Mining industry risks another lost decade – Richard Mills

2023.09.06

Mining — like any other sector — has experienced its fair share of issues over the past decade, holding back its overall reputation and efficiency.

Now faced with the formidable challenge of supplying enough minerals for the global energy transition, the industry has to dig deep — both literally and metaphorically — to improve its performance.

However, the root of the problem is multifaceted, and headwinds are coming from all sorts of directions. Among the key issues include a global skills shortage, environmental and human rights concerns, as well as the availability and use of funding.

Until those are addressed, the value of mining won’t be maximized, and the industry will likely suffer the same fate for the next ten years.

Below, we take a look at each of the major obstacles to the long-term sustainability of mining, and what the industry has (or hasn’t done) to mitigate these risks.

Critical Skills Gap

One of the biggest challenges facing the mining industry is a growing skills gap created by an aging workforce and a dearth of talent waiting next in line.

According to Walter Copan, VP Research and Technology Transfer at Colorado School of Mines, the mining industry is facing a critical skills gap, compounded with the so-called ‘grey tsunami’ impending with regard to the amount of retirements anticipated.

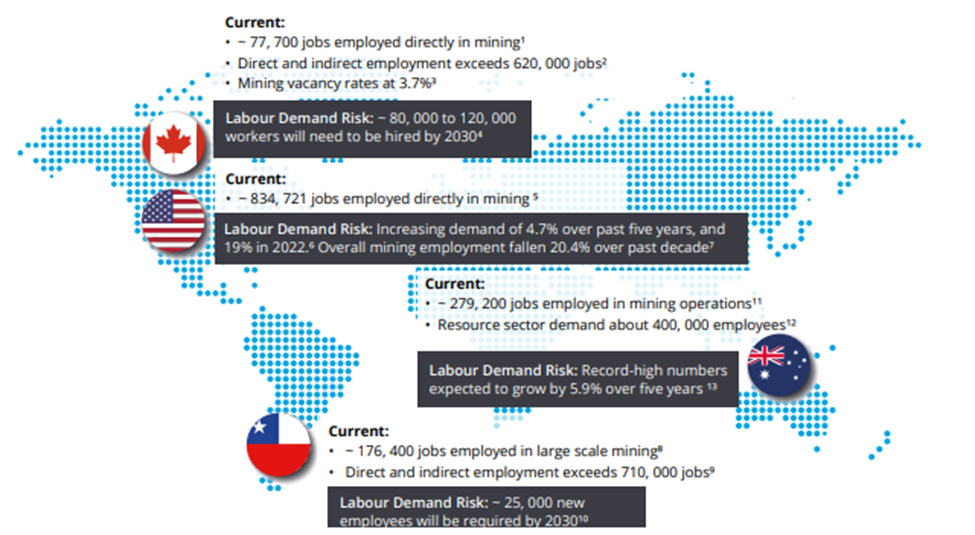

A study put out by Deloitte earlier this year revealed that nearly 50% of skilled mining engineers are reaching retirement age within the next decade. Many mine workers are at least 46 years and older.

Moreover, the study found that overall mining employment has fallen 20.4% over the past decade in the United States. In Canada, approximately 80,000 to 120,000 workers will need to be hired by 2030.

“Mining, mineral processing and then the downstream production of the materials that we rely upon for all aspects of the energy sector [are] at risk because of these shortages, and I find the statistic staggering that we are anticipating a retirement of more than half of the US mining workforce over the next six years, that’s 221,000 workers that are expected to retire by 2029,” Copan said in a June testimony before the House Committee on Natural Resources.

The bigger problem for the industry though, is a shortage of new talent to replace the old when the time comes. According to Copan, the pipeline of people servicing the sector from the leadership level to engineering and extractive metallurgy are being replaced only at a trickle in the United States, Canada, Australia and in Europe.

The industry’s age curve is quite apparent at the upper management level. Within the past year or so, we’ve seen several prominent names within the industry depart, none bigger than Teck Resources’ Don Lindsay, who announced his retirement after 17 years leading the Canadian miner. Others who have retired since are Sandeep Biswas, who was CEO of Newcrest Mining for eight years, and Wesdome Gold Mines chief executive Duncan Middlemiss.

Industry Losing Appeal

Copan, as many of the industry’s prominent figures had done in the past, also voiced concerns about the future of the talent pipeline. He noted that academia has seen a decline in programs related to mining, engineering, and extractive metallurgy.

“This industry has lost its luster, with regard to being attractive to the next generation of leaders at all levels in the sector and the lack of interest in the geosciences more broadly,” he stated. “It is doubly concerning because as we look at the reliance of this world on the materials that are sourced from the Earth’s crust, the entire mining sector is key to the energy transition.”

In regions like Canada and the US, enrollment or graduation from university courses related to mining engineering has been slipping in recent years.

As noted in a recent Bloomberg article, fewer students now want to be geologists or engineers, partly due to mining’s negative image regarding pollution, human rights and gender equality. That’s leaving the industry with an aging workforce and forcing it to recruit from outside the traditional university talent pool, such as through apprenticeship programs and internal training.

At the Colorado School of Mines, total enrollment in mining, geophysical and geological engineering undergraduate degree courses last year was down about 35% from almost a decade ago. In Canada, mining and mineral engineering graduates dropped by a third between 2016 and 2020, according to Statistics Canada.

It’s a similar story at the UK’s prestigious Camborne School of Mines, traditionally an important feeder school for the global industry. The number earning degrees from its undergraduate mining engineering course fell in recent years, with new intakes halted in 2020. The school this year announced new programs for mining employees.

UK mining faces a big challenge to meet its needs, according to Rhys Morgan, an engineering and education director at the Royal Academy of Engineering. Some 80% of the 1,250 mining engineers registered with the UK’s Engineering Council are over 50, and 40% are at least 60, he said.

“There’s been a bit of a lost decade in people going through university in mining courses — that’s proving to really come to crunch point now,” said Alison Allen, deputy managing director at UK-based mining consultancy Wardell Armstrong. “There are too few graduates filling needs.”

A talent squeeze within the mining industry had previously been cited by a 2022 McKinsey Global Institute survey, in which 86% of mining executives said it’s harder to recruit and retain talent versus two years ago—particularly in specialized fields such as mine planning, process engineering, and digital (data science and automation).

Also, 71% of the mining leaders said the talent shortage is holding them back from delivering on production targets and strategic objectives.

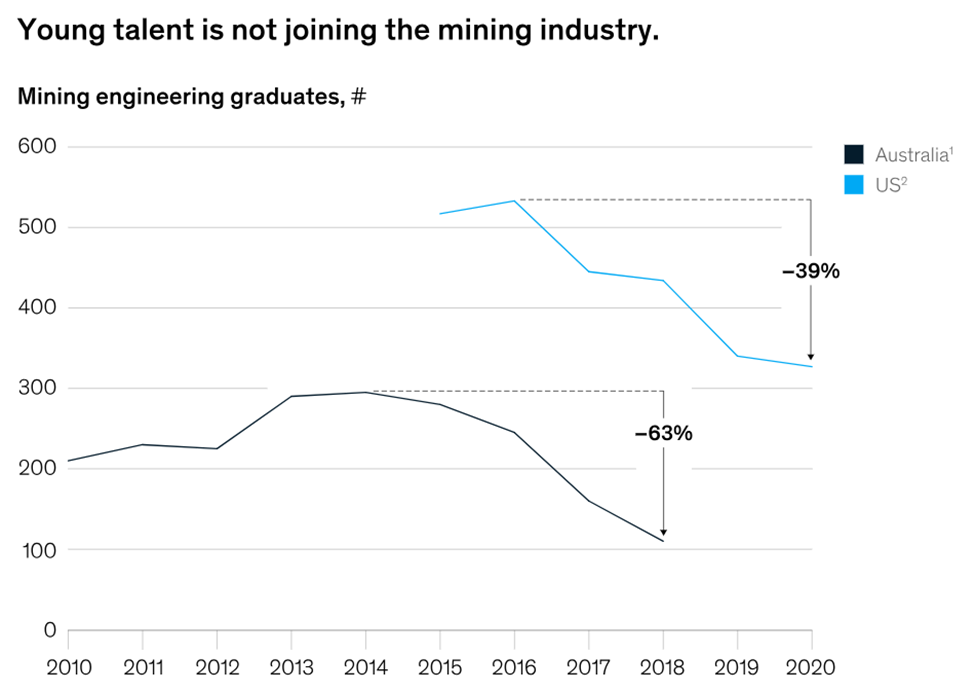

Mckinsey analysts expect this trend to continue. “Mining is not currently an aspirational industry for young technical talent to join: there has been around a 63% drop in mining engineering enrollment in Australia since 2014, and a 39% drop in mining graduations in the United States since 2016,” it found.

In its report, the research firm refers to the numerous structural challenges associated with the industry that are preventing mining companies from attracting and retaining talent.

“For the large number of mines that are remote, we observe a set of additional significant structural challenges, such as lack of sophisticated infrastructure (hospitals, schools, entertainment) and therefore lower family friendliness. Equally, there is the perception that the work is physically demanding and hazardous.

“Then, once talent has been attracted and employed, additional pain points often include uninspiring capability development (beyond standard occupational training), limited or vaguely defined career progression pathways beyond middle-management layers, and insufficient levels of diversity and inclusion,” McKinsey wrote.

“Such issues have been historically associated with mining—what’s changed today, however, is that more recent macro trends have brought these challenges into sharper relief. These trends include a greater focus on challenges for minorities and women in mining, Gen Z’s expectations to have purpose at work, an increasing disconnection between what workers want and managers provide, and competition for digital and technical talent among all industries,” it added.

Consequently, the employee value proposition (EVP) in mining has started to deteriorate and this is showing up in industry data, with demand outstripping the supply of mining talent.

Resource Nationalism

Rising political tensions across the world are also proving to be a tough challenge for the mining industry to navigate.

According to the World Economic Forum: ”The geopolitics of natural resource access and management is critical for the metals and mining sector. Geopolitical tensions affect demand-side indicators. Conflicts can lead to a decline in demand for new investments and, therefore, the demand for raw materials.”

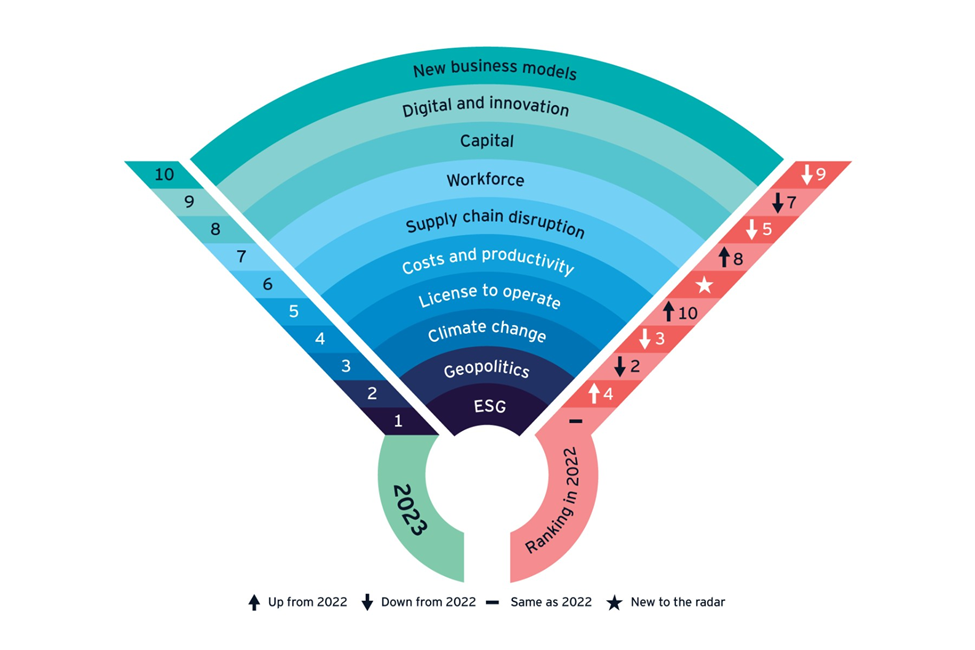

In EY Canada’s most up-to-date ranking of risks disrupting the mining industry, it has geopolitics in 2nd place, up two places from the 2022 list (see below).

In mining, political instability often manifests itself in the form of resource nationalism, which is loosely defined as the tendency of people and governments to assert control, for strategic and economic reasons, over natural resources located on their territory. It is often described as a backward form of state protectionism.

Miners are easy targets because mining is a long-term investment and one that is especially capital-intensive. Mines are also immobile, so mining companies are at the mercy of the countries in which they operate. Outright seizure of assets happens using the twin excuses of historical injustice and environmental or contractual misdeeds. There is no compensation offered and no recourse.

Governments may also get in the way of miners’ progress by implementing anti-mining agendas and/or thinking up new ways to hit the extractive industry with higher taxes.

A 2021 report by Verisk Maplecroft identified an increasing risk of resource nationalism in as many as 34 countries around the world. Countries now rated “extreme risk” include major African copper producers Zambia and the DRC.

According to the global risk consultancy, countries most at risk are those dependent on the minerals or hydrocarbons they export, and mining jurisdictions that have suffered significant economic contraction as a result of the coronavirus. These places are more likely to try and recoup their financial losses by targeting the mining industry in their countries.

In its report, Maplecroft says there is an increasing trend of “state interventionism, creeping expropriation, and indigenization” — interventionist measures that are more subtle than, say, outright nationalization or large tax increases imposed on foreign mining or energy companies.

In Latin America, the firm points to two influences behind resource nationalism. The first is ideologically driven, such as Argentina’s nationalization of Repsol’s interest in YPF; and the second is increased pressure from communities to exert greater control over their mineral resources. The latter is best personified by Chile. Triggered by the worst social unrest in a generation, anchored in rampant inequality, the country reportedly has just elected an assembly that will place responsibility for writing a new constitution in the hands of the left wing.

The reforms could give more power to indigenous communities and expand water rights, including a potential ban on mining in areas where there are glaciers, along with increased state ownership of water desalinated by mining companies.

Zambia made it into Maplecroft’s riskiest places to operate in due to an attempted liquidation of Konkola Copper Mines, whereas in the Democratic Republic of Congo, the Congolese government in 2018 raised taxes on mining firms and increased royalties. The country is Africa’s biggest producer of copper and cobalt.

One explanation of why resource nationalism has picked up in recent years has to do with globalization. During the 1970s and 80s it was common to see developing world governments nationalizing industries. However when globalization emerged in the 1990s, there was a need for foreign investment as governments privatized industries, resulting in fewer attempts to seize foreign-owned assets like mines and factories.

This changed when governments in Latin America, primarily, saw mining profits moving out of the country and they sought to seize greater control over their mineral wealth.

According to a report by Clifford Chance, a law firm, drivers of resurgent resource nationalism in the 21st century include:

- Over-dependence on natural resources.

- Fast-growing populations whose social, educational and health needs are not being satisfied.

- Evolving politics. A government that comes to power on a nationalist platform or that is more critical of foreign investment may be more likely to change the terms of foreign investment.

- The need for jobs.

- The lack of infrastructure and social services.

- Outdated or inappropriate laws.

- A lack of transparency in the licence and concession award process.

- Exploitative contracts. Some foreign investors have taken advantage of political instability, corruption or a kleptocratic state to negotiate terms that are often opposed by the population or a new government.

- High commodity prices and competition for a depleting supply of natural resources.

These factors can create pressure on a state to increase its “take” from its natural resources, it said.

By no means a new phenomenon, some of the ways that countries nationalize resources are through direct expropriation; increasing taxes or royalties foreign miners pay; terminating or suspending licenses/ permits they need to operate; and imposing new and often expensive regulations.

ESG Concerns

While ESG (environmental, social and governance) is a relatively novel term in the mining world, the underlying issues represented by each letter have been ever-present throughout its history.

The mining sector has long struggled with some poor environmental and social legacies that have impacted its ability to recruit young talent and attract investments. Recent high-profile cases such as the tailings dam collapse in Brazil and sexual assault at Rio Tinto’s Australian mines illustrate that the industry is still facing an uphill battle to repair its reputation to this day.

In recent years, ESG has been brought to the forefront as mining investors begin to look beyond financial statements and now want to consider the ethics, competitive advantage and culture of a mining organization.

When S&P Global released its first scorecard for metals and mining companies in 2020, it found that the mining industry has “well-above-average” exposure to environmental risks, resulting from land use, waste, pollution and water usage. Since then, the emphasis on ESG has only grown bigger.

According to EY Canada, ESG remains the top risk and opportunity for mining and metals companies in 2023. The issue is now firmly integrated within corporate strategies due to its impact on almost every aspect of operations.

Some of the greatest areas for ESG improvement are not new, EY said. Improving diversity, equity and inclusion is still a major challenge, and mine closures and rehabilitation require a longer-term, more strategic view.

But ESG is evolving, requiring miners to consider different issues and broaden their capabilities to manage them effectively, the firm added. For example, water stewardship and biodiversity are fast becoming urgent priorities amid a changing climate. Stakeholders expect miners to better assess risks and opportunities, and articulate these through transparent, outcome-based measurement and assurance.

Despite multiple industry initiatives and new standards set up in recent years, serious social and environmental issues continue to plague the sector. The Business & Human Rights Resources Centre (BHRRC), which monitors human rights abuses against local communities and indigenous peoples and environmental impacts of mining, documented close to 500 allegations of human rights abuses related to the extraction of six key transition minerals over the past ten years.

Over two-thirds of recorded allegations are against 12 companies, which are among the largest and most well-established of the extractive sector, including Grupo Mexico, Codelco, BHP, Anglo American and Glencore. One-third (148) of all allegations of abuses involve attacks on those defending the environment or communities.

Most of these were not standalone events, according to the BHRRC researcher Caroline Avan. “There was a continuum between land rights, in particular, and attacks on those defending them, particularly in relation to the rights of indigenous peoples to give free prior and informed consent for the exploitation of their lands,” she said in an interview with Reuters.

“A leading category of abuse is in relation to the environmental damage of extraction, in particular with regard to access to water, either in terms of quantity or pollution,” she says. “The situation is not getting better; as a matter of fact, the frequency of allegations of abuse has actually increased, given the rapid expansions of mining projects relating to the energy transition,” she added.

Decline in Capital Spending

A direct consequence of these risks associated with the sector is an overall lack of investment in mineral exploration. Understandably, investors’ standards are continuing to rise, as seen with ESG, and now it’s not always about the bottom line.

This is why, despite enjoying strong balance sheets and healthy margins, the mining industry is coming off almost ten years of underinvestment.

According to the Prospectors & Developers Association of Canada (PDAC), 2022 marked a reversal of money flowing into the mineral industry from virtually every global source as equity financing was down 50% from the nearly $35 billion raised in 2021. Canada appears one of only few countries holding up as well or better than the other major marketplaces around the world.

In addition, the amount of both equity and debt invested into the mineral industry dropped by a substantial amount in 2022, following along with declining economic conditions and broader market slowdown seen throughout the year, PDAC found.

In an analysis of the industry’s challenges over the next decade, McKinsey highlighted the existing dichotomy between the market capitalization of top mining companies, which climbed by some 40% from December 2019 to December 2021, and capital spending, which is traveling in the other direction.

Globally, capital expenditures in mining fell from approximately $260 billion in 2012 to $130 billion in 2020 (corresponding to 15% and 8% of industry revenues, respectively), the consultancy found.

This change in circumstances is even more apparent relative to the situation in 2016: As commodity prices declined from 2012 to 2016, most mining companies focused on reducing capital expenditures, fixing balance sheets, and controlling costs. Since 2016, absolute capital expenditures have risen, but relative to cash flows from operations levels of capital expenditure are still modest.

This, according to McKinsey, suggests that although growth is once again on their agendas, executive teams and boards remain cautious about using large-scale capital projects to fuel growth.

The firm also noted that while capital expenditures for the top 50 miners are expected to rise to $84 billion in fiscal year 2022, which is 30% higher than 2019’s level, it would still be around 30% below the peak capital spending of $125 billion in 2013.

On average, top miners have deployed around 70% of their cash flow from operations as capital expenditure while setting dividends at around 20%. Meanwhile, according to an analysis of McKinsey’s Mining Productivity Index, productivity has recently improved but is still some 25% below levels achieved in the mid-2000s, it added.

Moving forward, McKinsey analysts pointed to the transition to a net-zero economy as a key driving force behind further investments, and it will be up to the industry to rise up to the challenge.

“In certain technology-transition and supply-ramp-up scenarios, we could see copper demand exceeding supply by 5 million to 8 million metric tons and nickel by 700,000 to 1 million metric tons by 2030. For those two commodities alone, we estimate that meeting demand growth could require $250 billion to $350 billion cumulative capital expenditure by 2030 to grow and replace depletion of currently existing capacity,” McKinsey analysts wrote.

“In that context, given the inability of mining supply to respond rapidly, managing mining operations will become increasingly complex.”

Corruption & Misuse of Funds

But even if the investments grow, no one can guarantee they will be used in the right place. Sadly, misappropriation of funds is rife within the mining industry, highlighting the weakness of oversight and institutional structure in many parts of the world.

Recent examples include an audit of SolGold that revealed as much as $4.6 million spent by the Ecuador-focused miner between 2017 and 2021 was “misappropriated”, alarming its big shareholders such as BHP and Newcrest. SolGold’s Cascabel project is considered one of the world’s lowest-cost, lowest-carbon copper mines.

Two years ago, the Northern Territory government and Glencore’s massive lead-zinc mine were accused of misusing millions of dollars set aside for the benefit of traditional owners. Back in 2007, a community benefits trust totalling $32 million was set up as a condition of expanding the McArthur River mine operation, yet it was alleged that most of the money went into government infrastructure projects.

In Utah, a coalition of environmental groups was calling for a federal investigation, alleging that the Governor’s Permanent Community Impact Fund Board misused more than $109 million in taxpayer dollars to fund fossil fuel projects over the needs of rural communities.

Simply put, mining-related corruption is everywhere, many of which go unnoticed or unreported. This, which is tied to individual risks associated with jurisdictions, remains a key challenge for the industry, especially as the stakes rise with the value of minerals.

Richard (Rick) Mills

aheadoftheherd.com

subscribe to my free newsletter

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.

Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.

Any AOTH/Richard Mills document is not, and should not be, construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

AOTH/Richard Mills has based this document on information obtained from sources he believes to be reliable, but which has not been independently verified.

AOTH/Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness.

Expressions of opinion are those of AOTH/Richard Mills only and are subject to change without notice.

AOTH/Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission.

Furthermore, AOTH/Richard Mills assumes no liability for any direct or indirect loss or damage for lost profit, which you may incur as a result of the use and existence of the information provided within this AOTH/Richard Mills Report.

You agree that by reading AOTH/Richard Mills articles, you are acting at your OWN RISK. In no event should AOTH/Richard Mills liable for any direct or indirect trading losses caused by any information contained in AOTH/Richard Mills articles. Information in AOTH/Richard Mills articles is not an offer to sell or a solicitation of an offer to buy any security. AOTH/Richard Mills is not suggesting the transacting of any financial instruments.

Our publications are not a recommendation to buy or sell a security – no information posted on this site is to be considered investment advice or a recommendation to do anything involving finance or money aside from performing your own due diligence and consulting with your personal registered broker/financial advisor.

AOTH/Richard Mills recommends that before investing in any securities, you consult with a professional financial planner or advisor, and that you should conduct a complete and independent investigation before investing in any security after prudent consideration of all pertinent risks. Ahead of the Herd is not a registered broker, dealer, analyst, or advisor. We hold no investment licenses and may not sell, offer to sell, or offer to buy any security.

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.