5 Reasons the US Dollar Will Head Lower – Richard Mills

2023.03.27

Given its role as the world’s primary reserve currency, the importance of the US dollar in the global economy cannot be understated. It’s estimated as many as 90% of all international trades involve the greenback.

As with commodities, its value abides by the law of supply and demand, moving up or down as trades happen around the clock.

For over a decade, the general movement of direction was up, as a confluence of economic and political factors repeatedly drove up the demand for the currency. At the end of 2022, the dollar was even trading at 25% above its fair value level as measured by purchasing power parity, according to RBC Wealth Management.

In late September, the US dollar index – which is measured against six other peers – touched its highest in 20 years, the sign of a true long-term bull market.

But just like macroeconomy, the US dollar moves in cycles as it reflects the health of the American economy. A few months into 2023, it now appears that this decade-long bull cycle is nearing an end. Over the past five days, the dollar index has seen a 2% hit, down to its lowest since January.

What comes next will likely be years of downturn for the dollar. This is for several reasons.

- Peaking Interest Rates

First and foremost, it’s natural to pinpoint the dollar’s performance in 2022 to the interest rate hikes by the US Federal Reserve to combat inflation.

There’s ample historical evidence suggesting that interest rates and the US dollar tend to move together, as higher rates make greenback-denominated assets more attractive to foreign investors.

Since this time last year, the US central bank has already gone ahead with as many as NINE rate hikes, which has boded well for the dollar. But after this week’s rate hike, the Fed was non-committal on future increases, and insinuated that hikes are nearing an end.

Based on the Fed’s own projections, rates are likely to peak at 4.75% to 5% this year, with just one more rate hike to go, which represents a departure from its previous statements of “ongoing increases” to bring down inflation.

Once that peak is reached, the dollar may very well hit its reverse gear soon after.

Economists at ING are expecting the dollar to come under more pressure based on the latest Fed comments. “With a market not trusting the more ambiguous Fed communication and the US regional banking crisis far from resolved, it looks like investor bias on the Fed may stay on the dovish side,” they said.

- Banking Crisis Fears

While the market keeps its eye on the Fed’s next move, a ripple effect is being felt in the global banking system that could pose further questions for the dollar’s short-term prospects.

It’s hard to ignore what impacts the recent Silicon Valley Bank fiasco — the second-largest bank collapse in American history — would have on the economy, and by association, the dollar.

Some may view this as a one-off event, the product of a bank’s own negligence, but the implications could be much wider. And it’s not a coincidence that the greenback’s string of losses comes right after the SVB collapse.

For a long time, the US dollar has been considered a “safe haven” for investors, but the fear of more bank runs and lenders failing has created second thoughts amongst them. A loss of confidence in the banking system is probably not good for the value of currency.

One analyst quoted by Business Insider said “the turmoil has chipped away at the dollar’s long-established status as a haven currency that can be confidently held by investors during times of volatility.”

“The US dollar and the Swiss franc are easily the weakest of the majors,” Westpac Bank strategist Sean Callow told CNBC’s “Street Signs Asia” this week.

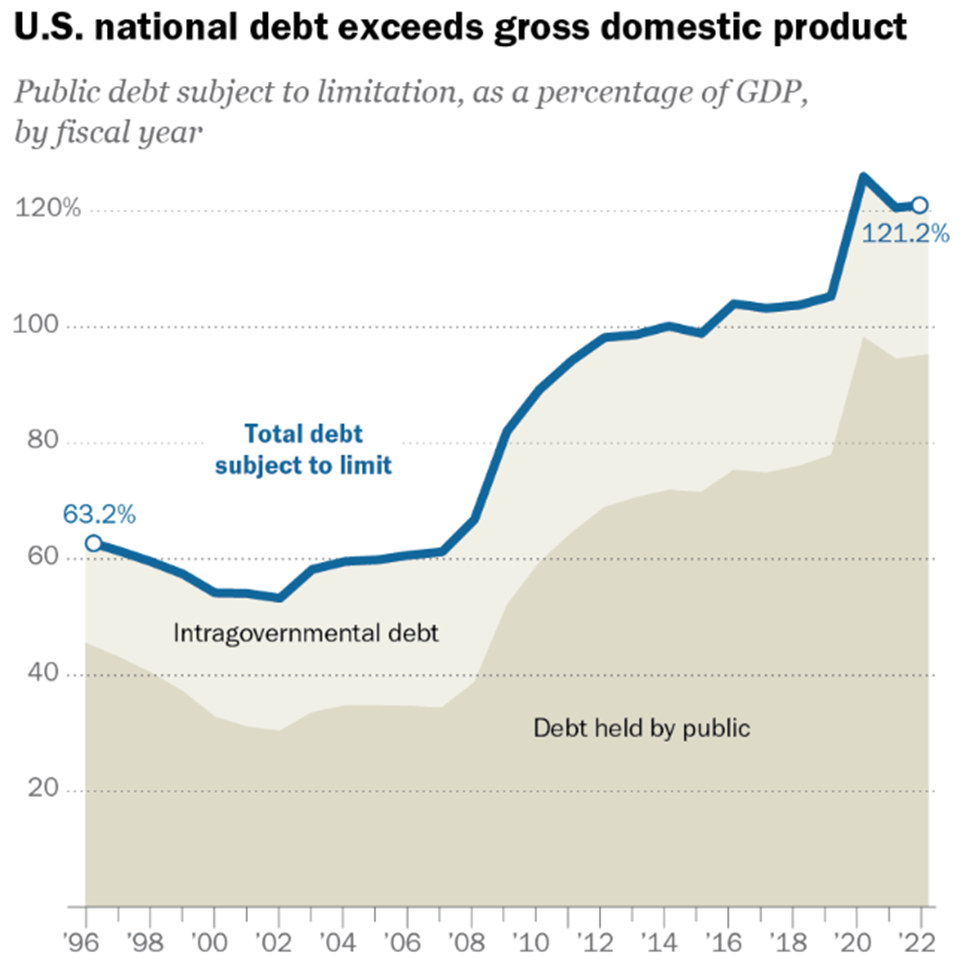

3. Potential National Debt Default

Despite the low likelihood of actually happening, the thought of the US government defaulting on national debt could cause anxiety amongst investors. Since the pandemic, the US has been racking up on its debt to fund various spending programs to the point that its debt-to-GDP ratio at one point hit a record high.

In 2023, that unprecedented amount of spending could well haunt them, fueled by the ongoing friction between President Joe Biden and the Republican-controlled House of Representatives over certain policies on national debt; Biden wants to raise the debt limit, whereas the Republican side wants the former to accept spending cuts.

Without a deal, the federal government could very well default as early as this July, according to the nonpartisan Congressional Budget Office.

While some take this as “a game of chicken” with one side eventually folding, the problem of rising debt still lingers. In a new Pew Research Center survey about the public’s policy priorities, 57% of Americans have cited reducing the budget deficit as a top priority for the president and Congress to address this year, up from 45% a year ago.

The concerns over debt, coupled with the recent banking collapse, would raise the stakes of further economic uncertainty, thus undermining the US dollar’s position as the primary reserve currency.

4. Central Bank Diversification

Another problem for the dollar is that it’s not just investors who are having concerns. Global central banks too are starting to question the dollar’s worth on the international stage.

This is because the US has been too “trigger-happy” when it comes to the use of sanctions and other economic punishments. As a result of these drastic measures, some central banks may now decide to diversify their portfolio of foreign reserves instead of relying heavily on the US dollar, the Institute for the Analysis of Global Security said.

According to Gal Luft, co-director of the Washington-based think tank, one in 10 countries in the world is now under some form of US sanctions. “That has a cumulative effect and as a result, we see the dollar playing less and less of a role and portfolios of central banks,” Luft said.

These comments come right after a Wall Street Journal report that Saudi Arabia is in accelerated talks with China to accept yuan instead of dollars for oil that Beijing buys.

Oil is typically priced in US dollars, and that has allowed Washington to run “huge deficits,” Luft told CNBC’s “Street Signs Asia” earlier this week. Sanctions, however, make governments want to move away from the dollar, he said.

5. Severe Overvaluation

The final reason why we won’t see a higher US dollar this year is simply that the greenback has been overvalued by the market. According to market veteran and former Morgan Stanley Asia chair Stephen Roach, the US dollar has been the most overvalued major currency in the world for quite some time.

Major investment banks like Goldman Sachs are also echoing a similar sentiment based on the dollar’s strong performance in 2022. “On a valuation basis, the dollar does look overvalued. Maybe not quite as overvalued as previous peaks but not that far from those levels either,” analysis by Goldman found.

Given the dollar’s overvaluation, Citibank’s wealth management arm in Hong Kong is predicting the DXY to fall to 96.87 in six to 12 months, and dip slightly lower to 96.61 in the long term.

Analysts at HSBC are also bearish toward the US dollar trend. In their forecast, they said: “We believe the USD will weaken further in 2023, as its significant overvaluation (based on the real effective exchange rate (REER)) can no longer be supported, once the Fed stops hiking, global growth shows signs of troughing and market volatility comes down.

Richard (Rick) Mills

aheadoftheherd.com

subscribe to my free newsletter

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.

Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.

Any AOTH/Richard Mills document is not, and should not be, construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

AOTH/Richard Mills has based this document on information obtained from sources he believes to be reliable, but which has not been independently verified.

AOTH/Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness.

Expressions of opinion are those of AOTH/Richard Mills only and are subject to change without notice.

AOTH/Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission.

Furthermore, AOTH/Richard Mills assumes no liability for any direct or indirect loss or damage for lost profit, which you may incur as a result of the use and existence of the information provided within this AOTH/Richard Mills Report.

You agree that by reading AOTH/Richard Mills articles, you are acting at your OWN RISK. In no event should AOTH/Richard Mills liable for any direct or indirect trading losses caused by any information contained in AOTH/Richard Mills articles. Information in AOTH/Richard Mills articles is not an offer to sell or a solicitation of an offer to buy any security. AOTH/Richard Mills is not suggesting the transacting of any financial instruments.

Our publications are not a recommendation to buy or sell a security – no information posted on this site is to be considered investment advice or a recommendation to do anything involving finance or money aside from performing your own due diligence and consulting with your personal registered broker/financial advisor.

AOTH/Richard Mills recommends that before investing in any securities, you consult with a professional financial planner or advisor, and that you should conduct a complete and independent investigation before investing in any security after prudent consideration of all pertinent risks. Ahead of the Herd is not a registered broker, dealer, analyst, or advisor. We hold no investment licenses and may not sell, offer to sell, or offer to buy any security.

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.

{kind=link}