AOTH metals and company roundup

2019.07.20

At the beginning of January we at Ahead of the Herd made a bold prediction: that Commodities are the right story for 2019. Considering the poor 2018 that most metals had, especially industrial metals dragged down by uncertainty over China-US tariffs and tariff threats – to stick our necks out for metals could have meant the guillotine.

We pinned our thesis on four main points: 1/ Commodities are cyclical, and the timing is right to be invested; 2/ The US dollar is likely to fall or be range-bound during 2019; 3/ A looser monetary policy by the Federal Reserve would weigh on the dollar and be good for commodities; 4/ The need for infrastructure spending is not going to let up. Despite the Chinese economy weakening, Beijing will continue to demand iron ore and base metals for its Belt and Road Initiative and other ambitious megaprojects. India and other developing nations are also in the mix.

A key message in our article was the global shift towards the electrification of the transportation system (cars, trucks, buses, trains) involves moving from an oil-based economy to one grounded on electric vehicles and sources of energy that emit fewer to no greenhouse gas emissions.

The electrification trend calls for a slew of battery metals – lithium, graphite, nickel and cobalt – along with tonnes of rare earths and copper.

The first three are crucial to this global transportation shift, because they all go into electric vehicles. Lithium is used in the different configurations of EV batteries (eg. NCA = nickel-cobalt-aluminum, NMC = nickel-manganese-cobalt) where lithium is the dominant metal in the battery.

Copper has under-performed this year, but we see this as a blip in a long-term trend that supports prices due to a pending supply shortage. Output at some major mines (eg. Escondida, Las Bambas) is falling, as are ore grades.

We continue to believe in gold because a/ it’s smart to have gold as a portion of your portfolio (most managers say 10% minimum); b/ low global growth has pushed many central banks to cut interest rates and stimulate their economies with bond-buying, a very bullish signal for the gold price; c/ appetite for gold has soared due to negative yields and slowing economic growth; and d/ now is an excellent time to own physical gold or gold stocks. Central bank gold buyingis at a record high as some countries move further towards de-dollarization.

Silver is also on our radar due mostly to the gold-silver ratio falling, presaging an upside for the white metal.

It turns out our contrarian position on commodities was forward-thinking and bang on. A half-year into 2019, we see major commodities indices up significantly.

The S&P GSCI Commodity-Indexed Trust (NYSEArca:GSG) had one of its best performing half-years, gaining 13% as of June 30. Crude oil was the top-performing commodity in H1, followed by palladium, states Safehaven.

After a couple of down months, seven of 10 Monthly Metal Indices (MMI) increased for July, MetalMiner reports. The only index to fall was steel, due to weak US steel prices, with aluminum and construction MMIs trading flat.

This week we’re taking a run through the metals we’re bullish on, and invested in. The company following each commodity write-up is an exclusive AOTH stock pick. Click on the company’s name to find out more, and scan my front page for in-depth articles on the commodity markets we’re covering.

Palladium

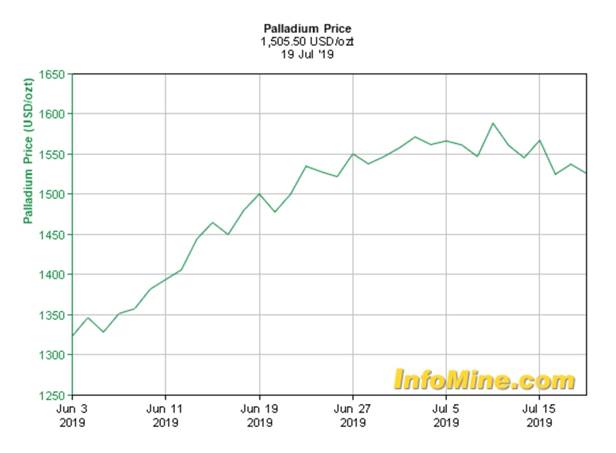

MetalMiner also notes the spread between palladium and platinum prices widened this past month. As of July 19, palladium closed at $1,505.50 an ounce versus $843.50/oz for platinum. Readers will notice that’s higher than the gold price which is trading around $1,425/oz. In January palladium raced past gold for the first time since 2002. Twice this year it’s broken the $1,600 an ounce mark.

Palladium is surging because of supply challenges and tougher emissions standards revving up demand for gas-powered vehicles, which use palladium in their catalytic converters, and hybrid vehicles.

By comparison platinum use is falling because the precious metal is used in the autocatalysts of on-the-way-out polluting diesel vehicles.

A recent Reuters article reports that The auto industry has all but stopped developing next-generation combustion engines as limited resources are directed towards building electric and self-driving cars.

Concerns over air pollution led the EU to set a target of cutting emissions by at least 40% by 2030, from 1990 levels. China, whose major cities are often blanketed with thick air pollution, has also begun to implement tougher vehicle emissions standards. The country is targeting a reduction of between 26 and 28% of emissions from 2005 levels by 2030.

According to Norilsk Nickel, which controls 40% of the world’s palladium production, palladium demand is intensifying. Bloomberg says a market analyst at the Russian miner is forecasting that combined palladium use in hybrids (HEVs) and plug-in hybrids (PHEVs) next year will be nearly triple that of 2016. JP Morgan & Chase is equally bullish on the precious metal. In a report, the investment bank predicts by 2025, hybrids will represent over 25 million vehicles, close to a quarter of all vehicle sales, compared to just 3% in 2016.

Not only has demand bounced up, palladium is also facing constricted supply. 2018 was the seventh year in a row that palladium was in deficit because of strong vehicle sales. The way things are going, 2019 will be the eighth year.

According to a report from Sprott Asset Management, “Supply shortages continue to support palladium’s performance, with strong multi-year growth in palladium demand now straining a fixed supply.” Citigroup said in December that production is expected to trail consumption by 545,000 ounces this year.

Indeed, there is limited scope for producers to increase supply, in the near term.

South African palladium is a by-product of platinum mining and palladium from Russia is a by-product of nickel. Between them, the two countries control 75% of the palladium market.

Safehaven notes that labor tensions are heating up in South Africa, with the Association of Mineworkers and Construction Union (AMCU), calling for a 48% rise in the minimum wage.

Platinum mining in South Africa is frequently interrupted by labour unrest. The country’s platinum miners are under constant pressure to contain costs, because their mines are some of the deepest and most labor-intensive in the world. High temperatures are also a serious issue. Platinum is being mined in reefs up to two kilometers deep, where virgin rock temperatures have been measured at 70 degrees C.

In 2014 workers at the country’s three major producers – Lonmin, Anglo American Platinum and Impala Platinum – downed tools for five months demanding that wages be doubled. The strike was the longest and most expensive in South African history, shutting down about 40% of the world’s platinum production.

Palladium One Mining Inc (TSX.V:PDM)

Palladium is integral to global transportation, energy shift

Re-capitalized, re-named Palladium One focused on mining-friendly Finland

Palladium, darling of the PGEs, shifting into high gear

Zinc

In 2017 zinc enjoyed a spectacular run from $1.19 a pound to $1.61 within only six months (+35%). Prices got a nice uplift from mine closures and an expected long-term structural supply deficit. The metal’s hot hand had many juniors roaming around with boots on the ground trying to find the next zinc deposit.

The zinc market was in deficit in 2018. According to the USGS, despite new zinc mines opening in Australia and Cuba in 2017, and increased production at the Antamina mine in Peru, supply failed to keep up with consumption. Some very large zinc mines have been depleted and shut down in recent years, with not enough new mine supply to take their place.

MMG’s shuttered Century mine for example used to supply 4% of the world’s zinc. Between the shutdown of the Lisheen mine in Ireland, Century, and Glencore’s Brunswick and Perseverance mines in Canada, over a million tonnes was ripped from global zinc production.

The closed mines represent an estimated 10 to 15% of the zinc market. On the flip side, there have been few discoveries or big zinc projects planned. This is setting the zinc market up for a supply shortage.

The International Lead and Zinc Study Group predicts the zinc market will again be in a deficit position of 72,000 tonnes in 2019.

Tighter environmental restrictions in China are lessening the amount smelters can produce.

Antaike, a Chinese metals research firm, estimates national production of refined zinc in 2018 fell to just 4.53 million tonnes, the sharpest downturn since 2013, Reuters said.

The result has been a record amount of zinc imported into the world’s largest metals consumer, 715,355 tonnes of refined zinc in 2018. The high demand in China has also pulled a lot of zinc out of LME warehouses.

In February zinc inventories fell to the point where there was less than two days worth of global consumption locked in London Metal Exchange warehouses. The paucity of the metal used to prevent rusting caused prices to spike to the highest they’ve been since last June.

Zinc prices were US$2,845 a tonne or $1.29 a pound, after data showed LME warehouses held just over 58,000 tonnes. Levels have since increased to 80,000 tonnes but are a long way off the 250,000t stockpiled a year ago. According to the International Lead and Zinc Study Group, there was a deficit of 123,000 tonnes for the first five months of this year.

Boreal Metals Corp (TSX.V:BMX)

Boreal hits more high-grade at Gumsberg’s South Discovery, Sweden

$2 trillion infrastructure plan will require mega metals

China’s environmental crackdown buoys lead, zinc

Nickel

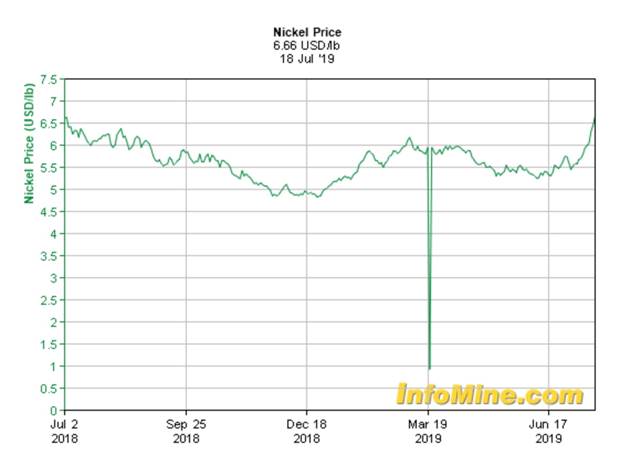

Once mined almost exclusively for its use in stainless steel, the industrial metal has enjoyed something of a rebirth since battery-makers started using it in electric vehicles. According to Adamas Intelligence, which tracks battery metals, EV manufacturers deployed 57% more nickel in EV batteries this past May, versus May 2018. MINING.com reports the inroads nickel have been making are due mainly to an industry shift towards “NCM 811” batteries which require over 50 kg of nickel. (NCM 111 batteries have one part each nickel, cobalt and manganese). The switch to NCM 811 could outpace the amount of nickel used for EVs, compared to stainless steel, adding up to 900,000 tonnes annually, by 2030, one analyst said.

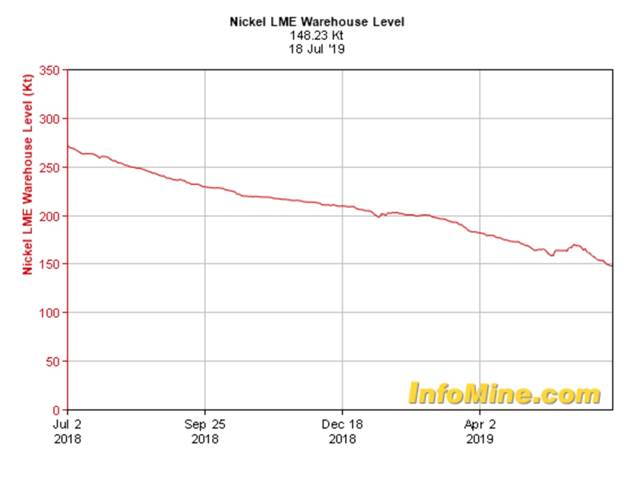

On the supply side, solid stainless steel production, a supply deficit and record-low warehouse inventories are contributing to the bullish case for nickel. Nickel stocks in LME warehouses have fallen to a 6.5-month low, from 450,000 tonnes in 2016 to just 147,942 tonnes, MetalMiner reports.

Another recent supply factor concerns Indonesia, a major nickel producer. The country this week re-instated a ban on ore exports, starting in 2022, to encourage the building of domestic smelters.

Nickel demanded for EV batteries and stainless steel, plus tight supply has resulted in a nickel price spike. Two weeks of technical and speculative buying hiked the metal to $15,115 a tonne on Thursday, the highest in over a year, and 20% better than two weeks ago. Year to date, nickel has been the star of the industrial metals complex, surging an impressive 37%.

Palladium One Mining Inc (TSX.V:PDM)

Cobalt

According to Roskill, standard-grade cobalt prices started the year at $26 a pound but have fallen in the first quarter, to $14 per pound in March. That’s a fair distance from the $40/lb prices reached in April of 2018.

However, Roskill observes that “some restocking is taking place” which should push cobalt prices back up after reaching a bottom of $14/lb in March. The metals consultancy expects prices to recover in 2019.

Roskill attributed the price slide to oversupply, especially of cobalt hydroxide, clashing with sluggish demand. Many buyers have stayed on the sidelines, preferring to buy on the spot market. A lot of cobalt that was not committed to long-term contracts last year added to the glut, Roskill explained. Still, DRC cobalt production expanded by 44% in 2018 to 106,439 tonnes. The African nation produces between 60 and 75% of world supply.

Oilprice.com writes that several years of rising cobalt prices “brought about a rush to mine as much cobalt as possible and sell it to the Chinese,” noting that China accounts for two-thirds of the world’s lithium-ion megafactory capacity. The publication also argues that artisanal mining in DRC was a factor in over-production.

But, a very recent article by Bloomberg reports that the market expects to see a big drop in artisanal cobalt output this year, due to prices falling. The hard-scrabble miners who use rudimentary digging tools, are switching to copper instead.

Another reason for the anticipated 70% decline in artisanal output, is less miners, says Bloomberg, citing cobalt specialists at Darton Commodities and Roskill:

The workforce at Kaumbu’s cooperative has halved this year to around 500 and the group is only producing 2,000 tons of ore a month, 15% of which is cobalt, compared with 4,000 tons of cobalt ore and 1,000 tons of copper a year ago.

Artisanal production will retreat to levels seen in 2013 to 2016 before the boom, said Jack Bedder, a cobalt expert and director at Roskill Information Services.

The Mutoshi Cobalt artisanal project has shed about 2,800 of its 4,100 authorized diggers this year.

As lack of artisanal supply is absorbed by the market resulting in higher prices, though, driven by explosive demand for cobalt used in EV batteries, more workers should return.

“Artisanal mining will continue to be the swing producer,” Bloomberg quotes George Heppel, senior analyst at CRU Group.

Boreal Metals Corp (TSX.V:BMX)

Universal Copper Ltd (TSX.V:UNV)

Copper

There is no getting around the fact that the copper market is experiencing some weakness. However, we see the current price slippage as a blip in what the evidence points to as a growing and powerful bull market for copper.

As we wrote in The coming copper crunch, copper mine production is expected to increase for the next year or so, then drop off significantly. By 2035, without major new mines up and running to replace the ore that is being depleted from existing copper mines, we are looking at a 15-million-tonne supply deficit by 2035. Four to six million tonnes of added capacity are needed by 2025. Lower ore grades are also part of the waning supply picture. Copper grades have declined about 25% in Chile in the last decade – highlighting the urgent need for grassroots exploration to arrest the trend.

One country that may be able to help fill the supply gap is Colombia. Better known for coal and gold than copper, Colombia is reportedly hoping to diversify into the essential base metal. The country only has one producing copper mine, in the Choco department of northwest Colombia. Choco is also the region the Andean Copper Belt runs through. The belt hugs the South American coastline all the way from Chile in the south to Central America in the north, and hosts some of the largest copper porphyry deposits in the world.

For now though, copper output is falling. Exports from Chile’s Escondida, the world’s second largest copper mine, are expected to drop this year by 85% due to operations moving from open-pit to underground. That’s a dramatic fall from 1.8 million tonnes in 2018 to just 200,000 in 2019. The mine is expected to take until 2022 to re-gain full production, I find it hard to believe they will produce the same tonnage from underground as open pit.

A processing problem at BHP’s Olympic Dam copper, gold and uranium mine ate into the company’s second-half production numbers. Problems in Zambia, Africa’s second-largest copper producer, are putting a big question mark beside the country’s output. First Quantum Minerals has reacted to a planned tax hike on operators by laying off 2,500 workers. Barrick is reportedly considering selling its Lumwana copper mine.

Another example of copper output declining is an expected delay at Mongolia’s Oyu Tolgoi mine going underground. Difficult ground conditions are cited as the reason the expansion could be delayed up to 30 months.

Globally, MINING.com reported a 2.4% production fall in February, with Chile and Peru hit the hardest, at a respective 7.1% and 5.1% reduction, year on year.

According to the International Copper Study Group, world copper mine production shrunk from 1.797 million tonnes in November 2018, to 1.515Mt in February 2019, an 18.6% decrease.

Meanwhile the anticipation of lower interest rates, causing the dollar to fall with them, is currently helping the copper price. The red metal hit a two-month high on Friday, with LME copper finishing up 1.4% at $6,065 per tonne, the best performance since May 10.

Three of the world’s largest investment banks, Morgan Stanley, Citi and Goldman Sachs, have all placed bullish bets on copper this year; Morgan Stanley expects the price to rocket 14% as supply tightens. Citi is predicting a demand surge from China in the second half, as construction completions requiring copper catch up with housing starts.

Aben Resources Ltd (TSX.V:ABN)

Sun Metals Corp (TSX.V:SUNM)

Universal Copper Ltd (TSX.V:UNV)

UNV acquires highly prospective copper block

Universal Copper batting for a double in Colombia

Boreal Metals Corp (TSX.V:BMX)

Max Resource Corp (TSX.V:MXR)

Max pursuing new high-grade gold target and hunting for copper-gold porphyry

Max in the chips at North Choco with high-grade gold/copper

Lithium

Arguably, lithium is the most important metal for electrification. As the main ingredient in lithium-ion batteries that drive EVs, a steady supply of lithium for battery-makers and auto manufacturers is going to be crucial.

Automobile manufacturers are increasingly investing in EV models. Just about all car makers are incorporating EVs into their production mix, and they are calling for public charging infrastructure to accommodate them.

Volvo has banned the internal combustion engine, stating that this year, all new models will be electrics or hybrids. Nissan, JLR, Daimler, BMW, Geely and BYD have made public commitments to EVs.

In North America a very small percentage of the auto market is electric, but elsewhere governments have made deeper commitments. Norway, the Netherlands, France, Germany, UK, China and India have all indicated they will ban cars running on fossil fuels.

Bloomberg says EV sales are expected to increase from 1.1% of the total auto market in 2017, by a factor of 10 by 2025, 27X by 2030 and 50X by 2040. JP Morgan is forecasting electric cars to be 35% of the global market by 2025 and 48% by 2030.

All these EVs will need lithium-ion batteries containing lithium, graphite, nickel and cobalt, plus other mined metals that go into EVs, like copper.

Will there be enough? According to Adamas Intelligence, in February 2019, 75% more lithium carbonate was deployed for batteries in electric and hybrid passenger vehicles compared to February, 2018.

We know that the lithium market, long term, is likely to be in deficit as troubles ramping up production meet a mounting wall of demand.

For more on this read Call for lithium tsunami cancelled

We also know that China produces roughly two-thirds of the world’s lithium-ion batteries and controls most of its processing facilities. This gives China tremendous clout should it decide to deprive the United States of lithium batteries or raw materials, just as the US is planning a mine-to-EV battery supply chain.

But North America has a problem. There is only one producing lithium mine, Silver Peak, run by Albemarle, the world’s largest lithium producer. The grades at Silver Peak are rumored to be declining. There are a number of companies exploring for the element in and around Nevada’s Clayton Valley (including AOTH’s lithium junior pick, Cypress Development Corp. (TSX-V:CYP)) but none has yet advanced to the mine permitting stage. The US is about 70% dependent on foreign suppliers for its lithium. Lithium products from Albemarle’s Silver Peak lithium brine operation in Nevada are sent to its processing plant in North Carolina. This material is then loaded on ships and sent to Asian battery manufacturers, which sell the batteries to automakers.

There is currently no “mine to battery” supply chain in North America, but steps are being taken to address our lithium dependence. The big question is, where are all the North American auto plants, once they get re-tooled for EVs, going to get their batteries from?

IHT Markit thinks electric vehicle sales in the US will smash 1.28 million units by 2026, a whopping 540% increase from the 200,000 sold in 2017, or a CAGR of 30.4%.

Major investments in the hundreds of millions and billions by some of the world’s largest EV automakers and battery-cos give us a good look at what could be a future electric vehicle ecosystem, where batteries are made in the United States possibly even from metals mined in America – like lithium, nickel, cobalt and graphite – then sold to EV makers in the US – likely the southeastern US anchored by SK Innovation’s huge battery plant being built in Georgia.

The announcement a few weeks ago by Schlumberger, the world’s largest oilfield services firm, that the USD$50.5-billion market cap company has invested $2 million for Pure Energy’s (C:PE) lithium brine project in the Clayton Valley, appears to support this thesis.

But the immediate growth is definitely centered around Tesla.

Tesla’s massive lithium battery plant, Gigafactory 1, in Sparks Nevada, was built to supply Model 3 electric motors and battery packs along with Tesla’s energy storage products. Panasonic makes Tesla’s EV batteries; the individual cells are assembled into battery packs for the cars at the Sparks plant.

Elon Musk, Tesla’s CEO, recently talked about plans to ramp up car production and to start mass-producing electric pick-ups and electric Class 8 semi trucks by the end of 2020. Musk added these plans are dependent on Tesla being able to manufacture a lot more lithium-ion battery cells. In fact the luxury car-maker may even try to go it alone without Panasonic.

Tesla skeptics may scoff, but the company apparently is zipping around its competition including the 400-odd electric vehicle manufacturers in China. A report from Toronto-based Adamas Intelligence states that Tesla’s vehicles accounted for 22% of global EV capacity in May, against 18% in May, 2018. The next-best EV maker was China’s BYD, backed by Warren Buffett, at 4% capacity.

Tesla’s head of minerals procurement has said the company expects global shortages of lithium, copper and nickel in the near future.

Once Tesla increases production to a “very high level it will look further down the supply chain and get into the mining business” said Musk.

Cypress Development Corp (TSX.V:CYP)

CYP partners with Lilac Solutions to get 83% recoveries from Nevada claystones

Ahead of the Herd Video Interview with Bill Willoughby CEO of Cypress Development Corp.

Gold

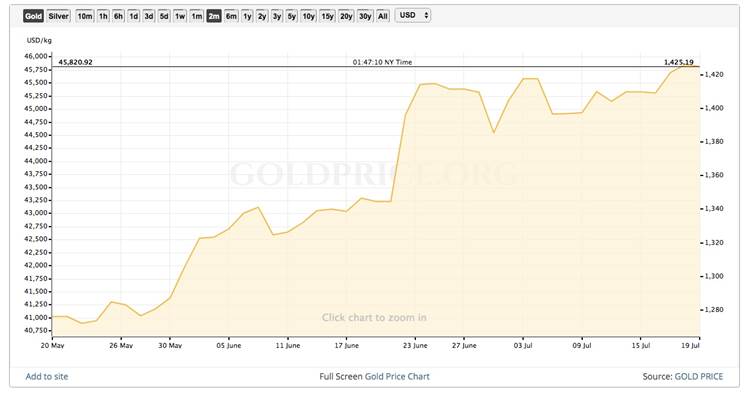

A few weeks ago we wrote that this is The season for gold. At the time, our reasons for being bullish on the “barbarous relic” were mostly to do with negative economic news coming out of the United States, including a bond yield curve inversion, signaling a recession is on its way.

Now it seems every day the gold price breaks a new record – the latest being on Friday, when gold breached a six-year high of $1,452.60/oz. Gold’s current movement is not so much related to economic malaise, but rather, is being judged against bond yields and what the Federal Reserve is going to do next.

The metal used mostly for jewelry and investments is up a rollicking 11%, year to date.

Until June the Fed’s party line was to keep increasing interest rates as long as the economy was hitting the right employment and inflation targets. When prices increased slower than expected, the Fed took a pause. At its last meeting, Fed Chair Jerome Powell strongly hinted that a rate cut – the first in a decade – was coming, which lit a fire under the gold price. Gold investors love low interest rates because that could weaken the dollar, thereby pushing up commodity prices and making dollar-priced investments like gold attractive. The idea of monetary easing causing inflation also appeals to gold investors, since the precious metal is known to hold its value over time versus depreciating fiat (paper) currencies.

The gold price is also being lifted by very low and in some countries, negative interest rates on sovereign debt. If investors have to effectively pay for lending money to borrowers, gold is seen as a better investment. Finally, the price is moving up in response to geopolitical tensions – among them, reports of an Iranian drone being shot down by an American warship.

As for what happens next, all eyes are on the next Fed meeting July 31.

NV Gold Corp (TSX.V:NVX)

NV Gold identifies large, structural target for August drilling

NV Gold swinging for the fences in Nevada

NV Gold chasing high-grade Au in Nevada

Max Resource Corp (TSX.V:MXR)

Max pursuing new high-grade gold target and hunting for copper-gold porphyry

Max in the chips at North Choco with high-grade gold/copper

Boreal Metals Corp (TSX.V:BMX)

Sun Metals Corp (TSX.V:SUNM)

Aben Resources Ltd (TSX.V:ABN)

Aben done drilling at Justin, moves on to Forrest Kerr

Aben drills targeting hi grade gold in Golden Triangle and Yukon

Ahead of the Herd interview with ABN CEO Jim Pettit

Guyana Goldstrike (TSX.V:GYA)

Guyana Goldstrike discovers mineralized outcrops along 1,100m trend

Guyana Goldstrike aims to add ounces at gold-bearing iron formation

Silver

Last week, ruminating about tools we might use to predict what direction gold is going, we decided to take a look at gold ratios, including the gold-silver ratio.

The gold-silver ratio is the amount of silver one can buy with an ounce of gold. Simply divide the current gold price by the price of silver, to find the ratio.

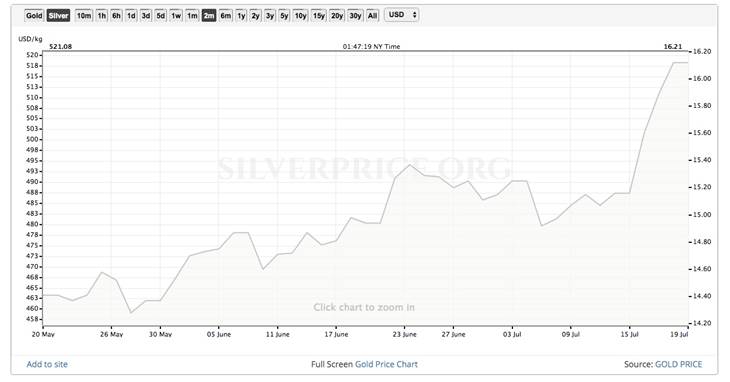

On June 12, the gold-silver ratio hit a 26-year high by breaking through the 90-ounce mark – meaning it took 93 ounces of silver to purchase one ounce of gold. The higher the number, the more undervalued is silver or, to put it another way, the farther gold is pulling away from silver, valued in dollars per ounce.

Given then that silver was so undervalued, one might speculate that now would be a good time to buy under-valued silver. Well low and behold, that is exactly what’s happened.

The chart below shows a major outbreak for “the devil’s metal” (characterized for its volatility). In the last two weeks, silver has shot up from $14.92/oz on July 5, to a close of $16.12 on Friday – a gain of 8%!

Bullion Vault remarked that at $16.10, the gold-silver ratio was down about five points to 88, the lowest in two months. The average ratio over the past 20 years is around 65.

While gold was retreating from Thursday’s six-year high, silver was taking off. On Friday the precious metal hit a 13-month high of $16.62, prompting a colorful commentary from Ross Norman of Sharps Pixley, London’s largest bullion broker:

Rather like the vapours emanating from the Temple of Apollo at the oracle in ancient Delphi, silver’s price action now portends well for gold.

The gold/silver ratio has fallen from 95 to 87 and if you like gold you should positively love silver as there is scope for a further correction.

NV Gold Corp (TSX.V:NVX)

Boreal Metals Corp (TSX.V:BMX)

Richard (Rick) Mills

subscribe to my free newsletter

Ahead of the Herd Twitter

Ahead of the Herd FaceBook

Legal Notice / Disclaimer

This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment. Richard Mills has based this document on information obtained from sources he believes to be reliable but which has not been independently verified. Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as

to its accuracy or completeness. Expressions of opinion are those of Richard Mills only and are subject to change without notice. Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission. Furthermore, I, Richard Mills, assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information provided within this Report.

ABN, BMX, MXR, PDM, UNV, NVX and GYA are advertisers on Richard’s site aheadoftheherd.com. Richard owns shares of ABN BMX, MXR, PDM, UNV, NVX, GYA, SUNM and CYP.

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.