet. But because they did hit extraordinarily-overbought extremes, they have to suffer a healthy rebalancing selloff before their rallying resumes. That’s already well-underway, with GDX plunging 19.1% in just thirteen trading days on gold’s parallel 9.5% drawdown making for 2.0x downside leverage!

And odds are that selling has a ways to run yet. In mid-October as gold peaked, my biggest-gold-bull-ever essay looked at what happened after the next-ten-largest cyclical gold bulls since 1971. Subsequent to their toppings, they averaged big 20.8% gold drawdowns over a fast 2.1 months! A similar big-and-fast selloff today would hammer gold back near $3,445 by mid-December or so. Gold stocks sure wouldn’t like that.

At GDX’s historical amplification range of 2x to 3x, that implies a brutal total drawdown of 42% to 62%! It might not get that bad since gold stocks underperformed so much in gold’s mighty cyclical bull, but 30%+ seems highly-likely. 40%+ wouldn’t be a surprise, but 50%+ seems excessive. At any rate, odds are recent weeks’ big-and-fast gold-stock selling isn’t the end of this drawdown. It will likely persist for some time.

But rather than fretting about the inevitable cyclicality of markets, speculators and investors alike should seize this opportunity. Periodic selloffs offer the best mid-bull buying opportunities to add new gold-stock positions at relatively-low prices. During drawdowns is the time to do your homework as we are, finding the best fundamentally-superior gold stocks to buy once this healthy rebalancing selloff looks to be maturing.

The bottom line is gold-stock valuations never challenged high extremes in recent years. That includes mid-October as GDX soared to some of its most-overbought levels ever. Despite getting too overheated technically, gold-stock prices remained fairly-modest relative to the metal overwhelmingly driving their profits. That lack of dangerous overvaluations argues this sector’s powerful bull run remains far from over.

But this sure doesn’t mean gold stocks will avoid the necessary reckoning from rallying too far too fast in recent months. Historical precedent implies gold itself is staring down the barrel of a 20%ish drawdown over a couple months or so, which gold stocks will amplify like usual. But once that largely passes rebalancing stretched technicals and sentiment, this gold-stock bull should resume until extreme overvaluations slay it.

Adam Hamilton, CPA

November 7, 2025

Copyright 2000 – 2025 Zeal LLC (www.ZealLLC.com)

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.