All signs point to gold price strength – Richard Mills

2026.03.14

Inflation, higher interest rates and a strong dollar are bad for gold prices. On the other hand, war, geopolitical stress, bad job reports and stagflation are good for gold.

The consensus on gold prices for 2026 is cautiously bullish, with many analysts expecting the precious metal to consolidate at higher levels.

I believe gold will see resistance at $5,000, with $100-200 moves on either side for the short term at least.

Despite the opposing forces of high interest rates (negative for gold) and severe geopolitical stress (positive for gold), the prevailing view is that structural drivers such as central bank buying, de-dollarization, persistent inflation/ stagflation, interest rate cuts and safe-haven demand will outweigh short-term headwinds.

Central bank buying

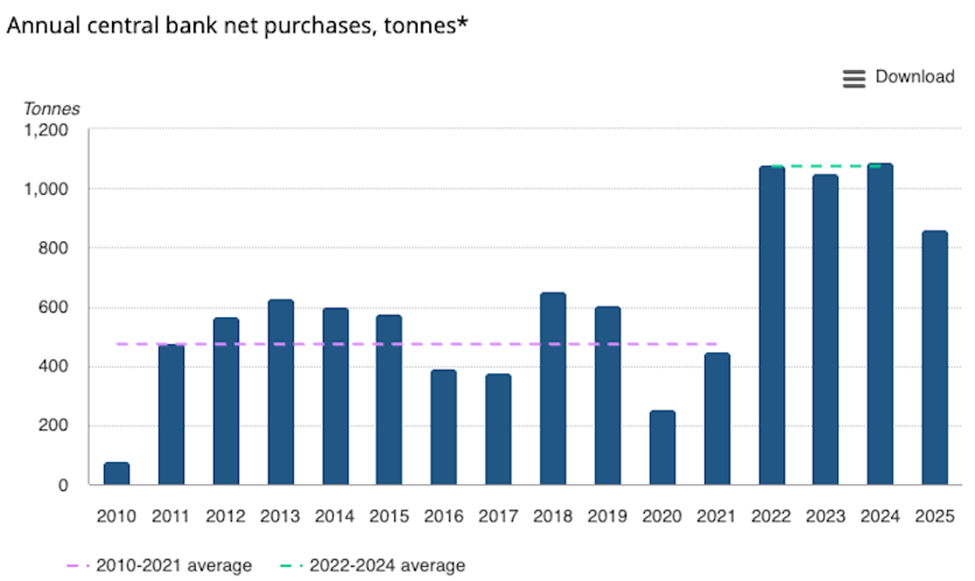

Emerging-market central banks continue to buy gold to diversify away from the US dollar, providing a solid floor for the price.

Net central bank gold demand increased to 230 tonnes in the fourth quarter of 2025, up 6% from 218t in the previous quarter. This strong performance concluded a year marked by durable buying activity, even as gold prices reached record highs, states the World Gold Council.

Twenty-two institutions reported an increase in their gold reserves of around a tonne or more during the year; seven were responsible for the bulk of the gold buying: the National Bank of Poland (+102t), the National Bank of Kazakhstan (+57t), the Central Bank of Brazil (+43t), the State Oil Fund of Azerbaijan (+38t), the Central Bank of Turkey and the People’s Bank of China (+27t), and the Czech National Bank (+20t).

Geopolitical risk

Ongoing conflicts and the “de-dollarization” trend are viewed as long-term, irreversible changes that favor hard assets. The war in Ukraine entered its fourth year this past February; and the threat of China invading Taiwan is back on people’s radar due to the US potentially running out of defensive missiles in the war with Iran that started on Feb. 28. There is also ongoing strategic competition focusing on trade, semiconductors and security, creating high risk for conflict.

The US risks running out of missiles in war with Iran — Richard Mills

Yemen’s Houthi rebels launched multiple missile and drone attacks targeting Israel throughout 2025; North Korea continues to provoke with missile launches; and there is increased volatility in Latin America, particularly with developments in Venezuela.

Stagflation

The war between Iran and the United States/ Israel is worrying investors that it could cause the return of 1970s-style stagflation.

Stagflation occurs when the inflation rate and unemployment remains stubbornly high, and economic growth slows.

If inflation stays high while growth slows, gold’s role as a hedge is expected to shine.

As we’ve previously written, gold does well in stagflationary periods and outperforms equities during recessions.

In six of the last eight recessions, gold outperformed the S&P 500 by 37% on average.

Brent crude has jumped from $67.13 on Feb. 17 to the current $103.86 a barrel, a gain of 54% in less than a month, as the Strait of Hormuz remains closed to shipping. The new Iranian leadership has vowed to keep the key waterway blocked, causing oil prices to spike.

Capital Economics says a useful rule of thumb is that a 5% rise in oil prices adds about 0.1% to developed-market inflation.

High oil prices also dampen economic growth, with the IMF estimating that for every 10% rise in oil prices, global economic output decreases by 0.1 to 0.2%.

The multiplier effects of closing the Hormuz Strait are going to be felt across the globe. It’s not only oil that transits the strait (about 20 million barrels a day), but LNG, distillates like gasoline and jet fuel, sulfur, fertilizer and aluminum. There is also helium, used in high-tech manufacturing processes to produce semiconductors.

All of these commodities are trapped, and their prices are rising fast.

The case for stagflation in the US is bolstered by events at home.

The economy lost 92,000 jobs in February, while the unemployment rate ticked up to 4.4%.

Data released this week showed that CPI inflation in February was sticky, rising 0.3% over January and 2.4% year over year. Of course, Wednesday’s inflation print didn’t capture the effects of the oil price surge this month. The March figure is likely to be considerably higher.

The Personal Consumption Expenditures (PCE) price index — the Fed’s preferred inflation gauge — increased 0.3% in January after rising 0.4% in December, the Bureau of Economic Analysis (BEA) said Friday.

US Treasury yields are rising with oil prices, as traders assess the war’s impact on inflation. On Friday morning the 10-year Treasury had climbed 5 basis points to 4.25% while the 30-year added more than 2 bp to 4.879%.

US manufacturing employment continues to shrink, with the sector losing another 12,000 jobs in February, to 12.57 million, the lowest since January 2022.

Manufacturing employment has contracted in 23 of the last 25 months, the longest losing streak since the financial crisis.

Expect the Iran war to make the manufacturing recession even worse, because higher energy costs will force factories to cut even more jobs.

Speaking of making things worse, Michael Pento, president of Pento Strategies, penned a column in which he stated that The battered US consumer, who was already suffering an affordability problem, is now having to deal with much higher energy prices. Higher energy prices hurt the consumer in two ways. First, the roughly $350 worth of fiscal stimulus per taxpayer from the OBBB [One Big Beautiful Bill Act] is now going to be used to pay utility and gas bills instead of increased discretionary spending. And secondly, the higher inflation caused by spiking energy prices reduces the Fed’s ability to cut interest rates. In other words, the highly anticipated and well-touted fiscal and monetary boost for the economy in 2026 is being cancelled.

Other key points made by Pento:

- On top of this, we have an economy that is no longer creating net new jobs.

- Meanwhile, the credit markets continue to fracture. BlackRock froze $1.2 billion in withdrawal requests from its $26 billion private credit fund.

- The Fed printed $15 billion last week alone just to keep stock prices elevated.

- There should still be a more lasting premium in energy prices even after the war officially ends. This is because the energy dynamic has changed. Much like US sanctions and the confiscation of foreign assets discouraged countries from holding dollars and towards hoarding gold, energy may now be hoarded due to supply fears caused by US aggression in the Gulf.

Interest rate cuts

Rate cuts from the Federal Reserve, as the US labor market keeps softening, are expected to reduce the opportunity cost of holding gold.

The Fed will be keeping a close eye on inflation to decide whether to lower or raise rates. If inflation ticks higher, the central bank may elect to raise rates, which would be bad for stocks, bonds, borrowers and the overall economy, which runs on cheap credit.

The global economy is facing increased risks of “stagflation lite” in 2026, characterized by high inflation, slowing growth, and a softening, but not cracking, labor market. While not universally considered a full-blown crisis yet, conditions in early 2026 show that rising inflation, driven in part by energy costs and geopolitical tensions, is colliding with tepid economic growth, creating a challenging environment for central banks.

Central banks around the world are having to balance the need to curb inflation, by raising interest rates, without causing a severe recession.

The war’s knock-on inflationary effects could dash the market’s expectation of at least two interest rate cuts this year in the US.

In fact, in a dramatic reversal of fortune, they could even rise.

The key questions for us at AOTH is how long the Hormuz Strait remains closed and if the Houthis, Iran’s proxies in Yemen, decide to try and close the Bab el-Mandeb Strait.

The Straits of Hormuz and Bab el-Mandeb are critical global chokepoints, together handling a significant portion of global energy and goods. The Strait of Hormuz transports 20 to 30% of global seaborne oil and one-third of liquefied natural gas (LNG), while the Bab el-Mandeb facilitates a major share of trade through the Suez Canal, handling roughly 30% of global oil and 40% of dry goods.

The Iran war and stagflation — Richard Mills

Yahoo Finance reports Fed officials are expected to hold interest rates steady when they meet later this month, as they did at their gathering in January.

Trade war

Before the US and Israel attacked Iran, gold was enjoying considerable safe-haven demand owing to the economic disorder caused by the Trump administration’s tariffs. This is expected to continue.

Those hoping that the Supreme Court decision striking them down would end the protectionist trade policy will be disappointed.

Trump has found another way to impose import duties, and that is by launching investigations under Section 301 of the Trade Act of 1974.

The administration has reportedly expanded its trade investigations to 60 countries, including Canada.

It also implemented a worldwide 10% levy but that can only stay in place for 150 days without Congressional approval.

InvestorDaily quotes Betashares’ chief economist David Bassanese in saying that tariffs and tighter immigration policy have weighed on both labor demand and labor supply.

“Higher US tariffs have both added to economic uncertainty and consumer prices while reducing corporate profits. The crackdown on illegal immigration – estimated to account for 10 per cent of the workforce – has also reduced labour supply,” he said.

Bassanese said these policies represented negative supply shocks that risked slowing economic growth while simultaneously lifting inflation.

“Raising tariffs while restricting the supply of labour are just the first two of the negative supply shocks US President Trump has imposed on the world’s leading economy. Such negative supply shocks are stagflationary in that they dampen economic activity while also raising prices,” he said.

Gold bucks a trend

Gold observers can, and should, ask a legitimate question: How can gold go up when the US dollar is climbing — as it infallibly does during energy crises — and Treasury yields are increasing?

Remember what I said at the top: inflation, higher interest rates and a strong dollar are bad for gold prices.

Yet we have a historical precedent that bucks this trend. Between 2023 and 2025, driven by massive central bank purchases, geopolitical risks, and distrust in monetary policy, gold broke its traditional inverse correlation to achieve record highs despite the headwinds of a strong dollar and rising US Treasury yields.

The charts below prove this apparent anomaly.

Source: Trading Economics

Source: Trading Economics

According to Institutional Investor and MarketWatch,

While a stronger dollar (which makes gold more expensive in other currencies) and higher yields (which increase the opportunity cost of holding non-yielding gold) typically create an “inverse” relationship, this “new normal” shows that other, more powerful drivers can dominate.

Conclusion

Gold hit an all-time high of $5,370 on Jan. 28. Although it has fallen around $300 since then, the bull market that started in early 2024 is arguably still intact.

Factors feeding into the bull include geopolitical risk, in frightening abundance right now; the ongoing trade war; central bank buying and de-dollarization; the prospect of higher interest rates that will increase the servicing costs on the nearly $39 trillion national debt; and stagflation — an ugly combination of high unemployment, high inflation and low economic growth.

Unless the war with Iran ends soon, stagflation will soon be stalking global economies. Stagflation is bad for stocks, bonds, consumers and manufacturers. The only thing that it’s good for, history has shown, is gold.

Richard (Rick) Mills

aheadoftheherd.com

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.