Automakers seeking greater control over EV battery raw materials like graphite, lithium

June 18, 2021

The auto industry is bleeding from a dearth of semiconductors, used for example in heads-up displays, sensors, cell phone integration, and to enhance engine performance.

According to AlixPartners, a consulting firm, the global chip shortage will cost automakers US$100 billion in lost revenue this year, and affect the production of 3.9 million vehicles.

The chip crunch is attributed to a number of factors. The pandemic prompted semiconductor factories to shut down early last year, particularly in Asia where the majority of processors are made. By the time their economies started to re-open, there was already a backlog of orders to fill. Then, chipmakers were swamped by unforeseen demand, not only for new cars, but personal computers and gaming consoles which also run on micro-chips. Adding to the demand surge, wireless providers clamored for chips to power new 5G networks.

Current vehicles have anywhere from 30 to 50 chips in them.

Losing control over such a vital link in their “just in time” supply chains has caused automakers to look at developing direct relationships with semiconductor manufacturers, something they were reluctant to do in the past because it meant being financially liable for such agreements.

“These things are shocked into existence,” Driving quoted Mark Wakefield, co-leader of AlixPartners’ global automotive practice. “Now the risk is real. It’s not a potential risk of losing production to semiconductor shortages.”

Fortunately, there is a template for them to follow. Driving cites the example of when automakers had supply agreements with producers of palladium and platinum, after a price rise in those raw materials, used in catalytic converters, prompted them to take a more direct approach to their raw materials sourcing.

The same thing is happening now with lithium and graphite — metals that are essential to lithium-ion batteries, which power electric vehicles, grid energy storage systems, and consumer electronics such as smart phones and power tools.

This week Volkswagen announced it is in talks with suppliers to secure direct access to raw materials for EV batteries, including BASF, a large maker of battery ingredients.

A June 15 news article states The world’s second biggest carmaker is trying to exert more control over key components in its supply chain such as semiconductors and lithium so it can overcome any potential bottlenecks and keep its plants running at full capacity.

The company is also trying to catch up with rivals like Tesla and BMW which have already struck supply deals with lithium producers, according to the Reuters story. BMW has an offtake agreement with US lithium manufacturer Livent and China’s Ganfeng Lithium, while Tesla has a five-year lithium hydroxide supply deal with China’s Sichuan Yahua Industrial Group.

“We need to move into vertical integration more strongly, procuring and securing raw materials,” Reuters quotes Thomas Schmall, Volkswagen’s board member in charge of technology.

Schmall said that gaining control of the supply of raw materials for EV batteries, which also includes graphite, cobalt and nickel, is vital to getting a better handle on costs.

“80% of cell costs are determined by raw materials. So it’s obvious that one needs to be more engaged.”

“We’re all in a race. It’s about making the most affordable cells and you need scale to do that,” he added.

The supply of battery metals will likely continue to be a concern for automakers and battery companies, so long as production is concentrated in the hands of so few players and countries. In 2020, the vast majority of mined graphite came from China, while for lithium, Australia and Chile were the top producers.

Meanwhile the demand side of the battery metals market just keeps growing.

$7 trillion opportunity

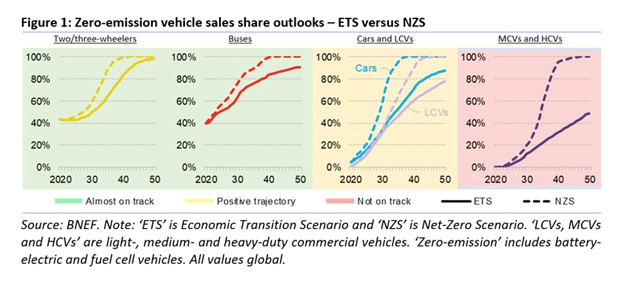

A new report from Bloomberg New Energy Finance (NEF) forecasts sales of zero-emissions cars will accelerate from 4% of the market in 2020, to 70% by 2040. Electric bus sales are predicted to reach 83% market penetration in the same forecast period. Zero-emissions light commercial vehicles will grow from just 1% of the market currently, to 60% in 2040, while medium and heavy commercial vehicles are expected to hit just over 30% market penetration, from almost nil today.

BNEF estimates that electric vehicles represent a $7 trillion global market opportunity between today and 2030, and $46 trillion between now and 2050, states its annual Electric Vehicle Outlook.

GM doubles down

Vehicle makers in North America are especially vulnerable to supply chain interruptions, given that so few battery-metal ingredients are mined here.

In 2020 (and earlier) the only lithium production in the United States was from Albemarle’s Silver Peak brine operation in Nevada.

No natural graphite, needed to make spherical graphite used in the EV battery anode, was mined in the US in 2020. The world’s inferred resources of recoverable graphite exceed 800 million tons, but domestic sources are “relatively small,” states the US Geological Survey.

However, the need for a domestic “mine to EV” supply chain is gaining in importance, starting with US carmakers recognizing they must invest in American battery-making capacity.

General Motors recently said it will increase its investments in EVs, and will build two new battery cell manufacturing plants in the United States by mid-decade.

According to the Detroit Free Press, GM announced this week it will spend $35 billion on EVs and autonomous vehicle technologies by 2025, a 75% increase from its initial commitment in early 2020.

The two new battery plants, whose locations were not disclosed, will add to GM’s partially built plant in northeastern Ohio, where the company’s Ultium Cells LLC will be made, and its Spring Hill assembly plant in Tennessee, where it will manufacture its Cadillac Lyriq electric SUV.

The company has set a goal of selling more than 1 million EVs by 2025, with 30 new electric models expected to come out by that year — a huge uptake from its current two models, the Chevrolet Bolt and Bolt EUV.

GM’s greater commitment to electric vehicles comes hot on the heels of a May announcement by rival Ford, which now expects to spend more than $30 billion on electrification, including battery development, by 2030, compared to its previous target of $22 billion.

Government backing

The concept of a North American EV supply chain is receiving support from the highest levels of government, with the US and Canada planning to execute a home-grown strategy to explore for and mine critical minerals in North America.

In January 2020, the two governments announced the Joint Action Plan on Critical Mineral Collaboration. The agreement would increase production and establish supply chains for numerous critical minerals the US is dependent on for imports.

Ottawa has released a critical minerals list like the list of 35 published by the US in 2017; the 31-metal catalogue includes cobalt, graphite, lithium and rare earths.

Earlier this year, the governments of Ontario and Canada announced a plan to each spend $295 million to help Ford upgrade its assembly plant in Oakville to start making electric vehicles.

At the PDAC mining investment conference in Toronto, Francois-Philippe Champagne, Canada’s minister of innovation, science and industry, said Canada is uniquely positioned to be a global leader in EV manufacturing.

“Canada offers renewably generated electricity, a skilled workforce, a stable and predictable jurisdiction to operate in, the rule of law – a commodity very much in demand these days – and an abundance of the critical minerals needed for the batteries that power electric vehicles,” the minister said.

This week, Canada and the European Union agreed, at an EU meeting in Brussels, to launch a new partnership to secure supply chains for critical minerals and reduce dependence on China.

“To begin with, in order to continue creating good, green jobs for the middle class, we must secure supply chains for critical minerals and metals that are essential for things like electric car batteries, Canadian Prime Minister Justin Trudeau told reporters on Tuesday.

In a joint statement, Canada and the EU said the partnership will focus on enhancing “security and sustainability of trade and investment; integration of raw material value chains; science, technology and innovation collaboration; and environmental, social, governance” criteria.

Governmental support for a mine-to-battery-to-EV supply chain right here in North America, bodes well for exploration companies focused on battery metals.

Lomiko Metals

This includes Lomiko Metals (TSXV:LMR, OTC:LMRMF, FSE:DH8C), exploring for graphite and lithium in the Canadian province of Quebec.

Lomiko’s flagship project is the La Loutre flake graphite property, located 117 km northwest of Montreal, and 53 km east of Imerys Carbon and Graphite’s Lac des Iles mine.

Originally explored for base and precious metals, historical reports showed graphite to be present on the property in quartzite and biotite gneiss, and in shear zones where the graphite content ranges from 1-10% on surface including visible flakes. A recent grab sampling and mapping program confirmed a graphite-bearing structure of approximately 7 km by 1 km, with results up to 22% graphite in multiple parallel zones 30m to 50m wide. Another 2 km x 1 km area consisting of multiple parallel zones, 20m to 50m, includes up to 18% graphite.

The property already has a resource of 18.4 million tonnes carbon flake graphite (Cg) grading 3.19% in the indicated category, and 16.7Mt @ 3.75% inferred. Using a 3% cut-off grade, the resource amounts to 4.1Mt @ 6.5% Cg indicated, and 6.2Mt @ 6.1% inferred.

Lomiko is currently working on a preliminary economic assessment (PEA) at La Loutre, and in 2019 completed a drill campaign at the EV Zone. Highlights from the 21-hole, 2,985-meter program featured 7.74% Cg over 135.60m, including 16.81% Cg over 44.10m; 17.08% Cg over 22.30m and 14.80 Cg over 15.10m; and 14.56 Cg over 110.80m.

The new PEA will include the latest results from both the Graphene-Battery and the EV zones.

“La Loutre has proven to be a large and high-grade area worthy of further investment,” stated A. Paul Gill, CEO, in the March 4, 2021 news release. “The only operating graphite mine in North America is the Imerys Graphite & Carbon at Lac-des-Îles, 53 km northwest of La Loutre which reported proven reserves of 5.2M tonnes at a grade of 7.42% Cg in July 1988 before the start of production.”

Earlier this year Gill referenced President Biden’s above-mentioned review of US supply chains including EV batteries, with respect to its nearest neighbor, Nouveau Monde Graphite, being “recently provided a mine permit which bodes well for other groups in Quebec such as Lomiko,” he stated in the Feb. 26 news release. “Although we are only starting our development process, it is good to know there has been nearby success.”

Lomiko has also made progress recently with the project’s metallurgy. A metallurgical flowsheet development program was carried out on samples from both the Graphene Battery Zone and the EV Zone. The program culminated in a locked cycle test (“LCT”) that generated a combined concentrate grading 97.8% total carbon at 93.5% graphite recovery — meeting the program’s objective of upgrading La Loutre mineralization to at last 95% total carbon.

“These very encouraging results of initial testing suggest that La Loutre graphite may be suitable for high-end industrial use,” Gill stated in the April 7 news release.

Conclusion

Lomiko Metals is cashed up and ready to go to work. On May 18 the company closed the first tranche of a $1.162 million private placement. Net proceeds from the $0.17 flow-through financing will go towards exploration on its Quebec properties.

With big car companies like GM and Volkswagen increasing their investments in electrification, and the governments of Canada, the US and the EU all agreeing on the need to collaborate on EV raw material supply chains, and to reduce their dependence on China, Lomiko’s timing couldn’t be better.

Lomiko Metals Inc.

TSXV:LMR, OTC:LMRMF, FSE:DH8C

Cdn$0.13, 2021.06.17

Shares Outstanding 76.5m

Market cap Cdn$27.9m

LMR website

Richard (Rick) Mills

aheadoftheherd.com

subscribe to my free newsletter

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.

Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.

Any AOTH/Richard Mills document is not, and should not be, construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

AOTH/Richard Mills has based this document on information obtained from sources he believes to be reliable, but which has not been independently verified.

AOTH/Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness.

Expressions of opinion are those of AOTH/Richard Mills only and are subject to change without notice.

AOTH/Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission.

Furthermore, AOTH/Richard Mills assumes no liability for any direct or indirect loss or damage for lost profit, which you may incur as a result of the use and existence of the information provided within this AOTH/Richard Mills Report.

You agree that by reading AOTH/Richard Mills articles, you are acting at your OWN RISK. In no event should AOTH/Richard Mills liable for any direct or indirect trading losses caused by any information contained in AOTH/Richard Mills articles. Information in AOTH/Richard Mills articles is not an offer to sell or a solicitation of an offer to buy any security. AOTH/Richard Mills is not suggesting the transacting of any financial instruments.

Our publications are not a recommendation to buy or sell a security – no information posted on this site is to be considered investment advice or a recommendation to do anything involving finance or money aside from performing your own due diligence and consulting with your personal registered broker/financial advisor.

AOTH/Richard Mills recommends that before investing in any securities, you consult with a professional financial planner or advisor, and that you should conduct a complete and independent investigation before investing in any security after prudent consideration of all pertinent risks. Ahead of the Herd is not a registered broker, dealer, analyst, or advisor. We hold no investment licenses and may not sell, offer to sell, or offer to buy any security.

Richard does not own shares of Lomiko Metals Inc. (TSXV:LMR). LMR is a paid advertiser on Richards site aheadoftheherd.com

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.

{kind=link}