Copper Road exploring two large-scale, near-surface mineralized zones in Ontario’s famed district – Richard Mills

2023.05.12

For years, we have been reporting on how a decline in productivity from existing copper mines, combined with a lack of new discoveries from a lack of investment in exploration have produced a supply shortfall for what is now a critical mineral for the global economy.

It is estimated that more than 20 million tonnes are consumed each year across a variety of industries, including building construction, power generation/ transmission and electronic product manufacturing. In fact, copper metal is considered the cornerstone of all electric-related technologies.

In recent years, the global transition towards clean energy has stretched the need for copper even further, as a lot more of the metal will be required to feed our renewable energy infrastructure such as photovoltaic cells used for solar power and wind turbines.

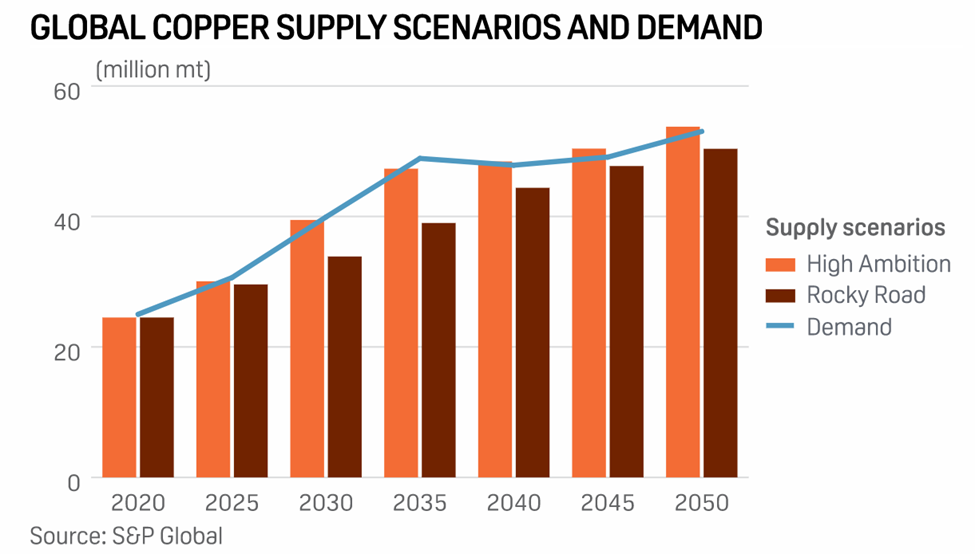

BloombergNEF estimates that copper demand, driven by various clean energy initiatives, will grow 53% to 39 million metric tons by 2040. Analysts at S&P Global are expecting an even quicker and bigger jump, with copper demand set to double to 50 million metric tonnes by 2035.

In a scenario that meets the Paris Agreement goals (as in the IEA’s Sustainable Development Scenario), the energy sector’s share of total demand must rise significantly over the next two decades to over 40% for copper.

However, looking further ahead in a scenario consistent with climate goals, the expected supply from existing mines and projects under construction is estimated to meet only 80% of the world’s copper needs by 2030, the IEA says.

According to consulting firm McKinsey, electrification is expected to create a 6.5 million ton shortfall at the start of the next decade, highlighting a substantial output gap that the mining industry has to address.

Therefore, new copper mines must be built, and in a timely manner, to close this gap.

The biggest players in the industry like Glencore, Vale and Anglo American have all been actively looking for copper development assets, and it’s only a matter of time before all these companies consolidate in places that have both the geographical advantage and history of success in copper exploration/production.

Ontario’s Advantage

While few would associate Canada with the likes of Chile or Peru when it comes to copper, the nation remains a solid contributor at 3% of the world’s total output in 2022.

But in terms of mining in general, there is perhaps no place better than Canada, especially the province of Ontario. It is often placed amongst the top 10 jurisdictions in the world for mineral exploration, and is home to some of the most mineral-rich deposits on the planet.

In fact, it is the major discoveries and mine development in the 20th century that underpinned Ontario’s status as Canada’s most populous and wealthiest province.

Today, there are as many as 35 active mining operations in Ontario, producing nickel, gold, copper, zinc and platinum, plus many others. Its copper production, together with that of British Columbia, accounts for over 80% of the domestic output.

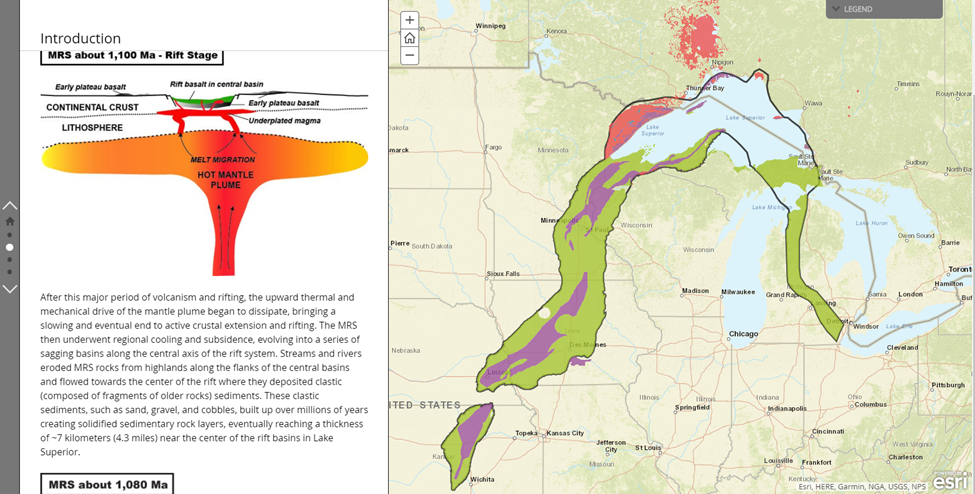

Behind Ontario’s wealth of mineral resources is the geological advantage offered by the Mid-Continental Rift, which curves for more than 2,000 kilometers across North America and is one of the world’s great continental rifts. Also called the “Keweenawan Rift”, it stretches across Lake Superior near Marathon, ON, all the way across Minnesota, Michigan, Wisconsin, Iowa, Nebraska and Kansas.

The copper that was mined in the Keweenaw formed during a spectacular period in Earth’s history— at a time when the North American continent was splitting apart (a geological process known as “rifting’). This separation began some 1.1 billion years ago and at its peak had a length of over 3,000 kilometers.

During the rifting, huge amounts of lava poured out of the earth’s crust, forming sequences thousands of feet thick. In the present day, these massive flood basalts are only exposed in the Lake Superior region. Throughout the rest of the US, they are buried in thousands of feet of sediments.

In the Lake Superior region, the rift-related rocks contain a wealth of mineral resources that were formed by magmatic and hydrothermal processes during the ~30 million year course of rift development. These rift rocks are host to Michigan’s storied native copper deposits, and contain significant copper (and nickel) that were deposited during various stages.

Studies have confirmed that the Midcontinent Rift System of North America hosts a diverse suite of magmatic and hydrothermal mineral deposits in the Lake Superior region, where the rift rocks are exposed at or near the surface. Historically, hydrothermal deposits such as Michigan’s native copper deposits and the White Pine sediment-hosted stratiform copper deposit, were major producers.

Ongoing exploration for and potential development of copper-nickel sulfide deposits hosted by the Duluth Complex of Minnesota and the opening of the Eagle nickel mine in Michigan indicate an expanding interest in these magmatic deposits.

Meanwhile, there are only a few copper developments on the Ontario side of the Keweenaw, providing an immense opportunity for mining companies to make new exciting discoveries in an era of high demand for critical minerals.

Copper Road Resources

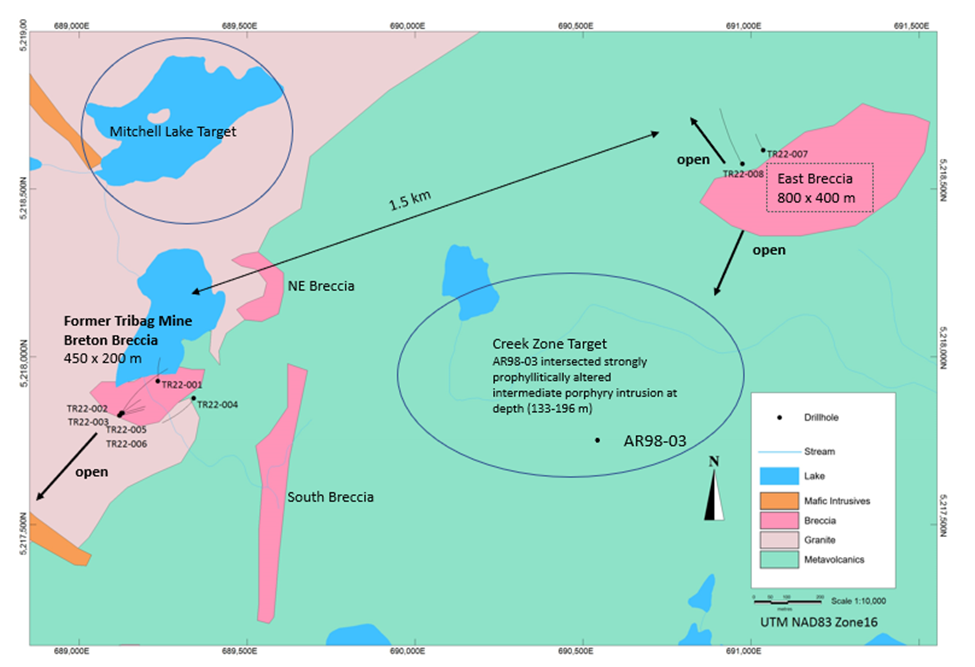

One Canadian junior miner looking to seize this opportunity is Copper Road Resources Inc. (TSXV: CRD), whose flagship project sits on the northeastern flank of the Mid-Continental Rift.

Copper Road’s property is district-scale, covering 21,000 hectares within the Batchewana Bay district, about 85 km north of Sault St. Marie, ON.

Part of the Copper Road project encompasses Proterozoic volcanic-sedimentary rocks intruded by breccia-porphyry bodies, and another part (previously, the Glenrock project) covers an adjacent window of classic Archean greenstone rocks.

The property package has a proven history of copper production, containing two former mines: The Tribag mine, which produced 1.2 million tonnes grading 1.52% Cu, and the Coppercorp mine, with historic production of 1 million tonnes at 1.16% Cu.

To date, there are several confirmed zones of mineralization within property boundaries — Tribag, Glenrock, JR (Richards/Jogran) and Coppercorp — each hosting multiple targets for exploration. Together, they span a total length of 30 km.

The former Tribag mine represents a porphyry-style copper deposit, consisting of four breccias (Breton, West, East South). Its reported historical production (1967-1974) was predominantly from the Breton breccia.

Historical estimates by Teck Resources, its former operator (1966-1972) and a household name in the Canadian mining industry, identified 40 million tonnes at 0.4% Cu from the Breton breccia, and estimated 125 million tonnes at 0.13% Cu and 0.05% Mo from the East breccia.

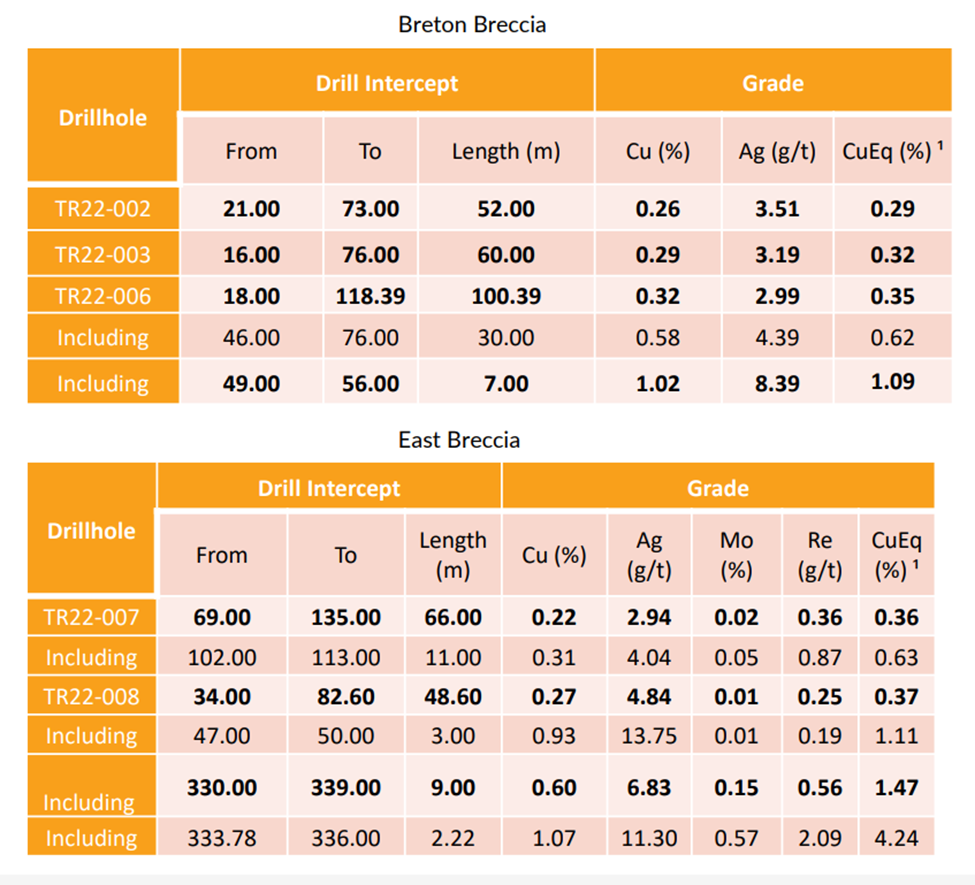

In 2022, Copper Road completed 3,000 m of drilling at the Tribag mine zone, designed to test the continuity of the significant zones of copper mineralization of the Breton and East breccia pipes.

All eight holes drilled in the program intersected significant intervals of near-surface mineralization, proving the continuity, depth, and additional mineralization outside of historical models at the Breton breccia. Notable results include hole TR22-006, with 100.39m at 0.32% Cu and 2.99 g/t Ag (0.35% CuEq), including a 5m interval at 1.11% Cu and 4.69 g/t Ag (1.15% CuEq).

The 9 m high-grade zone (1.47% CuEq) at depth also indicated potential for high-grade mineralization related to a feeder structure at the East breccia.

Commenting on the results, John Timmons, Copper Road’s president and CEO, said: “We believe our first drill program into our flagship property is just the start of reviving this historical mining district and clearly demonstrates that there is more copper to be mined.”

Given last year’s success, the company plans to continue exploring the Tribag zone in 2023.

Second Large-Scale Zone

Another area of particular interest is the JR zone, located 12 km from the Tribag mine.

The JR zone consists of the Richards breccia, a near-surface copper target, and the Jogran surface porphyry, which has been drilled to a depth of 200 m. The two targets are located 900 m apart.

The company’s plan this year is to expand this surface exploration and drill test the JR zone to establish a second large-scale mineralized zone at its Copper Road project.

Due to fragmented claim ownership and regional staking closures, the JR zone has only seen limited diamond drilling into these near-surface porphyry and breccia-hosted Cu-Mo-Au-Ag targets.

Historical exploration by Jogran Mines (1964), Phelps Dodge (1966), Duration Mines (1988), and Aurogin Resources (1997) encountered relatively broad near-surface intersections of copper mineralization that is still untested below 150 m in the porphyry, and below 75 m in the breccia.

In fall 2022, the company completed three reconnaissance Mobile Metal Ion (MMI) soil sample lines over the JR zone to evaluate the potential for an expanded footprint of the mineralized system(s) in areas outside of known mineralization.

All three lines returned strongly anomalous copper and molybdenum (as well as tungsten and silver) and localized gold over the known occurrences, confirming limited drilling and trenching, but also extending the anomalies for hundreds of metres in most directions in both Cu and Mo and discovering new Cu anomalies.

This, as Copper Road says, indicates the potential for a much larger footprint of the known mineralization, which at this point extends as much as 1.5 km along strike and up to 550 m wide.

Besides responding to the known mineralization, the expanded anomalies around the JR zone are equal in strength to those reported by Heberlein (2010) from MMI test lines completed over the Mount Milligan and Kwanika alkalic porphyry deposits in British Columbia.

And so, the company says it is reasonably confident that the MMI anomalies at Jogran and Richards represent valid potential concentrations of metals at shallow depth beneath the thick overburden cover (2 to 15+ metres) that is common in the project area.

Meanwhile, the company is still finishing the compilation of all historical exploration data, including drill holes in the area of the MMI anomalies. After a full review of all drill logs, the initial indications are that all holes proximal to or within the MMI anomalies intercepted widespread and consistent Cu±Mo mineralization, says Copper Road.

The core was subject to minimal sampling (e.g., on average only 7.6% of the Phelps-Dodge drill core was sampled and assayed), which the company believes was due to historical copper exploration in the 1960s to 1980s being focused on sourcing copper grades above 1%. Also, the operator in the 1990s was reportedly focused strongly on gold, so that copper mineralization was not considered significant.

Overall, but especially in the 1960s, assays for Au, Ag, Mo and W were rarely performed, so the value of these potential by-product credits may increase copper equivalent grades (CuEq) significantly.

For example, the average grade (historical in nature and not 43-101 compliant) of the main holes drilled into the Jogran porphyry in the 1960’s averaged 0.2% Cu and 0.032% Mo, which at today’s current LME spot metal prices (4.01 US$/lb Cu and 21.50 US$/lb Mo) represent a CuEq grade of 0.37% (assuming 100% recovery and using the formula CuEq % = % Cu + (% Mo x 5.36).

As part of the data compilation, a small Gradient IP survey completed in 1997 by former operator Aurogin Resources over the Richards breccia was digitized. The survey delineated two distinct ovoid chargeability anomalies, one of which underlies the known mineralization at Richards breccia, and a possibly larger and stronger anomaly (approximately 145 x 260 m, open to the NW), completely untested, located approximately 250 m NW of the Richards trench.

The subsurface below the trench was subsequently tested by three drill holes (AR98-07: 27 m @ 1.46% Cu, 0.17 g/t Au, 3.8 g/t Ag, AR97-25: 40 m @ 0.86% Cu, 0.06 g/t Au, 3.5 g/t Ag, AR97-24, 13.7 m @ 0.64% Cu, 0.06 g/t Au) that are located at the north edge of the second chargeability high (approximately 190 m wide) that extends SE for 130 m before trending off the survey grid. A third chargeability high is located at the east end of the grid but is so far only a two-station response on the south-most line, and it remains to be fully delineated.

Conclusion

Based on these results, an announcement was put out by Copper Road in April 2023 confirming the validation and expansion of the JR zone as its main exploration focus alongside the Tribag mine zone.

“The company is planning further exploration and drilling in 2023 to develop and de-risk the JR Zone targets, as well as expanding regional exploration to further enhance additional mineralized porphyry and breccia targets that have been identified through historical data compilation over this large project area,” CEO Timmons said in the release.

Though still in its early days, there’s a lot to like about the Copper project, including its large size with several mineralized zones of high-grade copper either near surface or at depth, plus many other untested areas.

We also can’t ignore its location. Note: The Mid-Continental Rift is the same structure that formed Lake Superior and the world-class Keweenawan peninsula copper mining region in the US, which housed the initial copper rush in the mid-1800s and was mined for more than 150 years.

This means there’s lots of copper yet to be mined in this area, as industry leaders like Teck had done in the past. The next updates from the company will tell us more about the full potential of this 21,000-hectare land package.

Copper Road Resources

TSXV:CRD

Cdn$0.08, 2023.05.011

Shares Outstanding 47.3m

Market cap Cdn$3.8m

CRD website

Richard (Rick) Mills

aheadoftheherd.com

subscribe to my free newsletter

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.

Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.

Any AOTH/Richard Mills document is not, and should not be, construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

AOTH/Richard Mills has based this document on information obtained from sources he believes to be reliable, but which has not been independently verified.

AOTH/Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness.

Expressions of opinion are those of AOTH/Richard Mills only and are subject to change without notice.

AOTH/Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission.

Furthermore, AOTH/Richard Mills assumes no liability for any direct or indirect loss or damage for lost profit, which you may incur as a result of the use and existence of the information provided within this AOTH/Richard Mills Report.

You agree that by reading AOTH/Richard Mills articles, you are acting at your OWN RISK. In no event should AOTH/Richard Mills liable for any direct or indirect trading losses caused by any information contained in AOTH/Richard Mills articles. Information in AOTH/Richard Mills articles is not an offer to sell or a solicitation of an offer to buy any security. AOTH/Richard Mills is not suggesting the transacting of any financial instruments.

Richard does not own shares of Copper Road Resources (TSXV:CRD). CRD is a paid advertiser on his site aheadoftheherd.com

This article is issued on behalf of CRD

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.